You might also like

- A Complete Guide To Volume Price Analysi - A. CoullingDocument242 pagesA Complete Guide To Volume Price Analysi - A. CoullingGiundat Giun Dat97% (129)

- Trading in The Shadow of The Smart Money BookDocument192 pagesTrading in The Shadow of The Smart Money BookSalvo Nona85% (46)

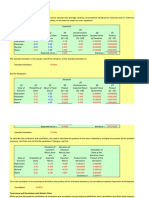

- CVP Excel ProjectDocument10 pagesCVP Excel ProjectLinh Ha Nguyen Khanh50% (4)

- Coffee Can Investing - The Low Risk Road To Stupendous WealthDocument364 pagesCoffee Can Investing - The Low Risk Road To Stupendous WealthKristen Ravali100% (38)

- Acsm Personal Trainer Exam Study GuideDocument18 pagesAcsm Personal Trainer Exam Study GuideHong Ye100% (1)

- DK Eyewitness Travel Guide - Barcelona & Catalonia (PDFDrive) PDFDocument210 pagesDK Eyewitness Travel Guide - Barcelona & Catalonia (PDFDrive) PDFDarryl Wallace100% (1)

- 59.business Intelligence and Analytics PDFDocument317 pages59.business Intelligence and Analytics PDFWilliam Archila100% (2)

- Majestic Mulch and Compost Co. Capital Budgeting AnalysisDocument68 pagesMajestic Mulch and Compost Co. Capital Budgeting AnalysisMnar Abu-ShliebaNo ratings yet

- FRM Index (Revised)Document28 pagesFRM Index (Revised)api-3717306No ratings yet

- Investigating The Value of An MBA Education Using NPV Decision ModelDocument72 pagesInvestigating The Value of An MBA Education Using NPV Decision ModelnabilquadriNo ratings yet

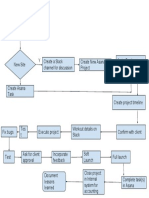

- Project WorkflowDocument1 pageProject WorkflowAnnaNo ratings yet

- Ch06 Tool KitDocument36 pagesCh06 Tool KitRoy HemenwayNo ratings yet

- CF Chapter 11 Excel Master StudentDocument40 pagesCF Chapter 11 Excel Master Studentjulita08No ratings yet

- FINA Chapter 6 HWDocument7 pagesFINA Chapter 6 HWBrandonNo ratings yet

- FCF Ch02 Excel Master StudentDocument24 pagesFCF Ch02 Excel Master Studentannu technologyNo ratings yet

- The Small Business Owner's Manual - Everything You Need To Know To Start Up and Run Your Business PDFDocument312 pagesThe Small Business Owner's Manual - Everything You Need To Know To Start Up and Run Your Business PDFkonserNo ratings yet

- Unlocking The Guitar Fretboard - An Intervallic Approach Towards M PDFDocument169 pagesUnlocking The Guitar Fretboard - An Intervallic Approach Towards M PDFANMOL100% (2)

- Electrician Guide Test PrepDocument6 pagesElectrician Guide Test PrepDarryl Wallace33% (3)

- Chap 005 MasterDocument116 pagesChap 005 MasterEstela VelazcoNo ratings yet

- CF Chapter 06 Excel Master StudentDocument41 pagesCF Chapter 06 Excel Master StudentImran KhanNo ratings yet

- Excel Project Timesheet FullDocument4 pagesExcel Project Timesheet Fullprateekchopra1No ratings yet

- In These Spreadsheets, You Will Learn How To Use The Following Excel FunctionsDocument78 pagesIn These Spreadsheets, You Will Learn How To Use The Following Excel FunctionsFaisal SiddiquiNo ratings yet

- LCC FormulaDocument3 pagesLCC Formulasomapala88No ratings yet

- TVM Formulas Guide Business Math ProblemsDocument7 pagesTVM Formulas Guide Business Math ProblemsAftab HossainNo ratings yet

- SEEP FRAME Tool, Version 2.02Document159 pagesSEEP FRAME Tool, Version 2.02anish-kc-8151No ratings yet

- ArgumentsDocument21 pagesArgumentsSaddam MullaNo ratings yet

- Excels For Solution ManualDocument116 pagesExcels For Solution ManualDimple PandeyNo ratings yet

- Performance Evaluation of Construction PDocument10 pagesPerformance Evaluation of Construction PMarioNo ratings yet

- Answers - Capital Budgeting TechniquesDocument44 pagesAnswers - Capital Budgeting Techniquesjacks ocNo ratings yet

- 3.NPER Function Excel Template 1Document9 pages3.NPER Function Excel Template 1w_fibNo ratings yet

- LR5 Cap 9 Cost Estimating - Scott Amos - Skills Knowledge of Cost Engineering - AACEI - 2004Document36 pagesLR5 Cap 9 Cost Estimating - Scott Amos - Skills Knowledge of Cost Engineering - AACEI - 2004apzambonNo ratings yet

- Analysis of Transaction CostDocument383 pagesAnalysis of Transaction CosthjsdNo ratings yet

- Excel Skills and Functions for Business Problem SolvingDocument119 pagesExcel Skills and Functions for Business Problem SolvingRishabh JainNo ratings yet

- CF 10e Chapter 11 Excel Master StudentDocument32 pagesCF 10e Chapter 11 Excel Master StudentWalter CostaNo ratings yet

- Primavera P6: Project Monitoring DepartmentDocument76 pagesPrimavera P6: Project Monitoring DepartmentMariam SaeedNo ratings yet

- Excel Advanced Excel For Finance EXERCISEDocument91 pagesExcel Advanced Excel For Finance EXERCISEhaz002No ratings yet

- Capital Budgeting Techniques WorkshopDocument3 pagesCapital Budgeting Techniques WorkshopValentina Barreto Puerta0% (1)

- Mgac CustomDocument123 pagesMgac CustomJoana TrinidadNo ratings yet

- Ch11 13ed CF Estimation MinicMasterDocument20 pagesCh11 13ed CF Estimation MinicMasterAnoop SlathiaNo ratings yet

- Compare ASME and material specsDocument2 pagesCompare ASME and material specsg_sanchetiNo ratings yet

- Employee Timecard1Document34 pagesEmployee Timecard1Ebiyele Olusegun OwoturoNo ratings yet

- Ch2-General Design Considerations Week2Document61 pagesCh2-General Design Considerations Week2ميثة الغيثيةNo ratings yet

- Chapter 8Document78 pagesChapter 8Faisal SiddiquiNo ratings yet

- Linear Programming On Excel: Problems and SolutionsDocument5 pagesLinear Programming On Excel: Problems and Solutionsacetinkaya92No ratings yet

- Risk and Return - Section 11.2Document99 pagesRisk and Return - Section 11.2Dane JonesNo ratings yet

- CH 4 4-35 SpreadsheetDocument34 pagesCH 4 4-35 Spreadsheetcherishwisdom_997598No ratings yet

- 12-Month Cash Flow ForecastDocument7 pages12-Month Cash Flow Forecastm qaiserNo ratings yet

- Hillier Model 3Document19 pagesHillier Model 3kavyaambekarNo ratings yet

- Chapter 6. Interest RatesDocument33 pagesChapter 6. Interest RatesNaufal IhsanNo ratings yet

- 1.FV Function Excel Template 1Document6 pages1.FV Function Excel Template 1w_fibNo ratings yet

- Ch05 Mini CaseDocument8 pagesCh05 Mini CaseSehar Salman AdilNo ratings yet

- Capitalization: Capital Vs Operating LeaseDocument2 pagesCapitalization: Capital Vs Operating Leasejohnsmith12312312312No ratings yet

- Financial Calculator Find Future Value - Time Line: Solving ForDocument3 pagesFinancial Calculator Find Future Value - Time Line: Solving ForPiyush KakkarNo ratings yet

- 2GO Excel Calculation 1Document60 pages2GO Excel Calculation 1w_fibNo ratings yet

- Cost Accounting Chapter 2 IntroductionDocument13 pagesCost Accounting Chapter 2 IntroductionAbigail Faye Roxas100% (1)

- Budgetary Control as a Key Management ToolDocument45 pagesBudgetary Control as a Key Management ToolMahtab AlamNo ratings yet

- Monthly Account-1Document46 pagesMonthly Account-1Abdul AleemNo ratings yet

- Timesheet: January, February, MarchDocument4 pagesTimesheet: January, February, MarchkhuonggiaNo ratings yet

- FCFF Valuation Model: Before You Start What The Model Doe Inputs Master Inputs Page Earnings NormalizerDocument34 pagesFCFF Valuation Model: Before You Start What The Model Doe Inputs Master Inputs Page Earnings Normalizernikhil1684No ratings yet

- Material-Handling EquipmentDocument7 pagesMaterial-Handling EquipmentNickiNo ratings yet

- Cash Flow Forecast TemplateDocument1 pageCash Flow Forecast TemplateMohamed Ahmed100% (1)

- CH 02 Mini CaseDocument18 pagesCH 02 Mini CaseCuong LeNo ratings yet

- Material DashboardDocument1 pageMaterial DashboardmdcegyptNo ratings yet

- EXERCISE - Calculating The Internal Rate of ReturnDocument5 pagesEXERCISE - Calculating The Internal Rate of ReturnNipun BajajNo ratings yet

- Glossary PM TerminologyDocument14 pagesGlossary PM TerminologyLawal Idris AdesholaNo ratings yet

- FCF Ch10 Excel Master StudentDocument68 pagesFCF Ch10 Excel Master StudentSilviaKartikaNo ratings yet

- Advance FunctionDocument20 pagesAdvance Functionthouseef06No ratings yet

- FCF Ch10 Excel Master StudentDocument68 pagesFCF Ch10 Excel Master StudentSilviaKartikaNo ratings yet

- James Personal Study Guide - PDF RoomDocument88 pagesJames Personal Study Guide - PDF RoomDarryl WallaceNo ratings yet

- Personal Study Guide - PDF RoomDocument41 pagesPersonal Study Guide - PDF RoomDarryl WallaceNo ratings yet

- (Media Business and Innovation) Artur Lugmayr, Cinzia Dal Zotto (Eds.)-Media Convergence Handbook - Vol. 1_ Journalism, Broadcasting, And Social Media Aspects of Convergence-Springer-Verlag Berlin HeiDocument430 pages(Media Business and Innovation) Artur Lugmayr, Cinzia Dal Zotto (Eds.)-Media Convergence Handbook - Vol. 1_ Journalism, Broadcasting, And Social Media Aspects of Convergence-Springer-Verlag Berlin HeiCîrstea AndreaNo ratings yet

- (BCPI, CLI, Warren J. Sonne) Criminal InvestigatioDocument186 pages(BCPI, CLI, Warren J. Sonne) Criminal InvestigatioSP Samuel Crespo100% (1)

- Persodevmanual PDFDocument1 pagePersodevmanual PDFSyedaffanNo ratings yet

- Explore The Bible Personal Study Guide - King James Version - PDF RoomDocument20 pagesExplore The Bible Personal Study Guide - King James Version - PDF RoomDarryl WallaceNo ratings yet

- 0902 Trading The Line PDFDocument45 pages0902 Trading The Line PDFRara Laki Laki100% (2)

- Investigative Journalism Manual (PDFDrive)Document121 pagesInvestigative Journalism Manual (PDFDrive)Darryl Wallace100% (2)

- TenThingsYouMustKnow KHMTRAVELDocument15 pagesTenThingsYouMustKnow KHMTRAVELDarryl WallaceNo ratings yet

- Cloud Computing Framework for Apparel Supply ChainsDocument12 pagesCloud Computing Framework for Apparel Supply ChainsDarryl WallaceNo ratings yet

- Selecting A Travel Management Company: Business Travel Buyer'S HandbookDocument6 pagesSelecting A Travel Management Company: Business Travel Buyer'S HandbookDarryl WallaceNo ratings yet

- Ada 596948Document214 pagesAda 596948Hajji Assamo PadilNo ratings yet

- FCM Redefining Corporate Travel Management 2019Document68 pagesFCM Redefining Corporate Travel Management 2019Darryl WallaceNo ratings yet

- Travel Agent - Outside Sales Support Netqork - Official Member HandbookDocument128 pagesTravel Agent - Outside Sales Support Netqork - Official Member HandbookDarryl Wallace100% (1)

- Erin Kennedy Executive ResumeDocument3 pagesErin Kennedy Executive ResumeDarryl WallaceNo ratings yet

- Everything You Need To Know About Becoming A: Successful Inteletravel AdvisorDocument8 pagesEverything You Need To Know About Becoming A: Successful Inteletravel AdvisorDarryl WallaceNo ratings yet

- Lead Guitar 6 Lesson GuideDocument37 pagesLead Guitar 6 Lesson GuideCarlos FernandezNo ratings yet

- Resume PrepareDocument28 pagesResume PreparekaparaveniNo ratings yet

- Eden WT500, WT600, WT800 - SchematicDocument307 pagesEden WT500, WT600, WT800 - SchematicDarkbass BowieNo ratings yet

- How Did House Bands Become A Filipino Export - The New York TimesDocument11 pagesHow Did House Bands Become A Filipino Export - The New York TimesDarryl WallaceNo ratings yet

- Exam PrepDocument57 pagesExam PrepMoh Slam100% (2)

- Broadband BillDocument1 pageBroadband BillKushi GowdaNo ratings yet

- Sugar Milling Contract DisputeDocument3 pagesSugar Milling Contract DisputeRomy IanNo ratings yet

- Merlin Gerin Medium VoltageDocument10 pagesMerlin Gerin Medium VoltagekjfenNo ratings yet

- Presentation of The LordDocument1 pagePresentation of The LordSarah JonesNo ratings yet

- C J L F S: Vinod TiwariDocument21 pagesC J L F S: Vinod TiwariVinod TiwariNo ratings yet

- Pike River Case StudyDocument7 pagesPike River Case StudyGale HawthorneNo ratings yet

- Philippines Taxation Scope and ReformsDocument4 pagesPhilippines Taxation Scope and ReformsAngie Olpos Boreros BaritugoNo ratings yet

- Unit 13 AminesDocument3 pagesUnit 13 AminesArinath DeepaNo ratings yet

- A - Bahasa Inggris-DikonversiDocument96 pagesA - Bahasa Inggris-DikonversiArie PurnamaNo ratings yet

- ДСТУ EN ISO 2400-2016 - Калибровочный блок V1Document11 pagesДСТУ EN ISO 2400-2016 - Калибровочный блок V1Игорь ВадешкинNo ratings yet

- Leapfroggers, People Who Start A Company, Manage Its Growth Until They Get Bored, and Then SellDocument3 pagesLeapfroggers, People Who Start A Company, Manage Its Growth Until They Get Bored, and Then Sellayesha noorNo ratings yet

- Programming in Java Assignment 8: NPTEL Online Certification Courses Indian Institute of Technology KharagpurDocument4 pagesProgramming in Java Assignment 8: NPTEL Online Certification Courses Indian Institute of Technology KharagpurPawan NaniNo ratings yet

- 04 Activity 2Document2 pages04 Activity 2Jhon arvie MalipolNo ratings yet

- Stellar Competent CellsDocument1 pageStellar Competent CellsSergio LaynesNo ratings yet

- Lead Magnet 43 Foolproof Strategies To Get More Leads, Win A Ton of New Customers and Double Your Profits in Record Time... (RDocument189 pagesLead Magnet 43 Foolproof Strategies To Get More Leads, Win A Ton of New Customers and Double Your Profits in Record Time... (RluizdasilvaazevedoNo ratings yet

- Java MCQ questions and answersDocument65 pagesJava MCQ questions and answersShermin FatmaNo ratings yet

- The Power of Flexibility: - B&P Pusher CentrifugesDocument9 pagesThe Power of Flexibility: - B&P Pusher CentrifugesberkayNo ratings yet

- Safety of High-Rise BuildingsDocument14 pagesSafety of High-Rise BuildingsHananeel Sandhi100% (2)

- WM3000U - WM3000 I: Measuring Bridges For Voltage Transformers and Current TransformersDocument4 pagesWM3000U - WM3000 I: Measuring Bridges For Voltage Transformers and Current TransformersEdgar JimenezNo ratings yet

- Embedded Systems: Martin Schoeberl Mschoebe@mail - Tuwien.ac - atDocument27 pagesEmbedded Systems: Martin Schoeberl Mschoebe@mail - Tuwien.ac - atDhirenKumarGoleyNo ratings yet

- Rejoinder To Adom Ochere's Misrepresentation - FinalDocument3 pagesRejoinder To Adom Ochere's Misrepresentation - FinalFuaad DodooNo ratings yet

- Industry Life Cycle-Plant Based CaseDocument3 pagesIndustry Life Cycle-Plant Based CaseRachelle BrownNo ratings yet

- Hillingdon Health Visiting ServiceDocument12 pagesHillingdon Health Visiting ServiceAnnikaNo ratings yet

- Market Participants in Securities MarketDocument11 pagesMarket Participants in Securities MarketSandra PhilipNo ratings yet

- Keynes Presentation - FINALDocument62 pagesKeynes Presentation - FINALFaith LuberasNo ratings yet

- RCA - Mechanical - Seal - 1684971197 2Document20 pagesRCA - Mechanical - Seal - 1684971197 2HungphamphiNo ratings yet

- AutocadDocument8 pagesAutocadbrodyNo ratings yet

- A Research About The Canteen SatisfactioDocument50 pagesA Research About The Canteen SatisfactioJakeny Pearl Sibugan VaronaNo ratings yet

- CELF Final ProspectusDocument265 pagesCELF Final ProspectusDealBookNo ratings yet

- Best Homeopathic Doctor in SydneyDocument8 pagesBest Homeopathic Doctor in SydneyRC homeopathyNo ratings yet