You might also like

- 3D Printing in Chemical Engineering and Catalytic Technology: Structured Catalysts, Mixers and ReactorsDocument35 pages3D Printing in Chemical Engineering and Catalytic Technology: Structured Catalysts, Mixers and ReactorsakshaykgNo ratings yet

- Processes MTP 03 00684 v2Document15 pagesProcesses MTP 03 00684 v2akshaykgNo ratings yet

- Continuous Production of Squalane Using 3D Printed Catalytic SupportsDocument14 pagesContinuous Production of Squalane Using 3D Printed Catalytic SupportsakshaykgNo ratings yet

- IBS Renault Nissan Alliance FinalDocument24 pagesIBS Renault Nissan Alliance FinalakshaykgNo ratings yet

- Marketing Management - Gold GymDocument23 pagesMarketing Management - Gold Gymakshaykg67% (3)

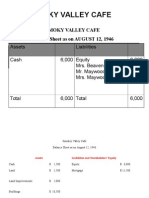

- Smoky Valley Cafe Balance Sheet As On AUGUST 12, 1946Document3 pagesSmoky Valley Cafe Balance Sheet As On AUGUST 12, 1946akshaykgNo ratings yet

- Sula Wines Presentation Group 7Document21 pagesSula Wines Presentation Group 7akshaykg100% (1)

- SM Project - Tata Solar-Competitive Strategy - Group7 (Section A) - EPGDIB 2014-15Document18 pagesSM Project - Tata Solar-Competitive Strategy - Group7 (Section A) - EPGDIB 2014-15akshaykgNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5795)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Project Global WarmingDocument3 pagesProject Global Warmingdiotima hazra100% (9)

- UnemploymentDocument31 pagesUnemploymentSyed badshahNo ratings yet

- Bourguignon and Morisson - 2002 - History of InequalityDocument18 pagesBourguignon and Morisson - 2002 - History of InequalityAeron Rai RoqueNo ratings yet

- A Capitalist Road To Communism 20 Years AfterDocument23 pagesA Capitalist Road To Communism 20 Years AfterTopeteNo ratings yet

- 3rd Part Social StratificationDocument29 pages3rd Part Social StratificationJena Manglicmot FortinNo ratings yet

- Konsep & Macam Indikator Ekonomi: Prof. Insukindro, PH.DDocument21 pagesKonsep & Macam Indikator Ekonomi: Prof. Insukindro, PH.DAndri IantoNo ratings yet

- Measuring The Cost of Living: Test BDocument7 pagesMeasuring The Cost of Living: Test Bmas_999No ratings yet

- Ex Ante and Ex Post MeaningDocument2 pagesEx Ante and Ex Post MeaningKamal PrasadNo ratings yet

- Teks Eksplanasi Pengangguran-DikonversiDocument1 pageTeks Eksplanasi Pengangguran-DikonversiAprilia Rizki PurnitasariNo ratings yet

- STS W11-1 Climate Change and Energy Crisis PDFDocument15 pagesSTS W11-1 Climate Change and Energy Crisis PDFJohn D50% (2)

- CPI CalculationDocument5 pagesCPI CalculationAnnu MeerNo ratings yet

- Wealth and Income Inequality TableDocument6 pagesWealth and Income Inequality Tableapi-589628245No ratings yet

- By, Carol Peters Prabhu Ii BBM Mahesh College of ManagementDocument12 pagesBy, Carol Peters Prabhu Ii BBM Mahesh College of ManagementcarolsaviapetersNo ratings yet

- Beijing's Lessons For Central Banks - FT Stephen RoachDocument3 pagesBeijing's Lessons For Central Banks - FT Stephen Roach3bandhuNo ratings yet

- Briefly Explain Okun's Law. Why Should Economists Care About Inflation and Unemployment?Document4 pagesBriefly Explain Okun's Law. Why Should Economists Care About Inflation and Unemployment?Arslan siddiqueNo ratings yet

- Consumer Price IndexDocument20 pagesConsumer Price IndexBritt John Ballentes0% (1)

- FHCE Fed Poverty LevelDocument2 pagesFHCE Fed Poverty Levelabc xyzNo ratings yet

- Unemploymentcopy Aug2011Document24 pagesUnemploymentcopy Aug2011Panda RodulfaNo ratings yet

- Real GDP, Nominal GDP and GrowthDocument2 pagesReal GDP, Nominal GDP and GrowthLý ĐinhNo ratings yet

- Bourguignon - 2002 - Inequality Among World Citizens, 1820-1992Document19 pagesBourguignon - 2002 - Inequality Among World Citizens, 1820-1992yezuh077No ratings yet

- Chap III InflationDocument34 pagesChap III InflationVAISALY S MBANo ratings yet

- What Is Economic DepressionDocument4 pagesWhat Is Economic DepressionFarhana RahmanNo ratings yet

- Indian Economy by Ramesh Singh 11 EditionDocument51 pagesIndian Economy by Ramesh Singh 11 Editionanon_726388494No ratings yet

- Chapter 12 Business CycleDocument38 pagesChapter 12 Business CycleCeline PanimdimNo ratings yet

- Mozal ExcelDocument4 pagesMozal Excelderek4wellNo ratings yet

- CH 12 PracticeDocument6 pagesCH 12 PracticeAli Abdullah Al-Saffar100% (1)

- Teacher Notes - Carbon FootprintDocument1 pageTeacher Notes - Carbon FootprintElena LópezNo ratings yet

- Unit 35 The Short-Run Trade-Off Between Inflation and UnemploymentDocument3 pagesUnit 35 The Short-Run Trade-Off Between Inflation and UnemploymentMinh Châu Tạ ThịNo ratings yet

- Notes On Inflation: How To Measure InflationDocument2 pagesNotes On Inflation: How To Measure InflationMark WatneyNo ratings yet

- Principles of Macroeconomics 6th Edition Frank Test Bank 1Document36 pagesPrinciples of Macroeconomics 6th Edition Frank Test Bank 1cynthiasheltondegsypokmj100% (24)