You might also like

- Financial Analysis of BDODocument4 pagesFinancial Analysis of BDOPCU COMSELECNo ratings yet

- Fs - Financial InclusionDocument7 pagesFs - Financial InclusionWasim SNo ratings yet

- Marketing Strategy of BankDocument34 pagesMarketing Strategy of BankVirendra SinghNo ratings yet

- SKS Annual Report 2012 13Document120 pagesSKS Annual Report 2012 13maahi7No ratings yet

- Microfinancial Analysis of J&K Grameen Bank2Document99 pagesMicrofinancial Analysis of J&K Grameen Bank2Ayan NazirNo ratings yet

- Axis Bank: Presented byDocument19 pagesAxis Bank: Presented byPratyush RathaNo ratings yet

- AXIS BANK NDocument20 pagesAXIS BANK Nankit5849733% (3)

- Section - ADocument6 pagesSection - ANaman SapraNo ratings yet

- Solved SRCC GBO 2021 Paper With SolutionsDocument51 pagesSolved SRCC GBO 2021 Paper With SolutionsMauli SinghalNo ratings yet

- Training Needs AssessmentDocument4 pagesTraining Needs AssessmentbalwinderNo ratings yet

- Risk Management in Punjab National BankDocument16 pagesRisk Management in Punjab National BanksauravNo ratings yet

- Research Paper Is at DominosDocument6 pagesResearch Paper Is at Dominosssharma83No ratings yet

- Company Profile of KBZ BankDocument6 pagesCompany Profile of KBZ BankKaung Ma Lay100% (1)

- Metrobank PitchDocument38 pagesMetrobank PitchChryselleNo ratings yet

- Bank Marketing StrategiesDocument12 pagesBank Marketing StrategiesLaiba SilenteyesNo ratings yet

- Marketing of Banking ServicesDocument97 pagesMarketing of Banking ServicesAvtaar Singh100% (1)

- New Trends in HR Practices Using AiDocument10 pagesNew Trends in HR Practices Using AiqwerrtNo ratings yet

- Powered by Ninja X SamuraiDocument2 pagesPowered by Ninja X SamuraiArkadeep TalukderNo ratings yet

- SME Lending Axis BankDocument231 pagesSME Lending Axis BankMadhusudan Partani67% (3)

- Prof.. Anju Dusseja: Name Roll - NoDocument18 pagesProf.. Anju Dusseja: Name Roll - NoOmkar PandeyNo ratings yet

- Regional Rural BankDocument26 pagesRegional Rural BankVijayeta Nerurkar100% (1)

- Cry Internship Application Form 1Document3 pagesCry Internship Application Form 1Tanya GuptaNo ratings yet

- Development BanksDocument17 pagesDevelopment BanksAsim jawedNo ratings yet

- Nestle Case Study PDFDocument4 pagesNestle Case Study PDFHina FahadNo ratings yet

- What Are The Benefits of Digital Marketing?Document4 pagesWhat Are The Benefits of Digital Marketing?Katie James100% (1)

- Global Business EnvironmentDocument10 pagesGlobal Business EnvironmentRADHIKA GARG-DMNo ratings yet

- Smart LBox FinalDocument9 pagesSmart LBox FinalAiiv Bautista0% (1)

- The Role of Nabard in Agriculture and Rural Development: An Parvesh Kumar GoyalDocument6 pagesThe Role of Nabard in Agriculture and Rural Development: An Parvesh Kumar GoyalRATHLOGICNo ratings yet

- Segmentation and Targeting of IciciDocument83 pagesSegmentation and Targeting of IciciShristy Singh100% (1)

- Ethical Dilemmas Faced by Multinational CompaniesDocument3 pagesEthical Dilemmas Faced by Multinational CompaniessupriyaNo ratings yet

- Internship Report On MCBDocument37 pagesInternship Report On MCBbbaahmad89No ratings yet

- Executive SummaryDocument4 pagesExecutive SummaryDebashish MazumderNo ratings yet

- RURALDocument21 pagesRURALSrikanth Bhairi100% (2)

- Bharti AirtelDocument25 pagesBharti AirtelSai VasudevanNo ratings yet

- Micro-Finance Case Study of Harshi PattanDocument6 pagesMicro-Finance Case Study of Harshi PattanaadityaNo ratings yet

- Punjab National Bank Vision & Mission StatementDocument34 pagesPunjab National Bank Vision & Mission StatementdhruvinNo ratings yet

- Chapter 1 Summary Cost AccountingDocument8 pagesChapter 1 Summary Cost AccountingkkNo ratings yet

- A Business Plan - RickshawDocument16 pagesA Business Plan - RickshawMehtab Hussain SyedNo ratings yet

- Internal Environment AnalysisDocument3 pagesInternal Environment AnalysisArifHossainNo ratings yet

- ICFAI University, Dehradun: Business Strategy and PoliciesDocument4 pagesICFAI University, Dehradun: Business Strategy and PoliciesPankaj ShuklaNo ratings yet

- Amul External AnalysisDocument14 pagesAmul External AnalysisGagan AulakhNo ratings yet

- Internship Report of NCCBLDocument39 pagesInternship Report of NCCBLaburayhanNo ratings yet

- Marketing Research ProposalDocument7 pagesMarketing Research Proposalsaherhcc4686No ratings yet

- IDLC Finance Limited: Assignment (Research Report)Document29 pagesIDLC Finance Limited: Assignment (Research Report)Nishat ShimaNo ratings yet

- Summer Internship Report - Allied MediaDocument28 pagesSummer Internship Report - Allied MediaSivaKumar RamamoorthyNo ratings yet

- Discuss The Growth and The Current Profile of The TVS Group of CompaniesDocument5 pagesDiscuss The Growth and The Current Profile of The TVS Group of CompaniesKhaled KalamNo ratings yet

- Bharti Minor Project ReportDocument42 pagesBharti Minor Project ReportHatsh kumarNo ratings yet

- Market Segmentation in Banking SectorDocument56 pagesMarket Segmentation in Banking SectorArchana Pawar78% (18)

- Can Information Systems Help Prevent A Public Health CrisisDocument5 pagesCan Information Systems Help Prevent A Public Health CrisisSaba Shahzad100% (1)

- Role of HR ManagerDocument8 pagesRole of HR ManagerRajesh BastiaNo ratings yet

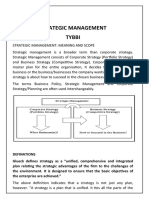

- Strategic Management TybbiDocument40 pagesStrategic Management TybbiAmos Dmello0% (1)

- Internship ReportDocument10 pagesInternship ReportSidra KhanNo ratings yet

- Yes Bank CRMDocument3 pagesYes Bank CRMKartik Karan50% (2)

- Assignment 3Document16 pagesAssignment 3ShradhaMinkuPradhananga100% (1)

- Chapter 3Document36 pagesChapter 3Karuna ShresthaNo ratings yet

- Consumer BehaviorDocument4 pagesConsumer BehaviorsaurabhalmightyNo ratings yet

- Capstone Project Dell PDFDocument55 pagesCapstone Project Dell PDFApeksha PadaliyaNo ratings yet

- Presentation On Internship Report Rastriya Beema Sansthan: Ayusha Regmi 6 Semester (Action) Apex CollegeDocument9 pagesPresentation On Internship Report Rastriya Beema Sansthan: Ayusha Regmi 6 Semester (Action) Apex CollegeSoo Ceal100% (1)

- Buying Behaviour of Consumers Towards Instant Food ProductsDocument13 pagesBuying Behaviour of Consumers Towards Instant Food ProductsHarsh AnchaliaNo ratings yet

- Axis Bank Marketing StrategyDocument10 pagesAxis Bank Marketing StrategyVishal KambleNo ratings yet

- The Chicago Plan Revisited - 2d Paper IMFDocument85 pagesThe Chicago Plan Revisited - 2d Paper IMFuser909No ratings yet

- Consolidation of Wholly Owned Subsidiaries Acquired at More Than Book ValueDocument11 pagesConsolidation of Wholly Owned Subsidiaries Acquired at More Than Book ValueJeklin LewaneyNo ratings yet

- 13 Sources of FinanceDocument26 pages13 Sources of FinanceNikhil GargNo ratings yet

- Credit Rating: Need, Process and LimitationsDocument24 pagesCredit Rating: Need, Process and LimitationsRupam Aryan BorahNo ratings yet

- ALIS - CFS1220 Ayala Land Inc and Subs - SEC - SIGNED - SDocument193 pagesALIS - CFS1220 Ayala Land Inc and Subs - SEC - SIGNED - Slantern san juanNo ratings yet

- Research Report Bajaj Finance LTDDocument8 pagesResearch Report Bajaj Finance LTDvivekNo ratings yet

- New Step Up Unit 4Document24 pagesNew Step Up Unit 4Regina AzzariyaNo ratings yet

- Acc 109 Quiz 1 P3Document2 pagesAcc 109 Quiz 1 P3GargaritanoNo ratings yet

- FAR 02 - Conceptual Framework For Financial ReportingDocument11 pagesFAR 02 - Conceptual Framework For Financial ReportingJohn Bohmer Arcillas PilapilNo ratings yet

- TWO: Financial Analyses and PlanningDocument18 pagesTWO: Financial Analyses and Planningsamuel kebedeNo ratings yet

- Reimbursement 1 1Document5 pagesReimbursement 1 1Sneha JoseNo ratings yet

- Rural Bank Case StudyDocument37 pagesRural Bank Case StudyRusselle Guste IgnacioNo ratings yet

- Estatement PDFDocument5 pagesEstatement PDFTena Chamberlin100% (1)

- Tds ChallanDocument2 pagesTds Challannilesh vithalaniNo ratings yet

- A Study On Financial Statement Analysis of Lakshmigraha Worldwide IncDocument77 pagesA Study On Financial Statement Analysis of Lakshmigraha Worldwide IncSurendra SkNo ratings yet

- Bank Reconciliation: Financial Accounting & Reporting 1Document20 pagesBank Reconciliation: Financial Accounting & Reporting 1Malvin Roix OrenseNo ratings yet

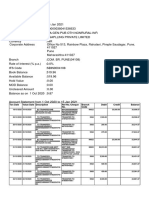

- Sbi Esap BS Ca Oct20-15jan21Document10 pagesSbi Esap BS Ca Oct20-15jan21Minhans SrivastavaNo ratings yet

- EACC2608 Semester Test 1 2023 Memo FinalDocument18 pagesEACC2608 Semester Test 1 2023 Memo FinalNOKUHLE ARTHELNo ratings yet

- Off Balance Sheet Transactions For Islamic BanksDocument25 pagesOff Balance Sheet Transactions For Islamic BanksSyed MohiuddinNo ratings yet

- Compiled Notes I NegoDocument16 pagesCompiled Notes I NegoDeanne ViNo ratings yet

- "Financial Statement Analysis of Bank of Maharashtra": A Project Report OnDocument65 pages"Financial Statement Analysis of Bank of Maharashtra": A Project Report OnShashi RanjanNo ratings yet

- Hand-Out in Insurance Law by Prof. Timoteo AquinoDocument13 pagesHand-Out in Insurance Law by Prof. Timoteo Aquinoapril75No ratings yet

- Fundamentals of AuditingDocument381 pagesFundamentals of AuditingMiguel CarneiroNo ratings yet

- Top 50 CAIIB Practice Questions For BFM: Download Free PDF NowDocument10 pagesTop 50 CAIIB Practice Questions For BFM: Download Free PDF NowAkthar fathimaNo ratings yet

- Nego Quiz 1Document2 pagesNego Quiz 1Koro SenseiNo ratings yet

- Pandemic and Banking IndustryDocument6 pagesPandemic and Banking IndustryHiyakishu SanNo ratings yet

- Financial Institutions Ch-1Document28 pagesFinancial Institutions Ch-1Shimelis Tesema100% (1)

- 12345Document17 pages12345xjammer0% (3)

- Policy Amendment FormDocument8 pagesPolicy Amendment FormN V Sumanth VallabhaneniNo ratings yet

- X Ä A A Ä A A X: Values of Joint-Life Actuarial Functions Based On The AM92 Mortality Table at I 4%Document1 pageX Ä A A Ä A A X: Values of Joint-Life Actuarial Functions Based On The AM92 Mortality Table at I 4%Fung AlexNo ratings yet