You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- DIAMOND NL - The Beauty of Ugly Part 2 - 1H12 Pleasing - Consistency Required To Restore ConvictionDocument6 pagesDIAMOND NL - The Beauty of Ugly Part 2 - 1H12 Pleasing - Consistency Required To Restore ConvictionMukarangaNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- CPI SJ - A Critique On Credit Risks & ROE - Solid Footing But We Maintain Our HOLD On Valuation RiskDocument16 pagesCPI SJ - A Critique On Credit Risks & ROE - Solid Footing But We Maintain Our HOLD On Valuation RiskMukarangaNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- RSA Banks - Run Harder To Stand Still - Next Key Issue For Absa Is Liquidity - We Remain Below ConsensusDocument8 pagesRSA Banks - Run Harder To Stand Still - Next Key Issue For Absa Is Liquidity - We Remain Below ConsensusMukarangaNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- GUARANTY NL - GT The Company, Liked GT The Stock, Unliked - Will The Asset Sensitive Balance Sheet and Growing Retail Exposure Hurt Earnings - Rolling Foward PT To FY13Document9 pagesGUARANTY NL - GT The Company, Liked GT The Stock, Unliked - Will The Asset Sensitive Balance Sheet and Growing Retail Exposure Hurt Earnings - Rolling Foward PT To FY13MukarangaNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Kenyan Banks - Could Equity Be A Victim of Its Own SuccessDocument22 pagesKenyan Banks - Could Equity Be A Victim of Its Own SuccessMukarangaNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- SSA Banks Nigeria Kenya UgandaDocument14 pagesSSA Banks Nigeria Kenya UgandaMukarangaNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Kenyan Banks - A Follow Up On Credit Risks As Investors Become Increasingly Concerned - Salient Features On Mortgage SectorDocument9 pagesKenyan Banks - A Follow Up On Credit Risks As Investors Become Increasingly Concerned - Salient Features On Mortgage SectorMukarangaNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Kenyan Banks - Time To Be Selective - We Remain Concerned by Credit Risks - Despite Higher Cost of Deposist, Banks Managed To Expand Spreads - Rolling PTs To FY13Document22 pagesKenyan Banks - Time To Be Selective - We Remain Concerned by Credit Risks - Despite Higher Cost of Deposist, Banks Managed To Expand Spreads - Rolling PTs To FY13MukarangaNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- SSA Banks - Denial Is Futile - Short Term Risks But Long-Term OpportunitiesDocument13 pagesSSA Banks - Denial Is Futile - Short Term Risks But Long-Term OpportunitiesMukarangaNo ratings yet

- RSA - Half Full or Half EmptyDocument28 pagesRSA - Half Full or Half EmptyMukarangaNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- CPI SJ - Glittery Prospects Priced-In - FY13 TP R205 - HOLDDocument17 pagesCPI SJ - Glittery Prospects Priced-In - FY13 TP R205 - HOLDMukarangaNo ratings yet

- Ugandan Banks - BUY Stanbic - HOLD DFCUDocument44 pagesUgandan Banks - BUY Stanbic - HOLD DFCUMukarangaNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Kenyan Banks - A Critique To System Credit Risks - System NPLs Defying Logic But Regulators Need To Mind The GapDocument22 pagesKenyan Banks - A Critique To System Credit Risks - System NPLs Defying Logic But Regulators Need To Mind The GapMukarangaNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- SSA Banks Nigeria Kenya Uganda Deja VuDocument13 pagesSSA Banks Nigeria Kenya Uganda Deja VuMukarangaNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Nigerian Banks - Atonement, Redemption and Resurrection - BUY Zenith - Diamond - Access - GT - HOLD First - UBADocument87 pagesNigerian Banks - Atonement, Redemption and Resurrection - BUY Zenith - Diamond - Access - GT - HOLD First - UBAMukarangaNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Kenyan Banks - Anchor Themes - Regionalisation and Mortgage Lending - BUY KCB - SELL CoopDocument62 pagesKenyan Banks - Anchor Themes - Regionalisation and Mortgage Lending - BUY KCB - SELL CoopMukarangaNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- ABIL - Non-Retail Deposit Taking Strategy Clouds Long Term Growth Outlook - Initiating With A HOLDDocument56 pagesABIL - Non-Retail Deposit Taking Strategy Clouds Long Term Growth Outlook - Initiating With A HOLDMukarangaNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- Ugandan Banks - BUY Stanbic - HOLD DFCUDocument44 pagesUgandan Banks - BUY Stanbic - HOLD DFCUMukarangaNo ratings yet

- ABIL - Non-Retail Deposit Taking Strategy Clouds Long Term Growth Outlook - Initiating With A HOLDDocument56 pagesABIL - Non-Retail Deposit Taking Strategy Clouds Long Term Growth Outlook - Initiating With A HOLDMukarangaNo ratings yet

- Stanbic Uganda - SBU - Ug 1H09Document9 pagesStanbic Uganda - SBU - Ug 1H09MukarangaNo ratings yet

- ABIL - Reiterate Our SELL - Improving But Lags Our ExpectationsDocument7 pagesABIL - Reiterate Our SELL - Improving But Lags Our ExpectationsMukarangaNo ratings yet

- Capitec Bank - Valuation Looks Steep But Growth Outlook Is The Differentiating Factor - FinalDocument54 pagesCapitec Bank - Valuation Looks Steep But Growth Outlook Is The Differentiating Factor - FinalMukarangaNo ratings yet

- SBU - Ug - Reiteration of BUY - Potential Return 27%Document6 pagesSBU - Ug - Reiteration of BUY - Potential Return 27%MukarangaNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- RSA 2009 OutlookDocument43 pagesRSA 2009 OutlookMukarangaNo ratings yet

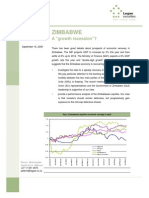

- Zimbabwe - A Growth RecessionDocument17 pagesZimbabwe - A Growth RecessionMukarangaNo ratings yet

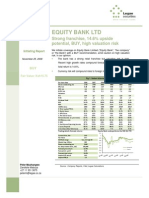

- Equity Bank Limited - Strong Franchise, 14.6% Potential Upsiide, BUY, High Valuation Risk2Document40 pagesEquity Bank Limited - Strong Franchise, 14.6% Potential Upsiide, BUY, High Valuation Risk2MukarangaNo ratings yet

- Kenya - Equities Ripe For A ReboundDocument15 pagesKenya - Equities Ripe For A ReboundMukarangaNo ratings yet

- RMKe-11 Book PDFDocument370 pagesRMKe-11 Book PDFShazwanShahNo ratings yet

- Critical Evaluation of New Indusrial PolicyDocument3 pagesCritical Evaluation of New Indusrial Policypatel_richi75% (4)

- Pestel Analysis Indian Footwear IndustryDocument14 pagesPestel Analysis Indian Footwear IndustryTanuj Kumar57% (7)

- 2013 EU IVD Market Statistics ReportDocument21 pages2013 EU IVD Market Statistics Reportanda_avNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- 06 06 2021 1622989457 6 IMPACTIJRBM 3.IJRBM Feb2021 DeterminantsofMicroandSmallScaleBusinessGrowthinEthiopiaDocument17 pages06 06 2021 1622989457 6 IMPACTIJRBM 3.IJRBM Feb2021 DeterminantsofMicroandSmallScaleBusinessGrowthinEthiopiaKanbiro OrkaidoNo ratings yet

- Case Study SS MiceDocument13 pagesCase Study SS MiceLeiNo ratings yet

- Expanding Opportunity in America'S Schools and WorkplacesDocument102 pagesExpanding Opportunity in America'S Schools and WorkplacesScribd Government DocsNo ratings yet

- GCE AS/A Level 1132/01 Economics - Ec2: P.M. MONDAY, 7 June 2010 2 HoursDocument8 pagesGCE AS/A Level 1132/01 Economics - Ec2: P.M. MONDAY, 7 June 2010 2 HoursprofoundlifeNo ratings yet

- Ch 1 Self Study Q&ADocument5 pagesCh 1 Self Study Q&ANayoon KimNo ratings yet

- Economic SurveyDocument42 pagesEconomic SurveymomliyadroNo ratings yet

- Vaishnani HB Thesis BMDocument409 pagesVaishnani HB Thesis BMRajkumar BaralNo ratings yet

- Lecture 1 - Introduction To Economics of Natural ResourcesDocument19 pagesLecture 1 - Introduction To Economics of Natural ResourcesSUKH SIDHUNo ratings yet

- Topic 1.2 - The Role of Entrepreneurship in SocietyDocument5 pagesTopic 1.2 - The Role of Entrepreneurship in SocietyRay John DulapNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Water Crisis in IndiaDocument24 pagesWater Crisis in IndiaAxel González100% (1)

- Gender EqualityDocument16 pagesGender EqualityRahima HullahNo ratings yet

- Ecosystems and PopulationsDocument37 pagesEcosystems and PopulationsFatma ZorluNo ratings yet

- IT and BPM September 2020Document33 pagesIT and BPM September 2020vaishakNo ratings yet

- The Roadmap To Industrial Automation and Robotics The Situation in The Developing EconomiesDocument9 pagesThe Roadmap To Industrial Automation and Robotics The Situation in The Developing EconomiesWisnu AjiNo ratings yet

- Zakat in Time of Covid-19 Pandemic - EbookDocument79 pagesZakat in Time of Covid-19 Pandemic - EbookInayah Hanifatussilmi WulandariNo ratings yet

- Madhya Pradesh Vision DocumentDocument44 pagesMadhya Pradesh Vision Documentsam_bhopNo ratings yet

- Chapter 06 The Process of Industrialization inDocument9 pagesChapter 06 The Process of Industrialization inMuhammad Saad50% (2)

- Strategic Management of of Coca-ColaDocument17 pagesStrategic Management of of Coca-Colasaurav67% (3)

- Mida20ipr2017Document132 pagesMida20ipr2017Mohammad Hyder AliNo ratings yet

- Role of Entrepreneurs in Socio-Economic DevelopmentDocument19 pagesRole of Entrepreneurs in Socio-Economic DevelopmentAkhilesh KumarNo ratings yet

- Iron and Steel Industry Report 2018 enDocument28 pagesIron and Steel Industry Report 2018 enAlexei AlinNo ratings yet

- Pharmaceuticals Industry Analysis - FinalDocument29 pagesPharmaceuticals Industry Analysis - FinalRishiraj Kashyap100% (1)

- Ministry of Finance QICV WebinarDocument29 pagesMinistry of Finance QICV WebinarHARISHNo ratings yet

- CPSD Honduras 1Document147 pagesCPSD Honduras 1egiron DHV Consultans HondurasNo ratings yet

- Unsustainable Development - The Philippine Experience PDFDocument11 pagesUnsustainable Development - The Philippine Experience PDFDeni MendozaNo ratings yet