You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Final General Awareness Capsule For SSC 2017 CGL PDFDocument123 pagesFinal General Awareness Capsule For SSC 2017 CGL PDFTiffany PriceNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- All SSC CPO 2018 Papers (WWW - Qmaths.in) PDFDocument680 pagesAll SSC CPO 2018 Papers (WWW - Qmaths.in) PDFJITENDER WADHWANo ratings yet

- June - 2017 Daily Vocab The Hindu EditorialDocument25 pagesJune - 2017 Daily Vocab The Hindu EditorialTiffany PriceNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- NCERT Solutions For Class 7 Geography Freehomedelivery - Net CH 1 5Document23 pagesNCERT Solutions For Class 7 Geography Freehomedelivery - Net CH 1 5Tiffany PriceNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- 1500+ One Words Substitution (WWW - Qmaths.in)Document41 pages1500+ One Words Substitution (WWW - Qmaths.in)Anonymous 49Kxx7zqX100% (1)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Global WarmingDocument6 pagesGlobal WarmingTiffany PriceNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- RSA Public Key Cryptosystem: Rivest, Shamir, Adleman)Document8 pagesRSA Public Key Cryptosystem: Rivest, Shamir, Adleman)Tiffany PriceNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- SAP Shortcut Keys PDFDocument5 pagesSAP Shortcut Keys PDFHarish KumarNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- SSC Question BankDocument77 pagesSSC Question BankTiffany PriceNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Ss Bharti PDFDocument400 pagesSs Bharti PDFTiffany Price100% (1)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Question Paper - HSSC .27Document8 pagesQuestion Paper - HSSC .27Tiffany PriceNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Cryptography HistoryDocument14 pagesCryptography HistoryTiffany PriceNo ratings yet

- ShortkeysDocument1 pageShortkeysTiffany PriceNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- CCC Book (Course of Computer Concept)Document159 pagesCCC Book (Course of Computer Concept)Dinesh Patdia94% (34)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- IJSER TemplateDocument5 pagesIJSER TemplateTiffany PriceNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The RSA AlgorithmDocument31 pagesThe RSA AlgorithmbyprasadNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The RSA AlgorithmDocument31 pagesThe RSA AlgorithmbyprasadNo ratings yet

- Kanak Speaker Recognition IjrDocument6 pagesKanak Speaker Recognition IjrTiffany PriceNo ratings yet

- Capsule For Sbi Po Mainsrrbrbi Assistant 2015 UpdatedDocument55 pagesCapsule For Sbi Po Mainsrrbrbi Assistant 2015 UpdatedSoumya RanjanNo ratings yet

- Class X ScienceDocument19 pagesClass X ScienceCgpscAspirantNo ratings yet

- Report For ThesisDocument58 pagesReport For ThesisTiffany PriceNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Cryptography HistoryDocument14 pagesCryptography HistoryTiffany PriceNo ratings yet

- 9 EnhanceDocument9 pages9 EnhanceTiffany PriceNo ratings yet

- SSC 74Document22 pagesSSC 74Tiffany PriceNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- GK Power Capsule Sbi Asso Assistant 2015Document56 pagesGK Power Capsule Sbi Asso Assistant 2015Prakash PudipeddiNo ratings yet

- Scalability of A Mobile Agents Based Network Management ApplicationDocument8 pagesScalability of A Mobile Agents Based Network Management ApplicationTiffany PriceNo ratings yet

- UGC NET Electronic Science Paper II Jun 05Document12 pagesUGC NET Electronic Science Paper II Jun 05Tiffany PriceNo ratings yet

- 1Document5 pages1Tiffany Price100% (1)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (120)

- Image Encryption and Decryption Using Symmetric Key in MatlabDocument4 pagesImage Encryption and Decryption Using Symmetric Key in MatlabTiffany PriceNo ratings yet

- Xxxxxx263 Aug 21Document5 pagesXxxxxx263 Aug 21Batthula SandeepNo ratings yet

- IFS - B.com End Sem. Que. Paper PDFDocument4 pagesIFS - B.com End Sem. Que. Paper PDFpranav2411No ratings yet

- BBPS - Agent Institution FormDocument2 pagesBBPS - Agent Institution FormSatya Rani LakkojuNo ratings yet

- Credit and Debit CardsDocument23 pagesCredit and Debit CardsRaihana Karolly100% (1)

- Secretary's Certificate (ATOMTECH)Document1 pageSecretary's Certificate (ATOMTECH)Gelyn OconerNo ratings yet

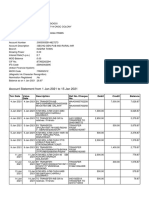

- Account Statement From 1 Jan 2021 To 15 Jan 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument2 pagesAccount Statement From 1 Jan 2021 To 15 Jan 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balanceabhijit gogoiNo ratings yet

- Hand Book On Know Your Circular Andhra Bank PromotionDocument81 pagesHand Book On Know Your Circular Andhra Bank PromotionSubrat Satyaranjan KanungoNo ratings yet

- Global Risk ManagementDocument76 pagesGlobal Risk ManagementMarcoGarcesNo ratings yet

- Citi Bank 2021 StatementsDocument2 pagesCiti Bank 2021 StatementsJohn call67% (3)

- s5 PDFDocument5 pagess5 PDFKeshav KumarNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Npa Policy PDFDocument21 pagesNpa Policy PDFravi kumarNo ratings yet

- Acct Statement XX7809 31032023Document6 pagesAcct Statement XX7809 31032023harshal jagtapNo ratings yet

- Financial Performance of Kist BankDocument14 pagesFinancial Performance of Kist BankDeepesh SharmaNo ratings yet

- Account - Statement - 011222 - 010323Document69 pagesAccount - Statement - 011222 - 010323Raja BabuNo ratings yet

- Comprehensive Project ReportDocument13 pagesComprehensive Project ReportRishi KanjaniNo ratings yet

- REportDocument20 pagesREportPrashant MahawarNo ratings yet

- Banking Laws Final Examinations: Instruments (Iuis)Document2 pagesBanking Laws Final Examinations: Instruments (Iuis)Patrick D GuetaNo ratings yet

- TVR Format - Shrikrushn Namdev Kavar - TF4343554Document19 pagesTVR Format - Shrikrushn Namdev Kavar - TF4343554Nikhil MohaneNo ratings yet

- Midland Bank PDFDocument1 pageMidland Bank PDFMST HAZERA KHATUNNo ratings yet

- Baking CH 2Document5 pagesBaking CH 2Endalkachew BefirdeNo ratings yet

- Goldman Sachs Apple Card Customer AgreementDocument15 pagesGoldman Sachs Apple Card Customer AgreementJack PurcherNo ratings yet

- Customer Request FormDocument1 pageCustomer Request Formrautakshay279No ratings yet

- Problem Session-2 - 15.03.2012Document44 pagesProblem Session-2 - 15.03.2012markydee_20No ratings yet

- RDInstallmentReport12 01 2024Document4 pagesRDInstallmentReport12 01 2024Khushal TembhekarNo ratings yet

- Mba M2a ChitrakshDocument125 pagesMba M2a ChitrakshAnkush SharmaNo ratings yet

- Vdocuments - MX Internship Report of Js Bank LTDDocument36 pagesVdocuments - MX Internship Report of Js Bank LTDShaikh JibranNo ratings yet

- 445pm Eric WadeDocument43 pages445pm Eric WadeqiuNo ratings yet

- Demonetization FinalDocument10 pagesDemonetization FinalShivani JadhavNo ratings yet

- Time Value of MoneyDocument40 pagesTime Value of MoneyAhmedmughalNo ratings yet

- Ready, Set, Growth hack:: A beginners guide to growth hacking successFrom EverandReady, Set, Growth hack:: A beginners guide to growth hacking successRating: 4.5 out of 5 stars4.5/5 (93)

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNFrom Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNRating: 4.5 out of 5 stars4.5/5 (3)

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingFrom EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingRating: 4.5 out of 5 stars4.5/5 (17)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 4.5 out of 5 stars4.5/5 (14)

- Value: The Four Cornerstones of Corporate FinanceFrom EverandValue: The Four Cornerstones of Corporate FinanceRating: 4.5 out of 5 stars4.5/5 (18)

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursFrom EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursRating: 4.5 out of 5 stars4.5/5 (8)