You might also like

- MBA Syllabus: Department of Accounting and Information Systems Jagannath University, DhakaDocument18 pagesMBA Syllabus: Department of Accounting and Information Systems Jagannath University, DhakaIbrahim Arafat ZicoNo ratings yet

- MBA SyllabusDocument18 pagesMBA SyllabusShaheen MahmudNo ratings yet

- Lesson Plan Far 600Document7 pagesLesson Plan Far 600ewinzeNo ratings yet

- Financial Reporting, Financial Statement Analysis and Valuation: A Strategic PerspectiveDocument5 pagesFinancial Reporting, Financial Statement Analysis and Valuation: A Strategic PerspectiveDiana CalderonNo ratings yet

- Syllabus PGDM FMDocument73 pagesSyllabus PGDM FMyash_meetuNo ratings yet

- Financial Acccounting MBA KUKDocument125 pagesFinancial Acccounting MBA KUKlalit_wadhwa_1100% (2)

- FA Sem1 FADocument2 pagesFA Sem1 FApraveenpatidar209No ratings yet

- Fundamentals of AccountingDocument3 pagesFundamentals of AccountingJessica100% (2)

- Unit 2Document25 pagesUnit 2FantayNo ratings yet

- MBA SyllabusDocument18 pagesMBA SyllabusAdnanNo ratings yet

- Fa A Accounting For ManagementDocument1 pageFa A Accounting For ManagementKshitij BhatiaNo ratings yet

- Core 10Document194 pagesCore 10Ashutosh Patro100% (1)

- A FMDocument9 pagesA FMshalu_duaNo ratings yet

- Principles of Accounting: Course DescriptionDocument10 pagesPrinciples of Accounting: Course DescriptionFasil BulaNo ratings yet

- Course Outline FINANCIAL AND MANAGERIAL ACC DBU 2014 - 020642Document3 pagesCourse Outline FINANCIAL AND MANAGERIAL ACC DBU 2014 - 020642Ahmed YimamNo ratings yet

- MGT105Document8 pagesMGT105shahnwazNo ratings yet

- 11f9eAFM SyllabusDocument2 pages11f9eAFM SyllabusSomu TiwariNo ratings yet

- BRMD 503 - Syllabus - Beirut Campus Spring 2015Document10 pagesBRMD 503 - Syllabus - Beirut Campus Spring 2015SaraBazziNo ratings yet

- MBA Syllabus: Department of Accounting and Information Systems Jagannath University, DhakaDocument18 pagesMBA Syllabus: Department of Accounting and Information Systems Jagannath University, Dhakasakib990100% (1)

- IILM Graduate School of ManagementDocument15 pagesIILM Graduate School of ManagementMd. Shad AnwarNo ratings yet

- BBA 1.4 Chapter 1 Notes 1Document10 pagesBBA 1.4 Chapter 1 Notes 1Gaurav vaidyaNo ratings yet

- Topics in Accounting Research SyllabusDocument9 pagesTopics in Accounting Research SyllabusumaarrNo ratings yet

- Solapur Uni. Mcom III & IV SyllabusDocument7 pagesSolapur Uni. Mcom III & IV Syllabusshaikh_naeem10No ratings yet

- DAC 501 Financial Accounting IDocument11 pagesDAC 501 Financial Accounting IdmugalloyNo ratings yet

- Financial Statement Analysis: Course DescriptionDocument4 pagesFinancial Statement Analysis: Course DescriptionMohsin RazaNo ratings yet

- Accounting Hounours 4th Year SyllabusDocument11 pagesAccounting Hounours 4th Year SyllabusMD Sakib HasanNo ratings yet

- The Essentials of Finance and Accounting for Nonfinancial ManagersFrom EverandThe Essentials of Finance and Accounting for Nonfinancial ManagersRating: 5 out of 5 stars5/5 (1)

- Curriculum: Masters in Business Administrat 2020-2022 Term: 1 - Semester Course: MGC1051 - Financial Accounting and AnalysisDocument16 pagesCurriculum: Masters in Business Administrat 2020-2022 Term: 1 - Semester Course: MGC1051 - Financial Accounting and AnalysisAnand BabarNo ratings yet

- Conceptual Framework in Financial AccountingDocument39 pagesConceptual Framework in Financial AccountingVon Lloyd Ledesma LorenNo ratings yet

- Ec7a3microsoft Word - Accounting For ManagementDocument1 pageEc7a3microsoft Word - Accounting For ManagementYasar SadiqNo ratings yet

- Financial Management: Partner in Driving Performance and ValueFrom EverandFinancial Management: Partner in Driving Performance and ValueNo ratings yet

- B. Tech Sem - I SUBJECT-Financial and Management Accounting (AF310) Teaching Scheme (Hr/week) Exam Scheme (Marks)Document6 pagesB. Tech Sem - I SUBJECT-Financial and Management Accounting (AF310) Teaching Scheme (Hr/week) Exam Scheme (Marks)ShaifaliMalukaniNo ratings yet

- (Part 2) Conceptual Framework (Doni, Bagas, Papin)Document30 pages(Part 2) Conceptual Framework (Doni, Bagas, Papin)Kazuyano DoniNo ratings yet

- Accounting For ManagersDocument2 pagesAccounting For Managersvivekgarg33.vgNo ratings yet

- Financial Accounting TheoryDocument8 pagesFinancial Accounting TheoryJustAHumanNo ratings yet

- BBA 2nd Semester Syllabus 2022Document16 pagesBBA 2nd Semester Syllabus 2022Ramanand YadavNo ratings yet

- Financial Accounting 1 Unit 2Document22 pagesFinancial Accounting 1 Unit 2AbdirahmanNo ratings yet

- 511 Ac & Finance For ManagersDocument3 pages511 Ac & Finance For ManagersYonasNo ratings yet

- AccountingDocument4 pagesAccountingSirtsepoNo ratings yet

- Study Material Accountancy Class 11th 2023-24Document146 pagesStudy Material Accountancy Class 11th 2023-24Drishti ChauhanNo ratings yet

- Study Material Accountancy Class 11th 2023-24-1Document138 pagesStudy Material Accountancy Class 11th 2023-24-1ganesh100% (1)

- Management AccountingDocument132 pagesManagement AccountingTarun Tater100% (1)

- Unit 02 Conceptual FrameworkDocument17 pagesUnit 02 Conceptual FrameworkNixsan MenaNo ratings yet

- (BBA) 2019-2023 GCUF Course OutlineDocument126 pages(BBA) 2019-2023 GCUF Course Outlinenadir60% (10)

- Syllabus BCOMACCT 2020-2021Document30 pagesSyllabus BCOMACCT 2020-2021Prîyôjèét KârmåkàrNo ratings yet

- Intermediate Accounting Principles and Analysis 2nd Edition Warfield Solutions ManualDocument36 pagesIntermediate Accounting Principles and Analysis 2nd Edition Warfield Solutions Manualsportfulscenefulzb3nhNo ratings yet

- Syllabus Final For I II III and IV SEM-2022-23Document50 pagesSyllabus Final For I II III and IV SEM-2022-23PrajwalNo ratings yet

- Accounting System PDFDocument122 pagesAccounting System PDFmanoj100% (1)

- Financial AccountingDocument3 pagesFinancial AccountingMikeNo ratings yet

- Fundamental of Accounting and Auditing ICSIDocument408 pagesFundamental of Accounting and Auditing ICSIKimi WaliaNo ratings yet

- Value Creation in Management Accounting and Strategic Management: An Integrated ApproachFrom EverandValue Creation in Management Accounting and Strategic Management: An Integrated ApproachNo ratings yet

- AcctsDocument3 pagesAcctsSimran GuptaNo ratings yet

- 1416175152877c Syllab. MBA.1st - Send. Final.3rdDocument14 pages1416175152877c Syllab. MBA.1st - Send. Final.3rdE M P E R O RNo ratings yet

- Bangalore University BBM 5th Semester Core SubjectsDocument7 pagesBangalore University BBM 5th Semester Core SubjectsHarsha Shivanna0% (1)

- International Financial Statement AnalysisFrom EverandInternational Financial Statement AnalysisRating: 1 out of 5 stars1/5 (1)

- Wiley CMAexcel Learning System Exam Review 2017: Part 2, Financial Decision Making (1-year access)From EverandWiley CMAexcel Learning System Exam Review 2017: Part 2, Financial Decision Making (1-year access)No ratings yet

- PDCA ModelDocument1 pagePDCA ModelTiffany SmithNo ratings yet

- Reta Sharfina Tahar 1111002006 Case 10-1 Variance Analysis ProblemsDocument2 pagesReta Sharfina Tahar 1111002006 Case 10-1 Variance Analysis ProblemsTiffany SmithNo ratings yet

- SM Case - Strategic AlliancesDocument2 pagesSM Case - Strategic AlliancesTiffany SmithNo ratings yet

- Case 5-1&5-4Document3 pagesCase 5-1&5-4Tiffany SmithNo ratings yet

- Minggu 7 Case 7-1 SPMDocument2 pagesMinggu 7 Case 7-1 SPMTiffany SmithNo ratings yet

- FSCDocument12 pagesFSCTiffany SmithNo ratings yet

- Summary of Starbucks' Management: Change and Innovation at StarbucksDocument3 pagesSummary of Starbucks' Management: Change and Innovation at StarbucksTiffany SmithNo ratings yet

- Inventory AuditDocument26 pagesInventory AuditTiffany SmithNo ratings yet

- Case 6 - 2 and Seminar 3 ExcersisesDocument3 pagesCase 6 - 2 and Seminar 3 ExcersisesStany D'melloNo ratings yet

- Case StudyDocument42 pagesCase StudyBrian MayolNo ratings yet

- Riza Haditia Saputri 1121002041Document3 pagesRiza Haditia Saputri 1121002041Tiffany SmithNo ratings yet

- Syllabus: Course DescriptionDocument7 pagesSyllabus: Course DescriptionTiffany SmithNo ratings yet

- Expenditure Multipliers: The Keynesian Model : Key ConceptsDocument15 pagesExpenditure Multipliers: The Keynesian Model : Key ConceptsTiffany SmithNo ratings yet

- Besanko HarvardDocument228 pagesBesanko Harvardkjmnlkmh100% (1)

- 03 Answers To All ProblemsDocument20 pages03 Answers To All ProblemsTiffany SmithNo ratings yet

- AEB14 SM CH17 v2Document31 pagesAEB14 SM CH17 v2RonLiu350% (1)

- Ob C2A006136 PDFDocument33 pagesOb C2A006136 PDFTiffany SmithNo ratings yet

- Chapter 12 SolutionDocument1 pageChapter 12 SolutionTiffany SmithNo ratings yet

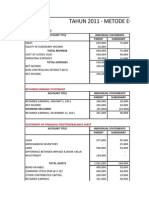

- Tahun 2011 - Metode Equity: Income StementDocument8 pagesTahun 2011 - Metode Equity: Income StementTiffany SmithNo ratings yet

- Print 3 RangkapDocument4 pagesPrint 3 RangkapTiffany SmithNo ratings yet

- Cpa Review School of The Philippines Manila Management Advisory Services Relevant CostingDocument13 pagesCpa Review School of The Philippines Manila Management Advisory Services Relevant CostingLive LoveNo ratings yet

- More Solved Examples PDFDocument16 pagesMore Solved Examples PDFrobbsNo ratings yet

- Infosys - Q4FY22 - Result Update - Investor ReportDocument10 pagesInfosys - Q4FY22 - Result Update - Investor ReportSavil GuptaNo ratings yet

- Moduel 4 Financial Statement Modeling Theory and ConceptsDocument26 pagesModuel 4 Financial Statement Modeling Theory and ConceptsAkshay Krishnan P RCBSNo ratings yet

- Winning in The Marketplace: Coffee House Taste by The Cup™Document13 pagesWinning in The Marketplace: Coffee House Taste by The Cup™Lilac CocoNo ratings yet

- Aecon - Project IDocument39 pagesAecon - Project IRaji MohanNo ratings yet

- Mergers and Acquisitions 314 v1 PDFDocument434 pagesMergers and Acquisitions 314 v1 PDFKavita KumawatNo ratings yet

- Application For Deceased ClaimDocument38 pagesApplication For Deceased Claimmohammed258No ratings yet

- Financial Management (MBOF 912 D) 1Document5 pagesFinancial Management (MBOF 912 D) 1Siva KumarNo ratings yet

- Corporate Tax Avoidance: A Literature Review and Research Agenda: Corporate Tax AvoidanceDocument20 pagesCorporate Tax Avoidance: A Literature Review and Research Agenda: Corporate Tax AvoidanceBudi UtomoNo ratings yet

- TLE - HO ME EC ON Omics 6: Weekly Home PlanDocument8 pagesTLE - HO ME EC ON Omics 6: Weekly Home PlanJEROME GONDRADA SISONNo ratings yet

- 2013-14 State Aid Projections (Final Budget)Document88 pages2013-14 State Aid Projections (Final Budget)robertharding22No ratings yet

- Guide To Cashflow 101 TrainingDocument5 pagesGuide To Cashflow 101 TrainingTong Kah Haw100% (2)

- Ar 2020 BTPN Eng 14 AprilDocument612 pagesAr 2020 BTPN Eng 14 AprilklieindwrNo ratings yet

- Syntech FibresDocument33 pagesSyntech FibresSaaDii KhanNo ratings yet

- Do It! 2: Accounting Principles (1) First GradeDocument4 pagesDo It! 2: Accounting Principles (1) First GradeAmer Wagdy GergesNo ratings yet

- Notre Dame Educational Association: Mock Board Examination TaxationDocument10 pagesNotre Dame Educational Association: Mock Board Examination TaxationirishjadeNo ratings yet

- LBR JWB Sesi 2 - ANGLE OF VIEW - 2020Document12 pagesLBR JWB Sesi 2 - ANGLE OF VIEW - 2020cupliswelNo ratings yet

- Ambulance ServiceDocument9 pagesAmbulance ServicedennymxNo ratings yet

- Equity Research Report On Tata MotorsDocument26 pagesEquity Research Report On Tata MotorsRijul SaxenaNo ratings yet

- AdvanceDocument32 pagesAdvancemuse tamiruNo ratings yet

- GST - Introduction To GST & Concept of SupplyDocument40 pagesGST - Introduction To GST & Concept of Supplydeepak singhalNo ratings yet

- There Are Some Major Key Performance Indicators For Chemical Industry: 1. FinancialDocument3 pagesThere Are Some Major Key Performance Indicators For Chemical Industry: 1. FinancialsonuNo ratings yet

- Microns20 DraftDocument294 pagesMicrons20 DraftadhavvikasNo ratings yet

- Mind Map Chapter 3 and 4 OutlineDocument2 pagesMind Map Chapter 3 and 4 OutlinePatricia SantosNo ratings yet

- Investments 3.4 March 2010 With AnswersDocument15 pagesInvestments 3.4 March 2010 With AnswersshironagaseNo ratings yet

- ACCT 3001 Chapter 5 Assigned Homework SolutionsDocument18 pagesACCT 3001 Chapter 5 Assigned Homework SolutionsPeter ParkNo ratings yet

- Investment Analysis Polar Sports ADocument9 pagesInvestment Analysis Polar Sports AtalabreNo ratings yet

- Financial Management Economics For Finance 2023 1671444516Document36 pagesFinancial Management Economics For Finance 2023 1671444516RADHIKANo ratings yet

- Paradise Island Resort A Completed Business PlanDocument30 pagesParadise Island Resort A Completed Business PlanMohdShahrukh100% (2)