You might also like

- Chapter 05 Testbank - Good Chapter 05 Testbank - GoodDocument58 pagesChapter 05 Testbank - Good Chapter 05 Testbank - GoodThu NguyenNo ratings yet

- Other Financing Alternatives Focus: 1. What Are The Five C's of Credit Analysis?Document10 pagesOther Financing Alternatives Focus: 1. What Are The Five C's of Credit Analysis?Muhammad Qasim A20D047FNo ratings yet

- Chapter 05 Testbank: of Mcgraw-Hill EducationDocument61 pagesChapter 05 Testbank: of Mcgraw-Hill EducationshivnilNo ratings yet

- CH - 15 Financial Management: Core ConceptsDocument35 pagesCH - 15 Financial Management: Core ConceptsLolaNo ratings yet

- Question Bank: University of MumbaiDocument5 pagesQuestion Bank: University of MumbaiMelissaNo ratings yet

- Chap 13 SolutionsDocument8 pagesChap 13 SolutionsMiftahudin MiftahudinNo ratings yet

- ADL 55 - Management of Financial Services Assignment-eLearningDocument7 pagesADL 55 - Management of Financial Services Assignment-eLearningAD Lead100% (1)

- Test 2 - PM - ADocument16 pagesTest 2 - PM - ADữ NguyễnNo ratings yet

- Ch8. Sources of Business Finance (AK)Document10 pagesCh8. Sources of Business Finance (AK)drdoomyt1089gNo ratings yet

- Sources and Uses of Short-Term and Long-Term Funds: LessonDocument8 pagesSources and Uses of Short-Term and Long-Term Funds: LessonI am MystineNo ratings yet

- Banking Quiz on Assets, Liabilities, Basel Accords & MoreDocument5 pagesBanking Quiz on Assets, Liabilities, Basel Accords & Morenatasha100% (1)

- CH 8 Sources of Business Finance Class 11 BSTDocument19 pagesCH 8 Sources of Business Finance Class 11 BSTRaman SachdevaNo ratings yet

- Chapter 8: Sources of Capital For Entrepreneurs: True/FalseDocument5 pagesChapter 8: Sources of Capital For Entrepreneurs: True/Falseelizabeth bernalesNo ratings yet

- Equity Financing Small Business AdministrationDocument8 pagesEquity Financing Small Business AdministrationrajuNo ratings yet

- 2006 s2 SolutionsDocument22 pages2006 s2 SolutionsVinit DesaiNo ratings yet

- Chapter 20 - Hybrid Financing - Prefernce Shares, Leasing, Options, Warrants, & ConvertiblesDocument2 pagesChapter 20 - Hybrid Financing - Prefernce Shares, Leasing, Options, Warrants, & Convertibleslou-924No ratings yet

- Financing strategies and risksDocument4 pagesFinancing strategies and risksMariam AmirehNo ratings yet

- Ch8. Sources of Business Finance (AK)Document10 pagesCh8. Sources of Business Finance (AK)Arundhoti MukherjeeNo ratings yet

- Medium and Long-term Debt Financing OptionsDocument47 pagesMedium and Long-term Debt Financing OptionsKhang Tran DuyNo ratings yet

- UntitledDocument1 pageUntitledJEANNE PAULINE OABELNo ratings yet

- Fundamentals of Corporate Finance Canadian 5th Edition Brealey Test BankDocument68 pagesFundamentals of Corporate Finance Canadian 5th Edition Brealey Test BankEricBergermfcrd100% (13)

- Chapter 17Document7 pagesChapter 17Linh ChiNo ratings yet

- Leach TB Chap12 Ed3Document7 pagesLeach TB Chap12 Ed3bia070386No ratings yet

- Understanding Equity and Debt FinancingDocument7 pagesUnderstanding Equity and Debt FinancingSindisiwe DlaminiNo ratings yet

- AC 313 Sources of Finance - Margaret Aeka ID 22700021Document10 pagesAC 313 Sources of Finance - Margaret Aeka ID 2270002122700021maaeNo ratings yet

- Unit - Vi Financing of Working CapitalDocument45 pagesUnit - Vi Financing of Working Capitaljitesh dhuleNo ratings yet

- Types of Borrowers-Lending ProcessDocument39 pagesTypes of Borrowers-Lending ProcessEr YogendraNo ratings yet

- Chap 017Document27 pagesChap 017Xeniya Morozova Kurmayeva100% (4)

- CH5 FinancingDocument2 pagesCH5 FinancingSamir SubediNo ratings yet

- Quiz Ak2Document23 pagesQuiz Ak2Andhika YogaraksaNo ratings yet

- Tybfm Sem6 VcpeDocument47 pagesTybfm Sem6 VcpeLeo Bogosi MotlogelwNo ratings yet

- 74786bos60495 Cp9u6Document53 pages74786bos60495 Cp9u6CHETNA CHANGLANINo ratings yet

- Chapter 6-8 - Sources of Finance & Short Term FinanceDocument8 pagesChapter 6-8 - Sources of Finance & Short Term FinanceTAN YUN YUNNo ratings yet

- IFQ Sample QsDocument14 pagesIFQ Sample Qspuliyanam100% (1)

- Chapter09 IfDocument10 pagesChapter09 IfPatricia PamelaNo ratings yet

- Corporate Finance Canadian 7th Edition Ross Test BankDocument27 pagesCorporate Finance Canadian 7th Edition Ross Test BankChristinaCrawfordigdyp100% (16)

- Mezzanine Finance ExplainedDocument9 pagesMezzanine Finance Explainedshweta khamarNo ratings yet

- FMS QBDocument57 pagesFMS QBkrishna chaitanyaNo ratings yet

- Corporate Finance Canadian 7th Edition Jaffe Test BankDocument27 pagesCorporate Finance Canadian 7th Edition Jaffe Test Bankdeborahmatayxojqtgzwr100% (13)

- FM Mod 5Document9 pagesFM Mod 5Gauri SinghNo ratings yet

- Guide To Preparing For Bond Issuance in NigeriaDocument21 pagesGuide To Preparing For Bond Issuance in NigeriaIfeNo ratings yet

- Corporate Finance Lecture Note Packet 2 Capital Structure, Dividend Policy and ValuationDocument262 pagesCorporate Finance Lecture Note Packet 2 Capital Structure, Dividend Policy and ValuationBhargavVithalaniNo ratings yet

- FinMan 1 - Prelim Reviewer 2017Document17 pagesFinMan 1 - Prelim Reviewer 2017Rachel Dela CruzNo ratings yet

- Corporate Law 5th SemDocument20 pagesCorporate Law 5th SemAayushiNo ratings yet

- Exam Code 1 ObDocument4 pagesExam Code 1 ObHuỳnh Lê Yến VyNo ratings yet

- Chapter 6Document7 pagesChapter 6Elijah IbsaNo ratings yet

- Audit Prob Part 2Document6 pagesAudit Prob Part 2Koko LaineNo ratings yet

- FRM Test 02 AnsDocument13 pagesFRM Test 02 AnsKamal BhatiaNo ratings yet

- Name Email-ID Smart Task No. Project Topic: Intern's DetailsDocument4 pagesName Email-ID Smart Task No. Project Topic: Intern's DetailsKinnu RajpuraNo ratings yet

- Cordillera Career Development College Financial Management IIDocument6 pagesCordillera Career Development College Financial Management IIJungie Mablay WalacNo ratings yet

- Chapter 10 Testbank Key Finance ConceptsDocument8 pagesChapter 10 Testbank Key Finance ConceptsTu NgNo ratings yet

- PF.docxDocument16 pagesPF.docxadabotor7No ratings yet

- What Makes A Good LoaNDocument25 pagesWhat Makes A Good LoaNrajin_rammsteinNo ratings yet

- Report - FonterraDocument19 pagesReport - FonterraK59 DOAN THANH TAMNo ratings yet

- Credit PolicyDocument84 pagesCredit PolicyDan John Karikottu100% (6)

- BfinDocument7 pagesBfinPaolo Niño AntonioNo ratings yet

- Credit and CollectionDocument53 pagesCredit and CollectionApril CastilloNo ratings yet

- Textbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingFrom EverandTextbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingNo ratings yet

- VC Valuation Methods SummaryDocument9 pagesVC Valuation Methods Summarybia070386No ratings yet

- 8Document11 pages8bia070386No ratings yet

- Leach TB Chap12 Ed3Document7 pagesLeach TB Chap12 Ed3bia070386No ratings yet

- EfDocument8 pagesEfbia070386No ratings yet

- Venture Capital Valuation Methods Chapter Explains Key TechniquesDocument7 pagesVenture Capital Valuation Methods Chapter Explains Key Techniquesbia070386No ratings yet

- Harvesting the Business Venture InvestmentDocument8 pagesHarvesting the Business Venture Investmentbia070386No ratings yet

- Security Structures and Deterimining Enterprise Values True-False QuestionsDocument6 pagesSecurity Structures and Deterimining Enterprise Values True-False Questionsbia070386No ratings yet

- 7Document9 pages7bia07038650% (2)

- EFim 05 Ed 3Document23 pagesEFim 05 Ed 3bia070386100% (1)

- Chap 1Document7 pagesChap 1bia070386No ratings yet

- Leach TB Chap08 Ed3Document9 pagesLeach TB Chap08 Ed3bia070386No ratings yet

- Types and Costs of Financial Capital: True-False QuestionsDocument8 pagesTypes and Costs of Financial Capital: True-False Questionsbia070386No ratings yet

- Leach TB Chap12 Ed3Document7 pagesLeach TB Chap12 Ed3bia070386No ratings yet

- Leach TB Chap11 Ed3Document7 pagesLeach TB Chap11 Ed3bia070386No ratings yet

- Leach TB Chap09 Ed3Document8 pagesLeach TB Chap09 Ed3bia070386No ratings yet

- Financial Planning: Short Term and Long Term: True-False QuestionsDocument8 pagesFinancial Planning: Short Term and Long Term: True-False Questionsbia070386No ratings yet

- Leach TB Chap03 Ed3Document10 pagesLeach TB Chap03 Ed3bia070386No ratings yet

- Evaluating Financial Performance: True-False QuestionsDocument9 pagesEvaluating Financial Performance: True-False Questionsbia070386100% (1)

- Leach TB Chap04 Ed3Document8 pagesLeach TB Chap04 Ed3bia070386No ratings yet

- CH 05 Evaluating Financial PerformanceDocument42 pagesCH 05 Evaluating Financial Performancebia070386100% (1)

- EF New Venture StrategyDocument5 pagesEF New Venture Strategybia070386No ratings yet

- Leach TB Chap01 Ed3Document9 pagesLeach TB Chap01 Ed3bia070386No ratings yet

- Chapter 3 IHRM NewDocument38 pagesChapter 3 IHRM Newbia070386No ratings yet

- CH 06 Financial Planning Short Term and Long TermDocument27 pagesCH 06 Financial Planning Short Term and Long TermshaahmookhanNo ratings yet

- The Principles of Successful Project ManagementDocument5 pagesThe Principles of Successful Project Managementbia070386No ratings yet

- Brazil and India Payment SystemDocument6 pagesBrazil and India Payment SystemRahul SinghNo ratings yet

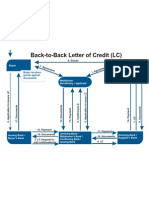

- Back To Back LCDocument1 pageBack To Back LCJayant Nair0% (1)

- RES 3200 Chapter 2 Real Estate FinancingDocument12 pagesRES 3200 Chapter 2 Real Estate FinancingbaorunchenNo ratings yet

- IJRSML 2015 Vol03 Issue 03 07Document6 pagesIJRSML 2015 Vol03 Issue 03 07Aftab HusainNo ratings yet

- Chapter 3 Government Banking InstitutionsDocument31 pagesChapter 3 Government Banking InstitutionsChichay KarenJoyNo ratings yet

- Types of L/CDocument127 pagesTypes of L/CSudershan ThaibaNo ratings yet

- Chapter16 PDFDocument50 pagesChapter16 PDFBabuM ACC FIN ECONo ratings yet

- Effects of Inflation AlchianDocument18 pagesEffects of Inflation AlchianCoco 12No ratings yet

- Chapter-6 Foreign Exchange and Financing of Foreign TradeDocument7 pagesChapter-6 Foreign Exchange and Financing of Foreign TradeFardin KhanNo ratings yet

- Risk Based Audit Approach in BanksDocument24 pagesRisk Based Audit Approach in Banksgian50% (2)

- Digital Technology & Inclusive Growth - Luohan Academy - 25Document22 pagesDigital Technology & Inclusive Growth - Luohan Academy - 25Andrean DinataNo ratings yet

- Credit Card Comparison: 0% For 6 Mo, 16.24% To 27.24% AfterDocument3 pagesCredit Card Comparison: 0% For 6 Mo, 16.24% To 27.24% AfterElise Smoll (Elise)No ratings yet

- Mis Assignment 4: Bajaj Electricals: Submitted To Prof. Harekrishna MisraDocument15 pagesMis Assignment 4: Bajaj Electricals: Submitted To Prof. Harekrishna MisraSupriya SarkarNo ratings yet

- Module 2Document20 pagesModule 2FRANZ ERVY D MALLARINo ratings yet

- Oliver v. Philippine Savings Bank and CastroDocument15 pagesOliver v. Philippine Savings Bank and CastroTESDA MIMAROPANo ratings yet

- Credit Risk Managementofnepalese Commercial Bank: A Thesis Proposal BY: Khim Raj B.CDocument11 pagesCredit Risk Managementofnepalese Commercial Bank: A Thesis Proposal BY: Khim Raj B.Canup bidariNo ratings yet

- CGTMSE - Scheme Document CGS I - Updated As On March 31, 2022 PDFDocument26 pagesCGTMSE - Scheme Document CGS I - Updated As On March 31, 2022 PDFkarthik kvNo ratings yet

- Presentation - Randolph Flay - USAIDDocument18 pagesPresentation - Randolph Flay - USAIDCSIPVietnamNo ratings yet

- Global Div Inv Grade Income Trust II-IndyMac 2005-AR14!3!31-10Document17 pagesGlobal Div Inv Grade Income Trust II-IndyMac 2005-AR14!3!31-10Barbara J. FordeNo ratings yet

- Consulting Case GuesstimateDocument82 pagesConsulting Case GuesstimateJerryJoshuaDiazNo ratings yet

- Business Activity Codes: WWW - Census.gov/cgi-Bin/sssd/ Naics/naicsrch?chart 2017Document1 pageBusiness Activity Codes: WWW - Census.gov/cgi-Bin/sssd/ Naics/naicsrch?chart 2017brenda smithNo ratings yet

- Colombia Watch Bank of America June 2023Document13 pagesColombia Watch Bank of America June 2023La Silla VacíaNo ratings yet

- Exim Finance, LC & Forfaiting-RDocument50 pagesExim Finance, LC & Forfaiting-RProf Dr Chowdari Prasad100% (1)

- SaudiFactbook 2010Document225 pagesSaudiFactbook 2010Harsh KediaNo ratings yet

- Project Home Loan-Team 9Document50 pagesProject Home Loan-Team 9Shadab HasanNo ratings yet

- Loan and Mortgage FraudDocument15 pagesLoan and Mortgage FraudHan Win100% (1)

- Chase Sapphire Case Study: Marketing and BenefitsDocument6 pagesChase Sapphire Case Study: Marketing and BenefitsLazy BotNo ratings yet

- Pantaleon V American ExpressDocument3 pagesPantaleon V American ExpressJogie AradaNo ratings yet

- Credit Transactions CASES 2nd ExamDocument41 pagesCredit Transactions CASES 2nd ExamAmanda Buttkiss100% (1)

- Hand-Out No. 5: Loan Receivable Financial Accounting and Reporting HAND-OUT NO. 5: Loan ReceivableDocument4 pagesHand-Out No. 5: Loan Receivable Financial Accounting and Reporting HAND-OUT NO. 5: Loan ReceivableJorufel PapasinNo ratings yet