You might also like

- RR 4-2007Document23 pagesRR 4-2007arloNo ratings yet

- VAT Regulations AmendmentsDocument4 pagesVAT Regulations AmendmentsKristel Anne LiwagNo ratings yet

- Bir RR 4-2007Document54 pagesBir RR 4-2007Mae JustineNo ratings yet

- RR No. 4-07Document24 pagesRR No. 4-07LRBNo ratings yet

- Amend VAT RegulationsDocument17 pagesAmend VAT RegulationsRavenclaws91No ratings yet

- RR 16-05Document32 pagesRR 16-05matinikki100% (1)

- Revenue Regulation No. 16-05Document62 pagesRevenue Regulation No. 16-05Raymond Atanacio100% (1)

- Rev. Regs. 16-2005Document55 pagesRev. Regs. 16-2005makimillianNo ratings yet

- Updated Rules On VatDocument42 pagesUpdated Rules On VatLuis de leonNo ratings yet

- RR 14-2005-VatDocument68 pagesRR 14-2005-VatEmil A. MolinaNo ratings yet

- RR 16-2005Document55 pagesRR 16-2005Mark Lester Lee AureNo ratings yet

- Revenue Regulations No. 16-05: September 1, 2005Document69 pagesRevenue Regulations No. 16-05: September 1, 2005Emil A. MolinaNo ratings yet

- Revenue Regulation No. 16-2005Document0 pagesRevenue Regulation No. 16-2005Kaye MendozaNo ratings yet

- BIR Revenue Regulations, Circular - VATDocument97 pagesBIR Revenue Regulations, Circular - VATFredrick FernandezNo ratings yet

- rr16-2005 2Document55 pagesrr16-2005 2Kobe Lawrence VeneracionNo ratings yet

- Vat On Sale of Goods or PropertiesDocument7 pagesVat On Sale of Goods or Propertiesnohair100% (3)

- Revenue Regulations No. 16-2005 (Digest)Document19 pagesRevenue Regulations No. 16-2005 (Digest)JERepaldoNo ratings yet

- RR No. 16-05Document71 pagesRR No. 16-05LRBNo ratings yet

- REVENUE REGULATIONS NO. 16-2005 Issued On October 19, 2005 Prescribes TheDocument2 pagesREVENUE REGULATIONS NO. 16-2005 Issued On October 19, 2005 Prescribes TheJennilyn TugelidaNo ratings yet

- RR 7-95 Consolidated VATDocument64 pagesRR 7-95 Consolidated VATjankriezlNo ratings yet

- RR No.16-05Document69 pagesRR No.16-05Danzki BadiqueNo ratings yet

- Lot Acquisition TaxesDocument29 pagesLot Acquisition TaxesShaira FaithNo ratings yet

- Tax UpdatesDocument19 pagesTax UpdatesYeoh MaeNo ratings yet

- Characteristic of Vat-Business TaxationDocument8 pagesCharacteristic of Vat-Business TaxationAthena LouiseNo ratings yet

- VAT ON SALES OF GOODS A 12Document48 pagesVAT ON SALES OF GOODS A 12Ivan Jester BautistaNo ratings yet

- Taxation On Sale of Real PropertiesDocument9 pagesTaxation On Sale of Real PropertiesIsaac CursoNo ratings yet

- RR 16-2005 Amended (Consolidated VAT Regulations)Document83 pagesRR 16-2005 Amended (Consolidated VAT Regulations)Genny JovellanosNo ratings yet

- RR 16-2005Document9 pagesRR 16-2005mblopez1No ratings yet

- Mcit and CWTDocument5 pagesMcit and CWTOlan Dave LachicaNo ratings yet

- BIR Ruling 27-02Document2 pagesBIR Ruling 27-02erikagcv100% (1)

- Value Added TaxDocument44 pagesValue Added TaxDa Yani ChristeeneNo ratings yet

- Updated RR 2-98 Sec 2.57.1 (J) Individual Real Property - Ordinary AssetDocument4 pagesUpdated RR 2-98 Sec 2.57.1 (J) Individual Real Property - Ordinary AssetJaymar DetoitoNo ratings yet

- Real Estate Sale Taxes ExplainedDocument7 pagesReal Estate Sale Taxes ExplainedJessa CaberteNo ratings yet

- BarterDocument2 pagesBarterRester NonatoNo ratings yet

- Creditable Withholding Tax ReviewerDocument6 pagesCreditable Withholding Tax ReviewerMark Rainer Yongis LozaresNo ratings yet

- 04.1 S4 VAT PPT AquinoDocument112 pages04.1 S4 VAT PPT Aquinosaeloun hrdNo ratings yet

- TaxDocument6 pagesTaxmgpadillaNo ratings yet

- Value Added TaxationDocument76 pagesValue Added Taxationxz wyNo ratings yet

- 3 VatDocument95 pages3 VatGileah ZuasolaNo ratings yet

- VATDocument17 pagesVATnodnel salonNo ratings yet

- Bsa2105 FS2021 Vat Da22414Document4 pagesBsa2105 FS2021 Vat Da22414ela kikay100% (1)

- VAT Codal and RegulationsDocument6 pagesVAT Codal and RegulationsVictor LimNo ratings yet

- Taxes in Real Estate SaleDocument5 pagesTaxes in Real Estate SaleJorgeNo ratings yet

- VAT Explained: Coverage, Rates, and TaxpayersDocument33 pagesVAT Explained: Coverage, Rates, and TaxpayersKiro ParafrostNo ratings yet

- Antonio, Gladys C. Bagon, Jaleen Anne A. Lapura, MelgenDocument22 pagesAntonio, Gladys C. Bagon, Jaleen Anne A. Lapura, MelgenJayvee FelipeNo ratings yet

- Real Estate Taxation - Transfer of PropertyDocument9 pagesReal Estate Taxation - Transfer of PropertyJuan FrivaldoNo ratings yet

- RR 8-98Document3 pagesRR 8-98matinikkiNo ratings yet

- Quick Notes Real Estate TaxationDocument3 pagesQuick Notes Real Estate TaxationJoshelle B. Bancilo100% (1)

- 10 42 Vat at GlanceDocument19 pages10 42 Vat at Glanceemmanuel JohnyNo ratings yet

- Input VAT: Understanding the BasicsDocument10 pagesInput VAT: Understanding the BasicsPineda, Paula MarieNo ratings yet

- ACC311 3rd Exam CoverageDocument108 pagesACC311 3rd Exam CoverageHilarie JeanNo ratings yet

- VALUE Added TaxDocument20 pagesVALUE Added TaxMadz Rj MangorobongNo ratings yet

- Chapter 7 - Regular Output VATDocument17 pagesChapter 7 - Regular Output VATSelene DimlaNo ratings yet

- Chapter 17Document10 pagesChapter 17Neriza maningasNo ratings yet

- Bustax Chapter 7Document10 pagesBustax Chapter 7Pineda, Paula MarieNo ratings yet

- Bar Review Companion: Taxation: Anvil Law Books Series, #4From EverandBar Review Companion: Taxation: Anvil Law Books Series, #4No ratings yet

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- Tax Sales for Rookies: A Beginner’s Guide to Understanding Property Tax SalesFrom EverandTax Sales for Rookies: A Beginner’s Guide to Understanding Property Tax SalesNo ratings yet

- Family Member ChartDocument1 pageFamily Member CharthirohonmaNo ratings yet

- FDA Circular NO. 2014-022Document1 pageFDA Circular NO. 2014-022hirohonmaNo ratings yet

- FDA Advisory No. 2014-075Document1 pageFDA Advisory No. 2014-075hirohonmaNo ratings yet

- CHRP Working PaperDocument22 pagesCHRP Working Paper500daysNo ratings yet

- Belgium CaseDocument47 pagesBelgium CasehirohonmaNo ratings yet

- Police Power and Eminent Domain Cases Full TextDocument205 pagesPolice Power and Eminent Domain Cases Full TextAldwin Dhon MartelNo ratings yet

- Tax Refund Denied for Lack of Official ReceiptsDocument2 pagesTax Refund Denied for Lack of Official ReceiptsDianne Bernadeth Cos-agon100% (1)

- Robinsons GalleriaDocument14 pagesRobinsons GalleriaKathleen Mae del RosarioNo ratings yet

- CV NMTC ApplicationDocument8 pagesCV NMTC ApplicationStephen GallutiaNo ratings yet

- 2014 Global Automotive Tax GuideDocument577 pages2014 Global Automotive Tax Guideriki187No ratings yet

- Study: Understanding Why So Many Corporations Do Not Pay Illinois Corporate Income TaxDocument57 pagesStudy: Understanding Why So Many Corporations Do Not Pay Illinois Corporate Income TaxZoe GallandNo ratings yet

- CBK V CIRDocument7 pagesCBK V CIRAna BelleNo ratings yet

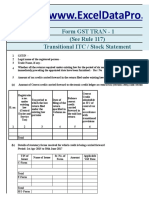

- GST TRAN 1 Return Excel TemplateDocument14 pagesGST TRAN 1 Return Excel TemplateRaju Ranjan KumarNo ratings yet

- Possibilities in Taxation For 2016 Mock Bar and Beyond - Atty. Roberto Bobby LockDocument74 pagesPossibilities in Taxation For 2016 Mock Bar and Beyond - Atty. Roberto Bobby LockHilikus IncubusNo ratings yet

- Interstate and Intrastate Transactions Under GSTDocument11 pagesInterstate and Intrastate Transactions Under GSTD.Naga RajuNo ratings yet

- CCH Federal TaxationDocument14 pagesCCH Federal Taxation50shadesofjohnNo ratings yet

- Comm vs. Central Luzon 456 SCRA 414Document21 pagesComm vs. Central Luzon 456 SCRA 414Jacinto Jr Jamero100% (1)

- Commissioner of Internal Revenue vs. Central Luzon Drug Corp.Document42 pagesCommissioner of Internal Revenue vs. Central Luzon Drug Corp.Daryll AsuncionNo ratings yet

- What You Need To Know For Tax Season 2023 - ReviewDocument34 pagesWhat You Need To Know For Tax Season 2023 - ReviewJagmohan TeamentigrityNo ratings yet

- Print Preview - Preliminary Application: Project DescriptionDocument21 pagesPrint Preview - Preliminary Application: Project DescriptionRyan SloanNo ratings yet

- Tax DigestDocument7 pagesTax DigestLeo Angelo LuyonNo ratings yet

- Monthly VAT ReturnDocument34 pagesMonthly VAT ReturnEdris MatovuNo ratings yet

- Bir Form 2307 2307Document12 pagesBir Form 2307 2307Edwin Siruno LopezNo ratings yet

- CIR Vs Philam Life G.R. No. 175124Document5 pagesCIR Vs Philam Life G.R. No. 175124Ian Kenneth MangkitNo ratings yet

- Zero-rated sales and VAT exemptions under TRAINDocument3 pagesZero-rated sales and VAT exemptions under TRAINMarionne GNo ratings yet

- The History of Leasing: by Jeffrey TaylorDocument18 pagesThe History of Leasing: by Jeffrey TaylorWedi TassewNo ratings yet

- 09 Foreign Tax Credit Foreign LossesDocument7 pages09 Foreign Tax Credit Foreign LossesTayyaba YounasNo ratings yet

- Module 2 Transcript Federal Taxation I Individuals Employees and Sole ProprietorsDocument66 pagesModule 2 Transcript Federal Taxation I Individuals Employees and Sole ProprietorsFreddy MolinaNo ratings yet

- 1701a - Page 2Document1 page1701a - Page 2Sygee BotantanNo ratings yet

- Tax Credits Applicable To Individuals - Zimbabwe Revenue Authority (ZIMRA)Document2 pagesTax Credits Applicable To Individuals - Zimbabwe Revenue Authority (ZIMRA)rodgington duneNo ratings yet

- 3/B Canal Bank Extension Mughalpura Hammad Khan: Declaration Acknowledgement Slip Name: AddressDocument4 pages3/B Canal Bank Extension Mughalpura Hammad Khan: Declaration Acknowledgement Slip Name: AddressHammad KhanNo ratings yet

- United Way Annual Report 2009Document28 pagesUnited Way Annual Report 2009traci_wickettNo ratings yet

- CTA upholds imprinting of "zero-ratedDocument12 pagesCTA upholds imprinting of "zero-ratedAnonymous gmZPbEvFdENo ratings yet

- Read Neal's LetterDocument2 pagesRead Neal's Letterkballuck1No ratings yet

- Patriot PayDocument1 pagePatriot PayAdam ForgieNo ratings yet