You might also like

- DEED OF ABSOLUTE SALE OF TRICYCLE (Cristina & Abundio)Document1 pageDEED OF ABSOLUTE SALE OF TRICYCLE (Cristina & Abundio)Arkim llovit100% (2)

- Debt Elimination Discharge Set Off, Law, TruthDocument5 pagesDebt Elimination Discharge Set Off, Law, TruthLandiBrown100% (7)

- Contract of LeaseDocument2 pagesContract of LeaseJilian Kate Alpapara Bustamante100% (1)

- NFCC - Oclp TemplateDocument1 pageNFCC - Oclp TemplateFranz Xavier GarciaNo ratings yet

- 3 Mining Platform Mike Da CostaDocument20 pages3 Mining Platform Mike Da CostaJEAN MICHEL ALONZEAUNo ratings yet

- Print Out 13Document1 pagePrint Out 13Taliyow AlowNo ratings yet

- Philips Annual Report 2020 21Document192 pagesPhilips Annual Report 2020 21vadansukhvindersinghNo ratings yet

- 6 Months Debtors Aging Reports: Date: 19/01/2022 Gan SDN BHD (Chor Kai En)Document3 pages6 Months Debtors Aging Reports: Date: 19/01/2022 Gan SDN BHD (Chor Kai En)karenNo ratings yet

- SDN 047182 Laupakam PDFDocument1 pageSDN 047182 Laupakam PDFFebrina TariganNo ratings yet

- Creditor Aging ReportDocument2 pagesCreditor Aging ReportSiti Nur QisthinaNo ratings yet

- Chapter 1Document18 pagesChapter 1Kenny WongNo ratings yet

- GuidelineFull PDFDocument464 pagesGuidelineFull PDFShubham MewadeNo ratings yet

- Bethesda & GoodweekDocument8 pagesBethesda & GoodweekDian Pratiwi RusdyNo ratings yet

- Cargills Ceylon Sustainability 2020-21 FinalDocument52 pagesCargills Ceylon Sustainability 2020-21 FinalPasindu HarshanaNo ratings yet

- GuidelineDocument490 pagesGuidelineRajesh BanwaniNo ratings yet

- AGEHYD28DEC2010Document2 pagesAGEHYD28DEC2010Seema SultanaNo ratings yet

- ROI BaripadaDocument1 pageROI BaripadaTanmay AgarwalaNo ratings yet

- Presentation NBODocument40 pagesPresentation NBODidiNo ratings yet

- GuidelineFull PDFDocument398 pagesGuidelineFull PDFamit_saxena_10No ratings yet

- Print Out 14Document1 pagePrint Out 14Taliyow AlowNo ratings yet

- 39ba0be5b0aaf1128a00e65094e3597d16776d3c87a3a672c82313bfc049968bDocument1 page39ba0be5b0aaf1128a00e65094e3597d16776d3c87a3a672c82313bfc049968bPreethi PushparajNo ratings yet

- Base Case Analysis Best CaseDocument6 pagesBase Case Analysis Best CaseMaphee CastellNo ratings yet

- Quiz 3032Document4 pagesQuiz 3032PG93No ratings yet

- Chhindwara 201720187103 English GuidelinefullDocument420 pagesChhindwara 201720187103 English GuidelinefullTL ICTNo ratings yet

- Daily Production Report: District BPCIDocument1 pageDaily Production Report: District BPCIAnita KarlinaNo ratings yet

- 131197.BSC 02.HW - Piazza.dessie - Ner Eno PPT 20200108 0833Document31 pages131197.BSC 02.HW - Piazza.dessie - Ner Eno PPT 20200108 0833MikatechNo ratings yet

- GDP OverallDocument832 pagesGDP OverallEleanorXuNo ratings yet

- 6 Nov 2018 - HandoutDocument22 pages6 Nov 2018 - Handoutanthony csNo ratings yet

- Niger Delta Coalition For Good Governance: Ekeki, Yenagoa, Bayelsa StateDocument10 pagesNiger Delta Coalition For Good Governance: Ekeki, Yenagoa, Bayelsa StateAbiel John BalogunNo ratings yet

- ExportDocument32 pagesExportwai waiNo ratings yet

- 111007.BSC 04.HW - Nfstel.saaz - Aa Eno PPTDocument27 pages111007.BSC 04.HW - Nfstel.saaz - Aa Eno PPTMikatechNo ratings yet

- FF - Karil Koiriyah - 180421621551 - Tugas 4Document92 pagesFF - Karil Koiriyah - 180421621551 - Tugas 4karinaNo ratings yet

- Mike Beveridge - Doing Business Under The OceanDocument18 pagesMike Beveridge - Doing Business Under The OceanGiacomo CalligarisNo ratings yet

- Housing CharterDocument17 pagesHousing CharternippuNo ratings yet

- Notification of PCBDocument10 pagesNotification of PCBDikkiNo ratings yet

- Business Plan: Proponent: Center Capital: Proposed ProjectDocument3 pagesBusiness Plan: Proponent: Center Capital: Proposed ProjectBorly GonzagaNo ratings yet

- Fabm OutputsDocument3 pagesFabm OutputsElaine Joyce GarciaNo ratings yet

- Current/Closing Rate Method: Adjusted Trial Balance $Document5 pagesCurrent/Closing Rate Method: Adjusted Trial Balance $Daneen GastarNo ratings yet

- Sozni 280-420 PDFDocument10 pagesSozni 280-420 PDFkfc financesNo ratings yet

- Webcrche 2019Document2 pagesWebcrche 2019DANKOIRE HMNo ratings yet

- GuidelinefullDocument526 pagesGuidelinefullSunil NadkarNo ratings yet

- CashflowDocument5 pagesCashflowHanan SalmanNo ratings yet

- Exam Gestion Financier Ratt 2018 Prof MESK - Faculté HASSAN 2 CASABLANCADocument1 pageExam Gestion Financier Ratt 2018 Prof MESK - Faculté HASSAN 2 CASABLANCAAbdoNo ratings yet

- Walking Stick For Blind With Sensors: Presented byDocument12 pagesWalking Stick For Blind With Sensors: Presented byAbbas MookhyNo ratings yet

- A Investment in Website Development: B-I Office & Operating ExpensesDocument15 pagesA Investment in Website Development: B-I Office & Operating ExpensesvaibhavmahajanNo ratings yet

- Lalbaba Engineering Group PresentationDocument21 pagesLalbaba Engineering Group Presentationabhi.s9No ratings yet

- Target Market Every Month 3,600.00 Average Sales Per Customer 25.00Document4 pagesTarget Market Every Month 3,600.00 Average Sales Per Customer 25.00Mark Harold RaspadoNo ratings yet

- Data JioDocument18 pagesData JioAnkit VermaNo ratings yet

- Ujjain Municipal Corporation GuidelineFullDocument511 pagesUjjain Municipal Corporation GuidelineFullPRINCE VERMA75% (4)

- DG 2015irDocument28 pagesDG 2015irGary ManNo ratings yet

- A2 Book For June 2023 p3 FinalDocument532 pagesA2 Book For June 2023 p3 Finals.alisufyaanNo ratings yet

- Awarding Report Set. 1-27, 2015Document3 pagesAwarding Report Set. 1-27, 2015franciscomitzNo ratings yet

- Biogas FinanceDocument9 pagesBiogas FinanceEngr Peter Iyke EboghaNo ratings yet

- 09 - 19 - 31 AF Assignment 3Document19 pages09 - 19 - 31 AF Assignment 320F007 Anto Raglin TNo ratings yet

- Summary of Operating Assumptions (For Example)Document5 pagesSummary of Operating Assumptions (For Example)Krishna SharmaNo ratings yet

- BNWCCC Site Expensess March, 2024Document2 pagesBNWCCC Site Expensess March, 2024reddyrabadaNo ratings yet

- GuidelineFull PDFDocument393 pagesGuidelineFull PDFShubham ChandwaniNo ratings yet

- Investor Meet Presentation May 19Document25 pagesInvestor Meet Presentation May 19Tshering Yangzom NamdaNo ratings yet

- 2021 20-October Part-4 AnswersDocument6 pages2021 20-October Part-4 AnswersLucky NetshamutavhaNo ratings yet

- Industry Statistics Auto Components 09Document7 pagesIndustry Statistics Auto Components 09ManishNo ratings yet

- 151208CapitalMarketsDay EnQuestDocument88 pages151208CapitalMarketsDay EnQuestredevils86No ratings yet

- Financial Model SampleDocument8 pagesFinancial Model SamplekaajitkumarNo ratings yet

- Broadband Services: Business Models and Technologies for Community NetworksFrom EverandBroadband Services: Business Models and Technologies for Community NetworksImrich ChlamtacNo ratings yet

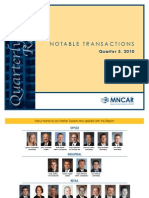

- MNCAR Notable Commercial Real Estate Transactions Q3 2010Document9 pagesMNCAR Notable Commercial Real Estate Transactions Q3 2010Jason SandquistNo ratings yet

- MNCAR 2012 Annual Market ReportDocument16 pagesMNCAR 2012 Annual Market ReportJason SandquistNo ratings yet

- MNCAR Notable Transactions Q2Document5 pagesMNCAR Notable Transactions Q2Jason SandquistNo ratings yet

- MNCAR Notable Transactions Quarter 1 2010Document5 pagesMNCAR Notable Transactions Quarter 1 2010Jason SandquistNo ratings yet

- Minneapolis Industrial ReportDocument35 pagesMinneapolis Industrial ReportJason SandquistNo ratings yet

- 2009 Real Estate Residential Activity ReportDocument18 pages2009 Real Estate Residential Activity ReportJason SandquistNo ratings yet

- Minneapolis 100Document3 pagesMinneapolis 100Jason SandquistNo ratings yet

- Twin Cities Foreclosures & Short Sales Ocotober 2009Document10 pagesTwin Cities Foreclosures & Short Sales Ocotober 2009Jason SandquistNo ratings yet

- Twin Cities Foreclosure & Short Sale Report 2009 Q3Document8 pagesTwin Cities Foreclosure & Short Sale Report 2009 Q3Jason SandquistNo ratings yet

- MNHOC Foreclosures in Minnesota 1st Half 2009Document35 pagesMNHOC Foreclosures in Minnesota 1st Half 2009Jason SandquistNo ratings yet

- Foreclosures and Short SalesDocument5 pagesForeclosures and Short SalesJason SandquistNo ratings yet

- La Consolacion College-Arfien DepartmentDocument2 pagesLa Consolacion College-Arfien DepartmentmikokeeNo ratings yet

- Friday Foreclosure List For Pierce County, Washington Including Tacoma, Gig Harbor, Puyallup, Bank Owned Homes For SaleDocument13 pagesFriday Foreclosure List For Pierce County, Washington Including Tacoma, Gig Harbor, Puyallup, Bank Owned Homes For SaleTom TuttleNo ratings yet

- Habtamu Budjet Hamele 01' 2009 - Sene 30'2010 HabtamuDocument5 pagesHabtamu Budjet Hamele 01' 2009 - Sene 30'2010 HabtamuAbelNo ratings yet

- Real Property Mini Review Lecture Slides in PictureDocument56 pagesReal Property Mini Review Lecture Slides in PictureMira HsieNo ratings yet

- Slab CycleDocument1 pageSlab CycleshardultagalpallewarNo ratings yet

- AESMT3Document5 pagesAESMT3Nova nbNo ratings yet

- Underwriting Training - CollateralDocument60 pagesUnderwriting Training - CollateralHimani SachdevNo ratings yet

- Land Sale AgreementDocument3 pagesLand Sale Agreementtkvimal100% (1)

- 2015 Alabama Tenants' HandbookDocument28 pages2015 Alabama Tenants' HandbookBen CulpepperNo ratings yet

- Contemporary Nigerian Residential ArchitectureDocument46 pagesContemporary Nigerian Residential ArchitectureSamuel Hugos100% (1)

- BoQ For Water TankDocument10 pagesBoQ For Water TankMenaka GurusingheNo ratings yet

- Bear Stearns Bear Stearns Quick Guide To NonAgency Mortgage Back SecuritiesDocument104 pagesBear Stearns Bear Stearns Quick Guide To NonAgency Mortgage Back Securitiesdshen1No ratings yet

- MI VIDA Brochure .22 RDDocument18 pagesMI VIDA Brochure .22 RDJoe WaigwaNo ratings yet

- Beta Plus Books On Interior DesignDocument4 pagesBeta Plus Books On Interior DesignACC DistributionNo ratings yet

- Bison Hollowcore Floors Bearing DetailsDocument4 pagesBison Hollowcore Floors Bearing DetailsAhmadNo ratings yet

- UNIVERSITY OF LAGOS Project PlaningDocument10 pagesUNIVERSITY OF LAGOS Project PlaningEmmanuelNo ratings yet

- Addenda Short SaleDocument2 pagesAddenda Short SaleAndrew WeintraubNo ratings yet

- "Go Dark" Provisions in Retail Leases The Commercial Leasing Law BlogDocument5 pages"Go Dark" Provisions in Retail Leases The Commercial Leasing Law BlogothergregNo ratings yet

- Consents Conveyancing Notes - HandoutDocument32 pagesConsents Conveyancing Notes - HandoutReal TrekstarNo ratings yet

- DEED OF ABSOLUTE SALE - EquipmentDocument3 pagesDEED OF ABSOLUTE SALE - EquipmentEloisa Moaje AtienzaNo ratings yet

- Tax ListDocument480 pagesTax ListSTACY BEARDNo ratings yet

- Authorization To ExcludeDocument1 pageAuthorization To ExcludealphaformsNo ratings yet

- Cruz Vs Filipinas InvestmentDocument2 pagesCruz Vs Filipinas InvestmentSaji JimenoNo ratings yet

- ( 126) Merger.: 3. ( 126) Merger., 4 Witkin, Summary 11th Sec Trans - Real 126 (2021)Document2 pages( 126) Merger.: 3. ( 126) Merger., 4 Witkin, Summary 11th Sec Trans - Real 126 (2021)AJNo ratings yet

- PSB Vs LantinDocument1 pagePSB Vs LantinkimuchosNo ratings yet

- Status of Civil Submittals (Sama Energy) (Neom)Document3 pagesStatus of Civil Submittals (Sama Energy) (Neom)sachin francisNo ratings yet