You might also like

- DN Whitepaper The Case For Cash Recycling April2017Document10 pagesDN Whitepaper The Case For Cash Recycling April2017discovery_saNo ratings yet

- Attacking The Cost of CashDocument8 pagesAttacking The Cost of Cashanonfai173No ratings yet

- Cash LogisticsDocument40 pagesCash LogisticsKalpesh ChouhanNo ratings yet

- A Perspective On German PaymentsDocument12 pagesA Perspective On German PaymentsRohan Batra100% (1)

- European Commission Green Paper Towards Integrated Payments MarketDocument25 pagesEuropean Commission Green Paper Towards Integrated Payments MarketNgân Hàng Ngô Mạnh TiếnNo ratings yet

- The benefits of cash: Costs and benefits of cash and cashless payment instruments (Module 2)From EverandThe benefits of cash: Costs and benefits of cash and cashless payment instruments (Module 2)No ratings yet

- Cash Versus Cards MatemDocument10 pagesCash Versus Cards MatemFlaviub23No ratings yet

- Guide: ATM Cash Management 101Document44 pagesGuide: ATM Cash Management 101abinash234No ratings yet

- The Case For Cash Recycling WhitepaperDocument11 pagesThe Case For Cash Recycling WhitepaperpnkemgneNo ratings yet

- Mobile Remittance Trends and M-Banking Cost ReductionsDocument3 pagesMobile Remittance Trends and M-Banking Cost ReductionsaqsarshadNo ratings yet

- Mr. Hartmann Reports On The Driving Forces Behind Current Changes in Payment and Settlement Systems Speech by Mr. Wendelin Hartmann, A Member of The Board of TheDocument4 pagesMr. Hartmann Reports On The Driving Forces Behind Current Changes in Payment and Settlement Systems Speech by Mr. Wendelin Hartmann, A Member of The Board of TheFlaviub23No ratings yet

- ATM Cash ManagementDocument5 pagesATM Cash Managementtulips26No ratings yet

- ACI Stopping Card Fraud Guide TL US 1010 4414Document28 pagesACI Stopping Card Fraud Guide TL US 1010 4414chawre 786No ratings yet

- Bu 1096 2Document6 pagesBu 1096 2mitch.bainNo ratings yet

- The Changing Retail Payments Landscape: Cost Efficiencies and StandardizationDocument48 pagesThe Changing Retail Payments Landscape: Cost Efficiencies and Standardizationdata_download_allNo ratings yet

- EUROPEAN COMMISSION GREEN PAPER TOWARDS AN INTEGRATED EUROPEAN MARKET FOR CARD, INTERNET AND MOBILE PAYMENTSDocument25 pagesEUROPEAN COMMISSION GREEN PAPER TOWARDS AN INTEGRATED EUROPEAN MARKET FOR CARD, INTERNET AND MOBILE PAYMENTSHaider HussainNo ratings yet

- MR Hartmann Reflects On Recent Developments in International Payment SystemsDocument5 pagesMR Hartmann Reflects On Recent Developments in International Payment SystemsFlaviub23No ratings yet

- ATM Fees: Does Bank Size Matter?: Joanna StavinsDocument12 pagesATM Fees: Does Bank Size Matter?: Joanna StavinsSeanSean ParkNo ratings yet

- Work 948Document20 pagesWork 948Alan CostaNo ratings yet

- Implications For Central Banks of The Development of Electronic MoneyDocument20 pagesImplications For Central Banks of The Development of Electronic MoneyAnonymous PnXCkKIagNo ratings yet

- Bisp 01Document20 pagesBisp 01aufaNo ratings yet

- Ecb - rb221031 A05030021c.enDocument7 pagesEcb - rb221031 A05030021c.enaldhibahNo ratings yet

- Article Vandezande2017Document13 pagesArticle Vandezande2017HenryNo ratings yet

- CBDC and Foreign ExchangeDocument15 pagesCBDC and Foreign ExchangePeekayNo ratings yet

- MoP16 Forging A Path To Payments DigitizationDocument8 pagesMoP16 Forging A Path To Payments DigitizationSophie De SaegerNo ratings yet

- Interchange in PaymentsDocument58 pagesInterchange in PaymentsAsna TungekarNo ratings yet

- Electronic Money and The Possibility ofDocument22 pagesElectronic Money and The Possibility ofjay_kanjariaNo ratings yet

- White Paper Auriga Smart AtmsDocument2 pagesWhite Paper Auriga Smart AtmsirwinohNo ratings yet

- Central Bank Digital Currencies:: Building Block of The Future of Value TransferDocument36 pagesCentral Bank Digital Currencies:: Building Block of The Future of Value TransferYosi YonahNo ratings yet

- Deloitte Uk Economic Impact of Online Payments TMTDocument24 pagesDeloitte Uk Economic Impact of Online Payments TMTVishwajit PatilNo ratings yet

- Debit and Credit Card Schemes in AustraliaDocument90 pagesDebit and Credit Card Schemes in AustraliaCalebNo ratings yet

- Case Study Deloitte Optimizing The Retail Bank Supply Chain 2013 10Document24 pagesCase Study Deloitte Optimizing The Retail Bank Supply Chain 2013 10Navdeep SinghNo ratings yet

- Distributed ledgers transform paymentsDocument14 pagesDistributed ledgers transform paymentsYitian LiNo ratings yet

- Frictionless Cross-Border Payments Alternatives To Correspondent Banking Volante PDFDocument17 pagesFrictionless Cross-Border Payments Alternatives To Correspondent Banking Volante PDFBen ChampionNo ratings yet

- 05 4 p03 0 PDFDocument15 pages05 4 p03 0 PDFJing WenNo ratings yet

- ECB Virtualcurrencyschemes201210enDocument55 pagesECB Virtualcurrencyschemes201210enmichelerovattiNo ratings yet

- Ulrich Bindseil: CBDC (Central Bank Digital Currency) - Financial System Implications and ControlDocument33 pagesUlrich Bindseil: CBDC (Central Bank Digital Currency) - Financial System Implications and ControlAnonymous xBnVwMmnzrNo ratings yet

- Ecb - Op229 4c5ec8f02a.enDocument54 pagesEcb - Op229 4c5ec8f02a.enaldhibahNo ratings yet

- Developing India's Payments InfrastructureDocument3 pagesDeveloping India's Payments Infrastructurekunjan_mehtaNo ratings yet

- Payment instruments used by non-banksDocument4 pagesPayment instruments used by non-banksPietrus KunenyNo ratings yet

- Ali, Barrdear - 2014 - Innovations in Payment Technologies and The Emergence of Digital CurrenciesDocument14 pagesAli, Barrdear - 2014 - Innovations in Payment Technologies and The Emergence of Digital CurrenciesJuana GiupponiNo ratings yet

- Progress Towards Cashless Society Poland PDFDocument5 pagesProgress Towards Cashless Society Poland PDFAndjenie RamautarNo ratings yet

- Electronic Payment Systems: - Strategic and Technical IssuesDocument25 pagesElectronic Payment Systems: - Strategic and Technical IssuesFlaviub23No ratings yet

- Cashless Economy in Nigeria: Discourse of The Advantages and Disadvantages of The PolicyDocument7 pagesCashless Economy in Nigeria: Discourse of The Advantages and Disadvantages of The PolicyLukman Abdurraheem100% (1)

- The International Journal of Engineering and Science (The IJES)Document7 pagesThe International Journal of Engineering and Science (The IJES)theijesNo ratings yet

- Ethiopia Digital Payments AssessmentDocument30 pagesEthiopia Digital Payments AssessmentTEMESGEN TEFERINo ratings yet

- The Evolution of Eft Networks From Atms To New On-Line Debit Payment ProductsDocument12 pagesThe Evolution of Eft Networks From Atms To New On-Line Debit Payment ProductsFlaviub23No ratings yet

- 2003 Cost For PaymentDocument16 pages2003 Cost For PaymentirwinohNo ratings yet

- Retail Payments: Overview, Empirical Results, and Unanswered QuestionsDocument20 pagesRetail Payments: Overview, Empirical Results, and Unanswered QuestionsLuisMendiolaNo ratings yet

- bispap123_eDocument4 pagesbispap123_eremoteworkpmNo ratings yet

- Digitalization enDocument32 pagesDigitalization enKeamogetse MotlogeloaNo ratings yet

- Alex PatheDocument13 pagesAlex PathePatheNo ratings yet

- Significant Effect of The Central Bank Digital Currency On The Design of Monetary PolicyDocument28 pagesSignificant Effect of The Central Bank Digital Currency On The Design of Monetary PolicyArif RamadhanNo ratings yet

- Least-Cost Routing of Debit Card Transactions - RBADocument5 pagesLeast-Cost Routing of Debit Card Transactions - RBACalebNo ratings yet

- European Payments Study 2022Document40 pagesEuropean Payments Study 2022HansNo ratings yet

- Connected Ach For CrossDocument6 pagesConnected Ach For CrossRahulNo ratings yet

- Dps 0116Document30 pagesDps 0116Flaviub23No ratings yet

- bispap128Document23 pagesbispap128BhanusreeNo ratings yet

- Europayments LandscapeDocument7 pagesEuropayments LandscapeRayan INo ratings yet

- The Future of Payment in AfricaDocument17 pagesThe Future of Payment in AfricaNegera AbetuNo ratings yet

- Tax Information Exchange Agreements Are Not Always WorkingDocument3 pagesTax Information Exchange Agreements Are Not Always Workingapi-25890976No ratings yet

- ADR Bulletin: Developing Understanding in ConflictDocument5 pagesADR Bulletin: Developing Understanding in Conflictapi-25890976No ratings yet

- NullDocument117 pagesNullapi-25890976No ratings yet

- Strategy For The Current Market Environment: Intuition Investment ReportDocument3 pagesStrategy For The Current Market Environment: Intuition Investment Reportapi-25890976No ratings yet

- NullDocument117 pagesNullapi-25890976No ratings yet

- Laurence Boulle, Alternative Dispute ResolutionDocument5 pagesLaurence Boulle, Alternative Dispute Resolutioninvestorseurope offshore stockbrokersNo ratings yet

- Tax Information Exchange Agreements Are Not Always WorkingDocument3 pagesTax Information Exchange Agreements Are Not Always Workingapi-25890976No ratings yet

- Tax Information Exchange Agreements Are Not Always WorkingDocument3 pagesTax Information Exchange Agreements Are Not Always Workingapi-25890976No ratings yet

- NullDocument117 pagesNullapi-25890976No ratings yet

- Laurence Boulle, War in Dispute Resolution TheoryDocument21 pagesLaurence Boulle, War in Dispute Resolution Theoryinvestorseurope offshore stockbrokersNo ratings yet

- The Bond Dispute Resolution Center Professor Laurence BoulleDocument13 pagesThe Bond Dispute Resolution Center Professor Laurence Boulleinvestorseurope offshore stockbrokersNo ratings yet

- Titanium Resources Group Preliminary ResultsDocument19 pagesTitanium Resources Group Preliminary Resultsapi-25890976No ratings yet

- Agreement Between The Government of The United States of America and The Government of Gibraltar For The Exchange of Information Relating To TaxesDocument8 pagesAgreement Between The Government of The United States of America and The Government of Gibraltar For The Exchange of Information Relating To Taxesapi-25890976No ratings yet

- RapporteurDocument6 pagesRapporteurapi-25890976No ratings yet

- Submission - National Mediator Accreditation SchemeDocument6 pagesSubmission - National Mediator Accreditation Schemeapi-25890976No ratings yet

- T H e 7 N A T I o N A L M e D I A T I o N C o N F e R e N C eDocument25 pagesT H e 7 N A T I o N A L M e D I A T I o N C o N F e R e N C eapi-25890976No ratings yet

- NullDocument117 pagesNullapi-25890976No ratings yet

- Fédération Européenne Des Conseils Et Intermédiaires FinanciersDocument2 pagesFédération Européenne Des Conseils Et Intermédiaires Financiersapi-25890976No ratings yet

- Cleaning Up Bunker Fuels. But at What Cost?: January 2010Document4 pagesCleaning Up Bunker Fuels. But at What Cost?: January 2010api-25890976No ratings yet

- Committee of European Securities RegulatorsDocument18 pagesCommittee of European Securities Regulatorsapi-25890976No ratings yet

- Winter Law School ProgrammeDocument1 pageWinter Law School Programmeinvestorseurope offshore stockbrokersNo ratings yet

- Understanding The Biggest Market in The WorldDocument5 pagesUnderstanding The Biggest Market in The Worldapi-25890976No ratings yet

- A Consumer's Guide To MiFIDDocument13 pagesA Consumer's Guide To MiFIDapi-25890976No ratings yet

- Risk Assessment ReportDocument41 pagesRisk Assessment Reportapi-25890976100% (1)

- Memorandum 39 - November 2009 PRIPS Workshop 22 October 2009Document7 pagesMemorandum 39 - November 2009 PRIPS Workshop 22 October 2009api-25890976No ratings yet

- BMO CM Basic Points Nov 2009Document43 pagesBMO CM Basic Points Nov 2009ZerohedgeNo ratings yet

- Statement of Business PrinciplesDocument6 pagesStatement of Business Principlesapi-25923204No ratings yet

- South Luangwa Conservation SocietyDocument29 pagesSouth Luangwa Conservation Societyapi-25890976No ratings yet

- South Luangwa Conservation SocietyDocument29 pagesSouth Luangwa Conservation Societyapi-25890976No ratings yet

- A Review of The FX Base Currency Approach FinalDocument18 pagesA Review of The FX Base Currency Approach FinalSyed TabrezNo ratings yet

- Title: 198, Tesma405, IJEAST PDFDocument9 pagesTitle: 198, Tesma405, IJEAST PDFShr BnNo ratings yet

- STRBI Table No. 01 Liabilities and Assets of Scheduled Commercial BanksDocument550 pagesSTRBI Table No. 01 Liabilities and Assets of Scheduled Commercial Banksayush singlaNo ratings yet

- Bank ValuationDocument29 pagesBank ValuationMarc Rubinstein100% (9)

- Project On Investment BankingDocument66 pagesProject On Investment BankingRaveena Rane0% (1)

- AudithaccDocument3 pagesAudithaccTk KimNo ratings yet

- CashSheet-s206 IzuwanDocument2 pagesCashSheet-s206 Izuwanasroneclums hondaNo ratings yet

- Particulars: Rs. RsDocument7 pagesParticulars: Rs. RsAnmol ChawlaNo ratings yet

- M1S2 Memory Retrieval. PaculbaDocument4 pagesM1S2 Memory Retrieval. PaculbaGarr PaculbaNo ratings yet

- Manage finances with online bankingDocument12 pagesManage finances with online bankingDikesh JaiswalNo ratings yet

- Advantages and disadvantages of small scale productionDocument10 pagesAdvantages and disadvantages of small scale productionGøräksh Ñäík100% (1)

- Education Loan FAQs - Manav Rachna International UniversityDocument5 pagesEducation Loan FAQs - Manav Rachna International UniversityKumarPintuNo ratings yet

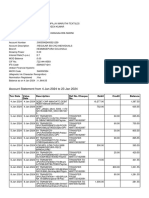

- Account Statement From 4 Jan 2024 To 23 Jan 2024: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument4 pagesAccount Statement From 4 Jan 2024 To 23 Jan 2024: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balancerangaswamy8194No ratings yet

- (A) A Cheque Which Had Originally Been Crossed Is Presented To You For Payment at The Counter Bearing The Remark "Crossing Cancelled" Below The Crossing Under The Drawer's InitialsDocument10 pages(A) A Cheque Which Had Originally Been Crossed Is Presented To You For Payment at The Counter Bearing The Remark "Crossing Cancelled" Below The Crossing Under The Drawer's InitialsSajid IslamNo ratings yet

- General Banking Activities (CBS)Document15 pagesGeneral Banking Activities (CBS)Ifrat SnigdhaNo ratings yet

- 3 - Currency Exchange RatesDocument32 pages3 - Currency Exchange RatesAditya NugrohoNo ratings yet

- Cash and Cash Equivalents Sample ProblemDocument8 pagesCash and Cash Equivalents Sample ProblemAllana MierNo ratings yet

- New Central BankDocument3 pagesNew Central BankMARIANo ratings yet

- BSP ReactionDocument1 pageBSP ReactionReymond Lovendino100% (2)

- AN OVERVIEW OF CUSTOMER SERVICE AT KAILASH BIKAS BANKDocument31 pagesAN OVERVIEW OF CUSTOMER SERVICE AT KAILASH BIKAS BANKArzu dhungana0% (1)

- Credit Union EssayDocument2 pagesCredit Union EssayInday MiraNo ratings yet

- Answer Chapter 1Document5 pagesAnswer Chapter 1Nguyễn Châu Mỹ KiềuNo ratings yet

- The Economics of BankingDocument257 pagesThe Economics of BankingPranav Kumar100% (2)

- Internet Banking ModulesDocument13 pagesInternet Banking ModulesRahul GavandeNo ratings yet

- Description: Tags: lr00Document30 pagesDescription: Tags: lr00anon-536171No ratings yet

- Indian Banking Internet ImpactDocument97 pagesIndian Banking Internet ImpactsspmNo ratings yet

- STMTDocument2 pagesSTMTJorge LopezNo ratings yet

- GD - Assignment 2 LatestDocument29 pagesGD - Assignment 2 LatestNurFazalina AkbarNo ratings yet

- Project Report KotakDocument74 pagesProject Report Kotaksalini singhNo ratings yet

- BofA Q2 2022Document37 pagesBofA Q2 2022ZerohedgeNo ratings yet