You might also like

- Why Moats Matter: The Morningstar Approach to Stock InvestingFrom EverandWhy Moats Matter: The Morningstar Approach to Stock InvestingRating: 4 out of 5 stars4/5 (3)

- Icahn Enterprises - May 2015 Investor PresentationDocument41 pagesIcahn Enterprises - May 2015 Investor PresentationCanadianValue100% (2)

- Investment Banking Investment Banking2122Document16 pagesInvestment Banking Investment Banking2122vishal13889100% (2)

- Pwc-Guide-Foreign-CurrencyDocument134 pagesPwc-Guide-Foreign-CurrencyJoaquim SousaNo ratings yet

- Protect Your Assets: Strategically Oriented, Metrics-Centered Credit ManagementFrom EverandProtect Your Assets: Strategically Oriented, Metrics-Centered Credit ManagementNo ratings yet

- DIVIDEND INVESTING: Maximizing Returns while Minimizing Risk through Selective Stock Selection and Diversification (2023 Guide for Beginners)From EverandDIVIDEND INVESTING: Maximizing Returns while Minimizing Risk through Selective Stock Selection and Diversification (2023 Guide for Beginners)No ratings yet

- Pershing Square Management's Letter To InvestorsDocument7 pagesPershing Square Management's Letter To InvestorsDealBook100% (1)

- Aspeon Sparkling Water, Inc. Capital Structure Policy: Case 10Document16 pagesAspeon Sparkling Water, Inc. Capital Structure Policy: Case 10Alla LiNo ratings yet

- 10 Top Gold Trading TipsDocument11 pages10 Top Gold Trading Tipszulfikar Salim100% (8)

- International Corporate FinanceDocument380 pagesInternational Corporate FinanceBiju GeorgeNo ratings yet

- CFPB Sample Revocation Letter To Your Bank or Credit UnionDocument2 pagesCFPB Sample Revocation Letter To Your Bank or Credit UnionkongbengNo ratings yet

- CFPB Sample Revocation Letter To Your Bank or Credit UnionDocument2 pagesCFPB Sample Revocation Letter To Your Bank or Credit UnionkongbengNo ratings yet

- 1Q12 Investor InformationDocument58 pages1Q12 Investor Informationvishan_sharmaNo ratings yet

- Dividend Growth Investing: The Ultimate Investing Guide. Learn Effective Strategies to Create Passive Income for Your Future.From EverandDividend Growth Investing: The Ultimate Investing Guide. Learn Effective Strategies to Create Passive Income for Your Future.No ratings yet

- Completed Chapter 5 Mini Case Working Papers Fa14Document12 pagesCompleted Chapter 5 Mini Case Working Papers Fa14Gauri KarkhanisNo ratings yet

- DeluxeDocument4 pagesDeluxeshielamaeNo ratings yet

- BBBY Case ExerciseDocument7 pagesBBBY Case ExerciseSue McGinnisNo ratings yet

- Reliance Capital - Initiating Coverage - Centrum 06122012Document19 pagesReliance Capital - Initiating Coverage - Centrum 06122012nit111No ratings yet

- CH 13 ActivityDocument3 pagesCH 13 Activityapi-24960437850% (2)

- M&A CaseDocument5 pagesM&A CaseRashleen AroraNo ratings yet

- Trend Analysis NewDocument3 pagesTrend Analysis Newgr82b_b2bNo ratings yet

- Fin420.540 Jan 2018 Q2-5Document8 pagesFin420.540 Jan 2018 Q2-5Amar AzuanNo ratings yet

- Hill CountryDocument8 pagesHill CountryAtif Raza AkbarNo ratings yet

- Agricultural Bank of ChinaDocument7 pagesAgricultural Bank of ChinaJack YuanNo ratings yet

- How to Retire Early on Dividends: Dividend Growth Machine: Mastering the Art of Maximizing Returns Through Dividend InvestingFrom EverandHow to Retire Early on Dividends: Dividend Growth Machine: Mastering the Art of Maximizing Returns Through Dividend InvestingNo ratings yet

- Best Day Trading Strategies and Secrets For Beginners - ForexBoat PDFDocument9 pagesBest Day Trading Strategies and Secrets For Beginners - ForexBoat PDFctanghamNo ratings yet

- Export Negotiation Collection Schedule-2015Document1 pageExport Negotiation Collection Schedule-2015kongbengNo ratings yet

- Citigroup Inc: Stock Report - May 7, 2016 - NYS Symbol: C - C Is in The S&P 500Document11 pagesCitigroup Inc: Stock Report - May 7, 2016 - NYS Symbol: C - C Is in The S&P 500Luis Fernando EscobarNo ratings yet

- The Blacker The Berry, The Sweeter The Juice: Management Guidance 270Document3 pagesThe Blacker The Berry, The Sweeter The Juice: Management Guidance 270maxmueller15No ratings yet

- JP Morgan 8.02.13 PDFDocument9 pagesJP Morgan 8.02.13 PDFChad Thayer VNo ratings yet

- Warren Buffett Presentation v3Document25 pagesWarren Buffett Presentation v3Sisi Ye50% (2)

- A View On Banks FinalDocument22 pagesA View On Banks FinaljustinsofoNo ratings yet

- Acm Dew An Housing Acc 08dec10Document7 pagesAcm Dew An Housing Acc 08dec10Abhi ChoudharyNo ratings yet

- Bac Zack HoldDocument9 pagesBac Zack HoldsinnlosNo ratings yet

- 2022 Q2 BAM LTR To Shareholders FF BDocument8 pages2022 Q2 BAM LTR To Shareholders FF BDan-S. ErmicioiNo ratings yet

- Stock Research Report For HBC As of 8/17/11 - Chaikin Power ToolsDocument4 pagesStock Research Report For HBC As of 8/17/11 - Chaikin Power ToolsChaikin Analytics, LLCNo ratings yet

- Annual Report Avenue CapitalDocument44 pagesAnnual Report Avenue CapitalJoel CintrónNo ratings yet

- Citi Report CIBCDocument23 pagesCiti Report CIBCinchoatehereNo ratings yet

- GI Report February 2012Document3 pagesGI Report February 2012Bill HallmanNo ratings yet

- CI Signature Dividend FundDocument2 pagesCI Signature Dividend Fundkirby333No ratings yet

- Managing Member - Tim Eriksen Eriksen Capital Management, LLC 567 Wildrose Cir., Lynden, WA 98264Document7 pagesManaging Member - Tim Eriksen Eriksen Capital Management, LLC 567 Wildrose Cir., Lynden, WA 98264Matt EbrahimiNo ratings yet

- Aetna Inc.: (Source S&P, Vickers, Company Reports)Document10 pagesAetna Inc.: (Source S&P, Vickers, Company Reports)sinnlosNo ratings yet

- 2014 Dow Annual Report With 10K PDFDocument186 pages2014 Dow Annual Report With 10K PDFKatia LoarteNo ratings yet

- GuggenheimDocument5 pagesGuggenheimRochester Democrat and ChronicleNo ratings yet

- Artko Capital 2018 Q4 LetterDocument9 pagesArtko Capital 2018 Q4 LetterSmitty WNo ratings yet

- Coho Capital 2017 Q4 LetterDocument5 pagesCoho Capital 2017 Q4 LetterPaul AsselinNo ratings yet

- Asteri Capital (Glencore)Document4 pagesAsteri Capital (Glencore)Brett Reginald ScottNo ratings yet

- Olam Dismisses Muddy Waters Report FindingsDocument45 pagesOlam Dismisses Muddy Waters Report Findingsstoreroom_02No ratings yet

- BNP Paribas Mid Cap Fund: Young Spark Today. Grandmaster TomorrowDocument2 pagesBNP Paribas Mid Cap Fund: Young Spark Today. Grandmaster TomorrowPrasad Dhondiram Zinjurde PatilNo ratings yet

- Stock Research Report For DISH As of 7/27/11 - Chaikin Power ToolsDocument4 pagesStock Research Report For DISH As of 7/27/11 - Chaikin Power ToolsChaikin Analytics, LLCNo ratings yet

- HFAC Annual Report 2013Document12 pagesHFAC Annual Report 2013thevariantviewNo ratings yet

- Cvs FinalpapermaheshDocument15 pagesCvs Finalpapermaheshnaikm3239No ratings yet

- BloombergBrief HF Newsletter 201458Document12 pagesBloombergBrief HF Newsletter 201458Himanshu GoyalNo ratings yet

- Berkshire Hathaway Research PaperDocument8 pagesBerkshire Hathaway Research PaperDennis KimNo ratings yet

- Market Outlook 12th March 2012Document4 pagesMarket Outlook 12th March 2012Angel BrokingNo ratings yet

- JPM Weekly Commentary 01-09-12Document2 pagesJPM Weekly Commentary 01-09-12Flat Fee PortfoliosNo ratings yet

- Aviva PLC Investor and Analyst Update 5 July 2012Document45 pagesAviva PLC Investor and Analyst Update 5 July 2012Aviva GroupNo ratings yet

- 018 - BoA 2008 - ARDocument195 pages018 - BoA 2008 - ARelivislivesNo ratings yet

- Emp Capital Partners - 4Q12 Investor LetterDocument7 pagesEmp Capital Partners - 4Q12 Investor LetterLuis AhumadaNo ratings yet

- FAPDocument12 pagesFAPAnokye AdamNo ratings yet

- 6 ChapterDocument11 pages6 ChapterAbdullah Al MahmudNo ratings yet

- MFC 4Q15 PRDocument48 pagesMFC 4Q15 PRÁi PhươngNo ratings yet

- Submitted by Ramesh Babu Sadda (2895538) : Word Count: 2800Document18 pagesSubmitted by Ramesh Babu Sadda (2895538) : Word Count: 2800Ramesh BabuNo ratings yet

- Finance QuestionsDocument6 pagesFinance QuestionsCream FamilyNo ratings yet

- Brookfield Asset Management q2 2013 Letter To ShareholdersDocument6 pagesBrookfield Asset Management q2 2013 Letter To ShareholdersCanadianValueNo ratings yet

- Arquitos Capital Management - Q3 2014 Investor LetterDocument4 pagesArquitos Capital Management - Q3 2014 Investor LetterCanadianValueNo ratings yet

- Chapter 06Document25 pagesChapter 06Farjana Hossain DharaNo ratings yet

- Discussion Forum Unit 8Document34 pagesDiscussion Forum Unit 8Eyad AbdullahNo ratings yet

- Financial Statements AnalysisDocument9 pagesFinancial Statements AnalysisDevanganaNo ratings yet

- An Investment Journey II The Essential Tool Kit: Building A Successful Portfolio With Stock FundamentalsFrom EverandAn Investment Journey II The Essential Tool Kit: Building A Successful Portfolio With Stock FundamentalsNo ratings yet

- LOIDocument1 pageLOIVinci PoncardasNo ratings yet

- He Usantara Anifesto: #L U C CDocument40 pagesHe Usantara Anifesto: #L U C CWan Hadi Wan ZainalNo ratings yet

- Pengaruh Torefaksi Terhadap Sifat Kimia Pelet TandDocument8 pagesPengaruh Torefaksi Terhadap Sifat Kimia Pelet TandkongbengNo ratings yet

- Destination: Innovation For YourDocument4 pagesDestination: Innovation For YourkongbengNo ratings yet

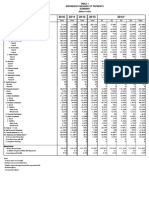

- Items 2010 2011 2012 2013 2014 : (Millions of USD)Document12 pagesItems 2010 2011 2012 2013 2014 : (Millions of USD)kongbengNo ratings yet

- K 112Document2 pagesK 112kongbengNo ratings yet

- Press Release Saratoga 9M2015Document3 pagesPress Release Saratoga 9M2015kongbengNo ratings yet

- Negative Net Resource Transfers As A Minskyian Hedge Profile and The Stability of The International Financial SystemDocument13 pagesNegative Net Resource Transfers As A Minskyian Hedge Profile and The Stability of The International Financial SystemkongbengNo ratings yet

- Employment AgreementDocument9 pagesEmployment AgreementkongbengNo ratings yet

- Appendix 7 Pa ContractDocument5 pagesAppendix 7 Pa ContractkongbengNo ratings yet

- Porsche DownloadDocument14 pagesPorsche DownloadkongbengNo ratings yet

- Notice of Payment: Court DetailsDocument1 pageNotice of Payment: Court DetailskongbengNo ratings yet

- From TO Asat (: Balance Sheet Information Profit & Loss InformationDocument1 pageFrom TO Asat (: Balance Sheet Information Profit & Loss InformationkongbengNo ratings yet

- YC Form SaaS AgreementDocument10 pagesYC Form SaaS AgreementYan BaglieriNo ratings yet

- Avtest Summary Homeuser 2017-06Document18 pagesAvtest Summary Homeuser 2017-06kongbengNo ratings yet

- Template BulletDocument1 pageTemplate BulletccllNo ratings yet

- Sample Org ContractDocument3 pagesSample Org ContractEmma FarcasNo ratings yet

- Airbus Gcs EbsDocument5 pagesAirbus Gcs EbskongbengNo ratings yet

- End User CertificateDocument2 pagesEnd User CertificatekongbengNo ratings yet

- Company Profile - Apple - Q4 2012Document2 pagesCompany Profile - Apple - Q4 2012kongbengNo ratings yet

- Press Release Saratoga 9M2015Document3 pagesPress Release Saratoga 9M2015kongbengNo ratings yet

- OneCare Global Extended Warranty Pricesheet 0117Document1 pageOneCare Global Extended Warranty Pricesheet 0117kongbengNo ratings yet

- Conger - Necessary Art of Persuasion PDFDocument12 pagesConger - Necessary Art of Persuasion PDFkongbengNo ratings yet

- Porsche DownloadDocument14 pagesPorsche DownloadkongbengNo ratings yet

- Compass Repeater Price Sheet GA4 0912Document2 pagesCompass Repeater Price Sheet GA4 0912kongbengNo ratings yet

- H184a S15Document4 pagesH184a S15kongbengNo ratings yet

- AT572Document3 pagesAT572kongbengNo ratings yet

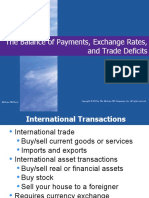

- The Balance of Payments, Exchange Rates, and Trade Deficits: Mcgraw-Hill/IrwinDocument15 pagesThe Balance of Payments, Exchange Rates, and Trade Deficits: Mcgraw-Hill/IrwinMonjur MorshedNo ratings yet

- M BankerDocument41 pagesM BankerNishi SinghNo ratings yet

- 162 019Document4 pages162 019Angelli LamiqueNo ratings yet

- A Training Report On ItcDocument31 pagesA Training Report On Itclakshya rajputNo ratings yet

- PM 10-11Document7 pagesPM 10-11Nguyễn UyênNo ratings yet

- Sales and Distribution at Nike (RJ Corp) : A Project Done Under The Supervision of DR Nidhi SinhaDocument12 pagesSales and Distribution at Nike (RJ Corp) : A Project Done Under The Supervision of DR Nidhi SinhaPriyanshu RanjanNo ratings yet

- Understanding Financial Statements, Taxes, and Cash Flows: Income Statement Balance Sheet Taxes Free Cash Flow (FCF)Document11 pagesUnderstanding Financial Statements, Taxes, and Cash Flows: Income Statement Balance Sheet Taxes Free Cash Flow (FCF)Rejean Dela CruzNo ratings yet

- Ebook Investment Analysis Portfolio Management PDF Full Chapter PDFDocument67 pagesEbook Investment Analysis Portfolio Management PDF Full Chapter PDFjuanita.diaz864100% (28)

- Capital Structure Debt Equity - ProblemsDocument5 pagesCapital Structure Debt Equity - ProblemsSaumya SinghNo ratings yet

- 09 Handout 1Document5 pages09 Handout 1Jeffer Jay GubalaneNo ratings yet

- UAE Corporate Tax PDFDocument59 pagesUAE Corporate Tax PDFzahidfrqNo ratings yet

- Group Exercises IFRS For SMEs - 2012Document14 pagesGroup Exercises IFRS For SMEs - 2012lorenbeatulalianNo ratings yet

- Competitors: Share Broking, Relligare, Angel Broking and Many MoreDocument34 pagesCompetitors: Share Broking, Relligare, Angel Broking and Many MoreAnonymous 1TmZEYNo ratings yet

- Ifrs 9Document4 pagesIfrs 9Elsha MisamisNo ratings yet

- Clearing and Settlement PPT: Financial DerivativesDocument24 pagesClearing and Settlement PPT: Financial DerivativesAnkush SheeNo ratings yet

- Economics Letters: Haejung Na, Soonho KimDocument7 pagesEconomics Letters: Haejung Na, Soonho KimHeni AgustianiNo ratings yet

- Money ControlDocument4 pagesMoney ControlKudire Anil KumarNo ratings yet

- Cougars+Deutsch HBS Case SolutionDocument16 pagesCougars+Deutsch HBS Case Solutionnicco.carduNo ratings yet

- L 5 Cost of CapitalDocument16 pagesL 5 Cost of CapitalMansi SainiNo ratings yet

- Report On Sumeru Securities PVT LTD 2Document18 pagesReport On Sumeru Securities PVT LTD 2sagar timilsinaNo ratings yet

- Profitability Ratio FM 2Document28 pagesProfitability Ratio FM 2Amalia Tamayo YlananNo ratings yet