You might also like

- Republic of The Philippines: Supreme CourtDocument12 pagesRepublic of The Philippines: Supreme CourtmrrrkkkNo ratings yet

- Coc v. Hypermix FeedsDocument9 pagesCoc v. Hypermix FeedsHaniyyah FtmNo ratings yet

- Commissioner of Customs, Et Al. vs. Hypermix Feeds CorporationDocument9 pagesCommissioner of Customs, Et Al. vs. Hypermix Feeds CorporationiccNo ratings yet

- Commissioner of Customs vs. Hypermix Feeds CorpDocument7 pagesCommissioner of Customs vs. Hypermix Feeds CorpJonjon BeeNo ratings yet

- Equal Protection Clause and The Rule of Uniformity of TaxationDocument124 pagesEqual Protection Clause and The Rule of Uniformity of TaxationIxhanie Cawal-oNo ratings yet

- Commissioner of Customs V HypermixDocument5 pagesCommissioner of Customs V Hypermixada9ablaoNo ratings yet

- Commissioner of Customs v. HypermixDocument8 pagesCommissioner of Customs v. HypermixJc IsidroNo ratings yet

- Commissioner of Customs v. Hypemix FeedsDocument6 pagesCommissioner of Customs v. Hypemix FeedsShayne SiguaNo ratings yet

- Commissioner of Customs vs. Hypermix Feeds G.R. No. 179579, February 1, 2012Document11 pagesCommissioner of Customs vs. Hypermix Feeds G.R. No. 179579, February 1, 2012Clarinda Merle100% (1)

- G.R. No. 179579 - Customs V Hypermix FeedsDocument13 pagesG.R. No. 179579 - Customs V Hypermix FeedsanjNo ratings yet

- Supreme Court: Custom SearchDocument5 pagesSupreme Court: Custom SearchsofiaqueenNo ratings yet

- Persons CD 0Document15 pagesPersons CD 0Jen BalmeoNo ratings yet

- SC upholds nullification of Customs regulation on wheat tariff classificationDocument5 pagesSC upholds nullification of Customs regulation on wheat tariff classificationLester AgoncilloNo ratings yet

- Commissioner of Customs v. Hypermix Feeds Corporation PDFDocument5 pagesCommissioner of Customs v. Hypermix Feeds Corporation PDFMarion Yves MosonesNo ratings yet

- 6 Commissioner of Customs V Hypermix Feeds CorpDocument3 pages6 Commissioner of Customs V Hypermix Feeds CorpJaz SumalinogNo ratings yet

- Supreme Court: Custom SearchDocument6 pagesSupreme Court: Custom Searchbai sinsuatNo ratings yet

- CUSTOMS RULING ON WHEAT TARIFF CLASSIFICATION STRUCK DOWNDocument4 pagesCUSTOMS RULING ON WHEAT TARIFF CLASSIFICATION STRUCK DOWNLoNo ratings yet

- SMART V NTCDocument5 pagesSMART V NTCAtty Mglrt100% (1)

- SEC ruling on Citibank sale of unregistered securitiesDocument4 pagesSEC ruling on Citibank sale of unregistered securitiesJeric Anne Azores-PresnediNo ratings yet

- Ilado Vs ChavezDocument4 pagesIlado Vs ChavezbennysalayogNo ratings yet

- Tax1. Cases. 7. A. Organization and Functions of The Bureau of Internal Revenue - 2. Income TaxDocument50 pagesTax1. Cases. 7. A. Organization and Functions of The Bureau of Internal Revenue - 2. Income TaxLecdiee Nhojiezz Tacissea SalnackyiNo ratings yet

- Commissioner of Customs V Hypermix Feeds Corp.Document2 pagesCommissioner of Customs V Hypermix Feeds Corp.Elah ViktoriaNo ratings yet

- Substance Vs ProcedureDocument6 pagesSubstance Vs ProcedureDianne MedianeroNo ratings yet

- SEC ruling on sale of unregistered securitiesDocument5 pagesSEC ruling on sale of unregistered securitiesMarilou GaralNo ratings yet

- Res judicata bars second case on membership statusDocument37 pagesRes judicata bars second case on membership statusDonna PhoebeNo ratings yet

- First Lepanto vs. CA, G.R. No. 110571, Mar. 10, 1994Document7 pagesFirst Lepanto vs. CA, G.R. No. 110571, Mar. 10, 1994Yna Marei AguilarNo ratings yet

- Digested - Insular Savings Bank v. Far East Bank and Trust CompanyDocument3 pagesDigested - Insular Savings Bank v. Far East Bank and Trust CompanyJean UcolNo ratings yet

- Arbitration Award Confirmed Despite Lack of Due ProcessDocument3 pagesArbitration Award Confirmed Despite Lack of Due ProcessJaz SumalinogNo ratings yet

- 67 People v. JumawanDocument27 pages67 People v. JumawanJia Chu ChuaNo ratings yet

- RUTH D. BAUTISTA v. CADocument8 pagesRUTH D. BAUTISTA v. CAChatNo ratings yet

- 56 Commissioner of Customs V HypermixDocument5 pages56 Commissioner of Customs V Hypermix01123813No ratings yet

- NTC Regulation on Billing Rules ChallengedDocument2 pagesNTC Regulation on Billing Rules ChallengedBea CapeNo ratings yet

- Civil Proc DigestsDocument40 pagesCivil Proc Digestsmubarak.gutocNo ratings yet

- First Lepanto Ceramics, Inc. vs. CA, 231 SCRA 30 (1994)Document5 pagesFirst Lepanto Ceramics, Inc. vs. CA, 231 SCRA 30 (1994)Jellie Grace CañeteNo ratings yet

- Civil Procedure B Group AssignmentDocument14 pagesCivil Procedure B Group Assignmentipenguin26No ratings yet

- NTC vs SMART & PILTELDocument58 pagesNTC vs SMART & PILTELRogelineNo ratings yet

- Highlighted Fulltext - ANDREA TAN, CLARITA LLAMAS, VICTOR ESPINA and LUISA ESPINA, Petitioners, v. BAUSCH & LOMB, INC., Respondent.Document5 pagesHighlighted Fulltext - ANDREA TAN, CLARITA LLAMAS, VICTOR ESPINA and LUISA ESPINA, Petitioners, v. BAUSCH & LOMB, INC., Respondent.Charity RomagaNo ratings yet

- Stage 2 Legal ResearchDocument11 pagesStage 2 Legal ResearchnchlrysNo ratings yet

- Audi AG Vs Mejia - RemRev Case DigestDocument2 pagesAudi AG Vs Mejia - RemRev Case DigestPam Otic-ReyesNo ratings yet

- Panay Railways Vs HEVA ManagementDocument2 pagesPanay Railways Vs HEVA ManagementMan-Man AcabNo ratings yet

- Panay Railways, Inc. v. Heva Management, G.R. No. 154061, January 25, 2012Document2 pagesPanay Railways, Inc. v. Heva Management, G.R. No. 154061, January 25, 2012Allyza RamirezNo ratings yet

- Petitioner RespondentDocument31 pagesPetitioner RespondentSeok Gyeong KangNo ratings yet

- Velasco, JR., J.Document15 pagesVelasco, JR., J.yenNo ratings yet

- Case For UploadDocument3 pagesCase For Uploadjappy27No ratings yet

- Abrenica v. Law Firm of Abrenica (G.r. No. 169420)Document3 pagesAbrenica v. Law Firm of Abrenica (G.r. No. 169420)CHARMAINE KLAIRE ALONZONo ratings yet

- Civil Application No Nai 32 of 2015 June 12 - 2015 PDFDocument14 pagesCivil Application No Nai 32 of 2015 June 12 - 2015 PDFfelixmuyoveNo ratings yet

- Board of Trustees v. Velasco, G.R. No. 170436, February 2, 2011Document4 pagesBoard of Trustees v. Velasco, G.R. No. 170436, February 2, 2011LegaspiCabatchaNo ratings yet

- Digested Cases in Constitutional Law 1 - Atty. Antonio Eduardo Nachura - 1B, 1H, 1N 2018-2019Document3 pagesDigested Cases in Constitutional Law 1 - Atty. Antonio Eduardo Nachura - 1B, 1H, 1N 2018-2019Phoebe MascariñasNo ratings yet

- Supreme Court: Custom SearchDocument6 pagesSupreme Court: Custom SearchGraile Dela CruzNo ratings yet

- Bautista vs. CADocument8 pagesBautista vs. CAHannah MedesNo ratings yet

- Petition For ProhibitionDocument13 pagesPetition For Prohibitionfrances_mae100% (1)

- Law Firm Partnership Dispute Appeal DismissedDocument4 pagesLaw Firm Partnership Dispute Appeal DismissedRandy SiosonNo ratings yet

- Commissioner of Cutoms Vs Hypermix Feeds CorporationDocument2 pagesCommissioner of Cutoms Vs Hypermix Feeds CorporationEileen Eika Dela Cruz-Lee83% (6)

- 8 Panay Railways VS Heva Management CorporationDocument3 pages8 Panay Railways VS Heva Management CorporationRENGIE GALONo ratings yet

- Belongilot V CuaDocument13 pagesBelongilot V CuaIvan Montealegre ConchasNo ratings yet

- SC rules on jurisdiction over appeals from MeTC decisionsDocument54 pagesSC rules on jurisdiction over appeals from MeTC decisionsKen EroNo ratings yet

- Commissioner of Customs v. HypermixDocument3 pagesCommissioner of Customs v. HypermixReino CabitacNo ratings yet

- Remedial Law Review Case Digests 1-20Document36 pagesRemedial Law Review Case Digests 1-20Pipoy Amy100% (1)

- California Supreme Court Petition: S173448 – Denied Without OpinionFrom EverandCalifornia Supreme Court Petition: S173448 – Denied Without OpinionRating: 4 out of 5 stars4/5 (1)

- Bar Review Companion: Remedial Law: Anvil Law Books Series, #2From EverandBar Review Companion: Remedial Law: Anvil Law Books Series, #2Rating: 3 out of 5 stars3/5 (2)

- White Gold V Pioneer GDocument14 pagesWhite Gold V Pioneer Gfjl_302711No ratings yet

- Digital Photography: Course DescriptionDocument1 pageDigital Photography: Course Descriptionfjl_302711No ratings yet

- Manalo Vs CADocument1 pageManalo Vs CAELDA QUIROGNo ratings yet

- Aruego V CaDocument7 pagesAruego V Cafjl_302711No ratings yet

- Supapo vs. Spouses de JesusDocument17 pagesSupapo vs. Spouses de Jesusfjl_302711No ratings yet

- LC All Enamel&Powder Roman CatholicDocument1 pageLC All Enamel&Powder Roman Catholicfjl_302711No ratings yet

- Expropriation suits fall under RTC jurisdictionDocument6 pagesExpropriation suits fall under RTC jurisdictionfjl_302711No ratings yet

- David Reyes v. Jose LimDocument6 pagesDavid Reyes v. Jose Limfjl_302711No ratings yet

- Sps. Villuga and Mercedita Villuga, v. Kelly Hardware and Construction Supply IncDocument1 pageSps. Villuga and Mercedita Villuga, v. Kelly Hardware and Construction Supply Incfjl_302711No ratings yet

- Boston Equity V CADocument2 pagesBoston Equity V CAfjl_302711No ratings yet

- Alvero v. de La RosaDocument3 pagesAlvero v. de La Rosafjl_302711No ratings yet

- Cocofed v. Republic of The PhilippinesDocument2 pagesCocofed v. Republic of The Philippinesfjl_302711No ratings yet

- ENVI 5 - Almuete Vs People DigestDocument1 pageENVI 5 - Almuete Vs People DigestErika BarbaronaNo ratings yet

- Uniwide vs Trajano Supreme Court DecisionDocument7 pagesUniwide vs Trajano Supreme Court Decisionfjl_302711No ratings yet

- Bir vs. Fortune Tobacco CorporationDocument2 pagesBir vs. Fortune Tobacco Corporationfjl_302711No ratings yet

- CACHO V CA (1997) Facts:: Melo, J.Document3 pagesCACHO V CA (1997) Facts:: Melo, J.fjl_302711No ratings yet

- First Leverage and Services Group, Inc v. Solid Builders, IncDocument1 pageFirst Leverage and Services Group, Inc v. Solid Builders, Incfjl_302711No ratings yet

- Land dispute case denied reviewDocument2 pagesLand dispute case denied reviewfjl_302711No ratings yet

- Mateo Vs MorenoDocument2 pagesMateo Vs Morenofjl_302711No ratings yet

- MANDATORY NEWSPAPER PUBLICATIONDocument3 pagesMANDATORY NEWSPAPER PUBLICATIONfjl_302711No ratings yet

- Chavez Vs PEA Case DigestDocument3 pagesChavez Vs PEA Case Digestfjl_302711100% (5)

- Secretary of DENR Vs Yap - DigestDocument2 pagesSecretary of DENR Vs Yap - Digestfjl_302711No ratings yet

- Ernesto Guevara v. Rosario GuevaraDocument1 pageErnesto Guevara v. Rosario Guevarafjl_302711No ratings yet

- Cayanan vs. De los Santos land disputeDocument1 pageCayanan vs. De los Santos land disputefjl_302711No ratings yet

- Republic vs. Intermediate Appellate Court, 186 SCRA 88Document8 pagesRepublic vs. Intermediate Appellate Court, 186 SCRA 88fjl_302711No ratings yet

- Leyva Vs JandocDocument1 pageLeyva Vs Jandocfjl_302711No ratings yet

- Palomo Vs CADocument2 pagesPalomo Vs CAfjl_302711100% (2)

- Divina v. CADocument1 pageDivina v. CAfjl_302711No ratings yet

- GR 52518 Internaltional Hardwood Vs UP August 13, 1991Document4 pagesGR 52518 Internaltional Hardwood Vs UP August 13, 1991fjl_3027110% (1)

- Heirs of Jacob v. CADocument8 pagesHeirs of Jacob v. CAfjl_302711No ratings yet

- Bihar Excise Act Chapter on Establishments, Control, Appeal and RevisionDocument40 pagesBihar Excise Act Chapter on Establishments, Control, Appeal and RevisionKumar SunnyNo ratings yet

- Fresh Fruit Compote Export GuideDocument17 pagesFresh Fruit Compote Export GuideMaya0% (1)

- Quarterly Newsletter on Water Governance Reforms in IndiaDocument16 pagesQuarterly Newsletter on Water Governance Reforms in IndiaSachin WarghadeNo ratings yet

- Case Study 1Document16 pagesCase Study 1Raj SethiNo ratings yet

- Zim Court Rules on Returning Resident's Vehicle Rebate DisputeDocument9 pagesZim Court Rules on Returning Resident's Vehicle Rebate DisputeColias DubeNo ratings yet

- NWRB Regulations: A Presentation For "Public Dialogue On Bulk Water Meter Arrangements" Quezon City, June 26, 2014Document19 pagesNWRB Regulations: A Presentation For "Public Dialogue On Bulk Water Meter Arrangements" Quezon City, June 26, 2014Catherine Kaye Belarmino AlmonteNo ratings yet

- Notice: Textile and Apparel Categories: Cotton, Wool, and Man-Made Textiles— HondurasDocument3 pagesNotice: Textile and Apparel Categories: Cotton, Wool, and Man-Made Textiles— HondurasJustia.comNo ratings yet

- IM - Tea To EgyptDocument25 pagesIM - Tea To EgyptBadar Qureshi100% (1)

- Bot & Bto ContractsDocument65 pagesBot & Bto ContractsWalid GradaNo ratings yet

- Direct & Indirect Tax Structure in India-FinalDocument23 pagesDirect & Indirect Tax Structure in India-FinalJivaansha SinhaNo ratings yet

- Olympiad QuestionsDocument7 pagesOlympiad QuestionsAsilbek AshurovNo ratings yet

- Flexible Clause Refer To The Power of The President Upon Recommendation ofDocument11 pagesFlexible Clause Refer To The Power of The President Upon Recommendation ofjharik23No ratings yet

- Econ 90 - Chapter 9 ReportDocument11 pagesEcon 90 - Chapter 9 ReportAnn Marie Abadies PalahangNo ratings yet

- JM Financial - Initiating Coverage On Power Financiers.Document73 pagesJM Financial - Initiating Coverage On Power Financiers.adityasood811731No ratings yet

- Starbucks A Strategic Report by James HeaveyDocument20 pagesStarbucks A Strategic Report by James HeaveySharon100% (11)

- Basic Principles of TaxationDocument55 pagesBasic Principles of TaxationKira LimNo ratings yet

- The Analysis of Competitive MarketsDocument94 pagesThe Analysis of Competitive MarketsMesrySimorangkirNo ratings yet

- Southern Cross Cement v. Cement Manufacturer's Assoc., G.R. No. 158540, 2005Document2 pagesSouthern Cross Cement v. Cement Manufacturer's Assoc., G.R. No. 158540, 2005JMae Magat100% (1)

- Import and Export Markets in IndiaDocument21 pagesImport and Export Markets in IndiaAnant Bajaj50% (2)

- Cambridge Past Paper June 2015 Paper 3 EssayDocument2 pagesCambridge Past Paper June 2015 Paper 3 EssayGooroochurn KentishNo ratings yet

- New War Fronts Lie in Economic Zones EssayDocument7 pagesNew War Fronts Lie in Economic Zones EssayJaseem Saleh SiyalNo ratings yet

- Export PromotionDocument16 pagesExport Promotionanshikabatra21167% (3)

- ABAKADA GURO Party List challenges constitutionality of VAT lawDocument3 pagesABAKADA GURO Party List challenges constitutionality of VAT lawchocoberriesNo ratings yet

- Bulk Supply TariffDocument2 pagesBulk Supply TariffshroffhardikNo ratings yet

- International Marketing (TYBMS - Sem 6) : For Private Circulation OnlyDocument20 pagesInternational Marketing (TYBMS - Sem 6) : For Private Circulation OnlyPriteshPanchal100% (1)

- The Swiss fruit and vegetable market overviewDocument36 pagesThe Swiss fruit and vegetable market overviewBernabé Lapuerta MoralesNo ratings yet

- Parity Conditions and Currency Forecasting</bDocument21 pagesParity Conditions and Currency Forecasting</bgalan nationNo ratings yet

- International Marketing 16th Edition Cateora Test BankDocument119 pagesInternational Marketing 16th Edition Cateora Test BankLauraLittlegzmre100% (15)

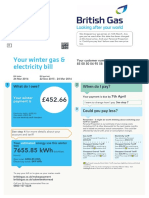

- Your Winter Gas & Electricity Bill: What Do I Owe?Document6 pagesYour Winter Gas & Electricity Bill: What Do I Owe?Tasawar Hussain100% (3)

- Investment Opportunity Profile For Cut Flower Production in EthiopiaDocument9 pagesInvestment Opportunity Profile For Cut Flower Production in EthiopiaqfarmsNo ratings yet