You might also like

- The Versatility of the Real Estate Asset Class - the Singapore ExperienceFrom EverandThe Versatility of the Real Estate Asset Class - the Singapore ExperienceNo ratings yet

- Singapore Equity Research | Ezion Holdings Shows ResilienceDocument5 pagesSingapore Equity Research | Ezion Holdings Shows ResilienceventriaNo ratings yet

- Thailand: Bangkok LandDocument15 pagesThailand: Bangkok LandVishan SharmaNo ratings yet

- Indiabulls Group Presentation - 111113Document37 pagesIndiabulls Group Presentation - 111113Ritesh VarmaNo ratings yet

- Cambridge Ind Trust - DBSDocument17 pagesCambridge Ind Trust - DBSTerence Seah Pei ChuanNo ratings yet

- City Developments Downgraded to Sell on Residential Uncertainties; Hotel Segment Remains FirmDocument6 pagesCity Developments Downgraded to Sell on Residential Uncertainties; Hotel Segment Remains FirmJay NgNo ratings yet

- Newz Bits: Highlights of The DayDocument10 pagesNewz Bits: Highlights of The DaytheheavybolterNo ratings yet

- Igb IpoDocument39 pagesIgb IpoPhara MustaphaNo ratings yet

- Ocus Ocus Ocus: Colombo Stock Market Colombo Stock Market Colombo Stock MarketDocument25 pagesOcus Ocus Ocus: Colombo Stock Market Colombo Stock Market Colombo Stock MarketRandora LkNo ratings yet

- BRDB Announcement - Joint Ventures Withh MPHBDocument6 pagesBRDB Announcement - Joint Ventures Withh MPHBjohn1122334455No ratings yet

- SOBHA DEVELOPERS LTD Investor PresentationDocument29 pagesSOBHA DEVELOPERS LTD Investor PresentationSobha Developers Ltd.No ratings yet

- JKH - WPL Rights Issue Update - 20131021Document10 pagesJKH - WPL Rights Issue Update - 20131021Randora LkNo ratings yet

- (Underweight) : PlantationsDocument5 pages(Underweight) : Plantationsahmad_subhan1832No ratings yet

- AFR Stockland Exits Retirement Living With $987m Sale To EQT, Profit RisesDocument4 pagesAFR Stockland Exits Retirement Living With $987m Sale To EQT, Profit Risesroshan24No ratings yet

- DBRealty AnandRathi 061010Document135 pagesDBRealty AnandRathi 061010Adishree AgarwalNo ratings yet

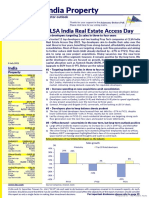

- India Property: CLSA India Real Estate Access DayDocument21 pagesIndia Property: CLSA India Real Estate Access DayManideep KumarNo ratings yet

- The Real Deals (19-07-2012)Document9 pagesThe Real Deals (19-07-2012)SG PropTalkNo ratings yet

- RHB Equity 360° (Genting Singapore, Cement, Furniture, Allianz, Top Glove, EPIC Technical: Measat) - 27/04/2010Document4 pagesRHB Equity 360° (Genting Singapore, Cement, Furniture, Allianz, Top Glove, EPIC Technical: Measat) - 27/04/2010Rhb InvestNo ratings yet

- Fundamental Analysis DLFDocument5 pagesFundamental Analysis DLFNidhisha VarshneyNo ratings yet

- Keppel Investment ReportDocument30 pagesKeppel Investment ReportMarina100% (1)

- Property Perfect Trading Buy: Catalysts in Potential Turnaround and GainsDocument10 pagesProperty Perfect Trading Buy: Catalysts in Potential Turnaround and GainsbodaiNo ratings yet

- DB Realty LTD IPO Crisil ReportDocument20 pagesDB Realty LTD IPO Crisil Reportakhil_agarwal2006No ratings yet

- The Real Deals (22-11-2012)Document9 pagesThe Real Deals (22-11-2012)SG PropTalkNo ratings yet

- Morning Pack: Regional EquitiesDocument59 pagesMorning Pack: Regional Equitiesmega_richNo ratings yet

- Singapore Property Weekly Issue 3Document19 pagesSingapore Property Weekly Issue 3Propwise.sgNo ratings yet

- Undervalued Sabah PlantersDocument9 pagesUndervalued Sabah PlantersNorazmi Abdul RahmanNo ratings yet

- RHB Equity 360° - 13 September 2010 (Emas Kiara, Banks, Mah Sing, SP Setia Technical: TDC, WCT)Document4 pagesRHB Equity 360° - 13 September 2010 (Emas Kiara, Banks, Mah Sing, SP Setia Technical: TDC, WCT)Rhb InvestNo ratings yet

- 6 July 2015 2Document1 page6 July 2015 2Ady HasbullahNo ratings yet

- Oberoi Realty Initiation ReportDocument16 pagesOberoi Realty Initiation ReportHardik GandhiNo ratings yet

- Sunteck ShareDocument4 pagesSunteck ShareLalit AgrawalNo ratings yet

- RHB Equity 360° (Axiata, Furniture, Kossan Technical: IJM) - 22/04/2010Document3 pagesRHB Equity 360° (Axiata, Furniture, Kossan Technical: IJM) - 22/04/2010Rhb InvestNo ratings yet

- 3-Way MergerDocument20 pages3-Way MergerNur 'AtiqahNo ratings yet

- 2013-5-13 Big OcbcDocument5 pages2013-5-13 Big OcbcphuawlNo ratings yet

- Singapore Property Weekly Issue 57Document14 pagesSingapore Property Weekly Issue 57Propwise.sgNo ratings yet

- Report on DLF Pvt Ltd's operations and performanceDocument25 pagesReport on DLF Pvt Ltd's operations and performanceMayank SharmaNo ratings yet

- RHB Equity 360° - 1 September 2010 (Benchmarking, Property, Semicon, O&G, Sunway City, Glomac, Maxis, Kurnia Asia, KPJ, KNM Technical: UMW)Document5 pagesRHB Equity 360° - 1 September 2010 (Benchmarking, Property, Semicon, O&G, Sunway City, Glomac, Maxis, Kurnia Asia, KPJ, KNM Technical: UMW)Rhb InvestNo ratings yet

- Ca-Final SFM Question Paper Nov 13Document11 pagesCa-Final SFM Question Paper Nov 13Pravinn_MahajanNo ratings yet

- Singapore Property Weekly Issue 46Document15 pagesSingapore Property Weekly Issue 46Propwise.sgNo ratings yet

- Singapore Property Weekly Issue 18Document13 pagesSingapore Property Weekly Issue 18Propwise.sgNo ratings yet

- Sri Lanka Real Estate Market Brief Jan 2012 (Softcopy)Document10 pagesSri Lanka Real Estate Market Brief Jan 2012 (Softcopy)nerox87No ratings yet

- A R 2009Document30 pagesA R 2009pauperprinceNo ratings yet

- JV Capital Services Pvt. LTD: WWW - Sharetrading.inDocument6 pagesJV Capital Services Pvt. LTD: WWW - Sharetrading.inpraneet singhNo ratings yet

- HKEX & LME 15june2012Document4 pagesHKEX & LME 15june2012tansillyNo ratings yet

- Reliance Infrastructure 091113 01Document4 pagesReliance Infrastructure 091113 01Vishakha KhannaNo ratings yet

- Kinross Gold Corporation: Institutional Equity Research Intraday NoteDocument6 pagesKinross Gold Corporation: Institutional Equity Research Intraday NoteAvi CohenNo ratings yet

- Sgproperty260508 OW DbsDocument6 pagesSgproperty260508 OW DbskohmandoNo ratings yet

- Last 5 Years Mergers and Acquisitions in Banking and Financial SectorDocument5 pagesLast 5 Years Mergers and Acquisitions in Banking and Financial SectorAshok GeorgeNo ratings yet

- DB Realty - Bamboo Hotels - Marine Drive Hospitality & Realty - Prestige GroupDocument3 pagesDB Realty - Bamboo Hotels - Marine Drive Hospitality & Realty - Prestige Grouptowaf57520No ratings yet

- Market Outlook 040113Document14 pagesMarket Outlook 040113Angel BrokingNo ratings yet

- Aily Review: Market Statistics All Share Price IndexDocument9 pagesAily Review: Market Statistics All Share Price IndexRandora LkNo ratings yet

- Initiating Coverage On JP Associates LTDDocument23 pagesInitiating Coverage On JP Associates LTDVarun YadavNo ratings yet

- Agricultural Bank of China Hold: Asset Restructuring Takes TimeDocument17 pagesAgricultural Bank of China Hold: Asset Restructuring Takes TimeShi HuangaoNo ratings yet

- RHB Equity 360° (Market, Motor, Ta Ann, Evergreen, ILB, MAS Technical: MAS) - 17/08/2010Document4 pagesRHB Equity 360° (Market, Motor, Ta Ann, Evergreen, ILB, MAS Technical: MAS) - 17/08/2010Rhb InvestNo ratings yet

- OSEA-Building Up Momentum... HC For Free!-BUYDocument16 pagesOSEA-Building Up Momentum... HC For Free!-BUYran2013No ratings yet

- Glencore 31 5 11Document6 pagesGlencore 31 5 11Chandra ChadalawadaNo ratings yet

- Colombo Stock Market: ASI Daily ClosingDocument24 pagesColombo Stock Market: ASI Daily ClosingRandora LkNo ratings yet

- News Bulletin - August 2013Document11 pagesNews Bulletin - August 2013Randora LkNo ratings yet

- DB Realty Limited: Another Mumbai-Based PlayerDocument8 pagesDB Realty Limited: Another Mumbai-Based PlayerVahni SinghNo ratings yet

- 2010 May - Morning Pack (DBS Group) For Asian StocksDocument62 pages2010 May - Morning Pack (DBS Group) For Asian StocksShipforNo ratings yet

- Adrian Wee DWMDDocument72 pagesAdrian Wee DWMDNorazmi Abdul Rahman0% (1)

- Complete Continuous Quran Dictionary-32 Pages-EnglishDocument32 pagesComplete Continuous Quran Dictionary-32 Pages-Englishasiksa2010No ratings yet

- Serenia Residential E Brochure FA-1Document9 pagesSerenia Residential E Brochure FA-1Norazmi Abdul RahmanNo ratings yet

- Trade Online With M+ OnlineDocument1 pageTrade Online With M+ OnlineNorazmi Abdul RahmanNo ratings yet

- Paraiso PDFDocument6 pagesParaiso PDFNorazmi Abdul RahmanNo ratings yet

- CIMB Share MarginDocument1 pageCIMB Share MarginNorazmi Abdul RahmanNo ratings yet

- Agile PDFDocument13 pagesAgile PDFNorazmi Abdul RahmanNo ratings yet

- KSL Mutiara Bestari, Johor BahruDocument20 pagesKSL Mutiara Bestari, Johor BahruNorazmi Abdul RahmanNo ratings yet

- Escape to Hilltop Homes at Bukit Rahman Putra SanctuaryDocument22 pagesEscape to Hilltop Homes at Bukit Rahman Putra SanctuaryNorazmi Abdul RahmanNo ratings yet

- Begonia BrochureDocument2 pagesBegonia BrochureNorazmi Abdul RahmanNo ratings yet

- Verdi Floor PlanDocument4 pagesVerdi Floor PlanNorazmi Abdul RahmanNo ratings yet

- Floor Plans - Type A and SpecificationsDocument2 pagesFloor Plans - Type A and SpecificationsNorazmi Abdul RahmanNo ratings yet

- Maybank IB SU 2013-01-14 Property Sector Pain First Gain Later 2873Document17 pagesMaybank IB SU 2013-01-14 Property Sector Pain First Gain Later 2873Norazmi Abdul RahmanNo ratings yet

- Undervalued Sabah PlantersDocument9 pagesUndervalued Sabah PlantersNorazmi Abdul RahmanNo ratings yet

- My Salary Guide2012-2013Document15 pagesMy Salary Guide2012-2013Chandra Adi PradanaNo ratings yet

- Malaysia My Second Home (MM2H)Document2 pagesMalaysia My Second Home (MM2H)Norazmi Abdul RahmanNo ratings yet

- Undervalued Sabah PlantersDocument9 pagesUndervalued Sabah PlantersNorazmi Abdul RahmanNo ratings yet

- CHGS EleafletDocument4 pagesCHGS EleafletNorazmi Abdul RahmanNo ratings yet

- Presentation On DAP PJ DinnerDocument24 pagesPresentation On DAP PJ DinnerNorazmi Abdul RahmanNo ratings yet

- Construction & Property 2013Document8 pagesConstruction & Property 2013Tam AbdullahNo ratings yet

- ISOVERDocument35 pagesISOVERMadhu RaghuNo ratings yet

- Mechanical CalculationsDocument34 pagesMechanical CalculationsNorazmi Abdul RahmanNo ratings yet

- Duct CalculatorDocument1 pageDuct CalculatorNorazmi Abdul RahmanNo ratings yet

- Phoenix Metals Product Catalog 2012Document42 pagesPhoenix Metals Product Catalog 2012Norazmi Abdul RahmanNo ratings yet

- How To Run The Web ProgramDocument2 pagesHow To Run The Web ProgramNorazmi Abdul RahmanNo ratings yet

- Backward Curved Centrifugal ApplicationDocument2 pagesBackward Curved Centrifugal ApplicationNorazmi Abdul RahmanNo ratings yet

- Zeta DeskyeDocument24 pagesZeta DeskyeNorazmi Abdul RahmanNo ratings yet

- Forward Curved Centrifugal Fan ApplicationDocument3 pagesForward Curved Centrifugal Fan ApplicationNorazmi Abdul Rahman100% (1)

- Service Marketing 3 - (Marketing Mix)Document123 pagesService Marketing 3 - (Marketing Mix)Soumya Jyoti BhattacharyaNo ratings yet

- FP&A Interview Q TechnicalDocument17 pagesFP&A Interview Q Technicalsonu malikNo ratings yet

- Hercules Exercise Equipment Co Purchased A Computerized Measuring Device TwoDocument1 pageHercules Exercise Equipment Co Purchased A Computerized Measuring Device TwoAmit PandeyNo ratings yet

- A Study On Investors Buying Behaviour Towards Mutual Fund PDF FreeDocument143 pagesA Study On Investors Buying Behaviour Towards Mutual Fund PDF FreeRathod JayeshNo ratings yet

- Notes # 2 - Fundamentals of Real Estate Management PDFDocument3 pagesNotes # 2 - Fundamentals of Real Estate Management PDFGessel Xan Lopez100% (2)

- The MBA DecisionDocument7 pagesThe MBA DecisionFiry YuanditaNo ratings yet

- Travis Kalanick and UberDocument3 pagesTravis Kalanick and UberHarsh GadhiyaNo ratings yet

- Hindusthan Microfinance provides loans to Mumbai's poorDocument25 pagesHindusthan Microfinance provides loans to Mumbai's poorsunnyNo ratings yet

- HTTPSWWW Sec GovArchivesedgardata1057791000105779114000008ex991 PDFDocument99 pagesHTTPSWWW Sec GovArchivesedgardata1057791000105779114000008ex991 PDFДмитрий ЮхановNo ratings yet

- Jharkhand Govt Gazette Regarding Stipend For LawyersDocument6 pagesJharkhand Govt Gazette Regarding Stipend For LawyersLatest Laws TeamNo ratings yet

- Teaching Market Making with a Game SimulationDocument4 pagesTeaching Market Making with a Game SimulationRamkrishna LanjewarNo ratings yet

- Cooperative ManualDocument35 pagesCooperative ManualPratik MogheNo ratings yet

- Essentials of a Contract - Formation, Validity, Performance & DischargeDocument25 pagesEssentials of a Contract - Formation, Validity, Performance & Dischargesjkushwaha21100% (1)

- Reauthorization of The National Flood Insurance ProgramDocument137 pagesReauthorization of The National Flood Insurance ProgramScribd Government DocsNo ratings yet

- LTD Report Innocent Purchaser For ValueDocument3 pagesLTD Report Innocent Purchaser For ValuebcarNo ratings yet

- ESCHEATS AND TRUSTEE RULESDocument6 pagesESCHEATS AND TRUSTEE RULESJames Ibrahim AlihNo ratings yet

- Cio Rajeev Thakkar's Note On Parag Parikh Flexi Cap FundDocument3 pagesCio Rajeev Thakkar's Note On Parag Parikh Flexi Cap FundSaswat PremNo ratings yet

- Croissance Economique Taux Change Donnees Panel RegimesDocument326 pagesCroissance Economique Taux Change Donnees Panel RegimesSalah OuyabaNo ratings yet

- Information Collection Survey For The Mega Manila Subway Project in The Republic of The PhilippinesDocument226 pagesInformation Collection Survey For The Mega Manila Subway Project in The Republic of The PhilippinesLian Las Pinas100% (2)

- Deco404 Public Finance Hindi PDFDocument404 pagesDeco404 Public Finance Hindi PDFRaju Chouhan RajNo ratings yet

- Sinhgad Institute of Management - Research TopicsDocument17 pagesSinhgad Institute of Management - Research TopicsAnmol LimpaleNo ratings yet

- Office Stationery Manufacturing in The US Industry ReportDocument40 pagesOffice Stationery Manufacturing in The US Industry Reportdr_digital100% (1)

- The Land Acquisition Act 1894Document25 pagesThe Land Acquisition Act 1894Shahid Jamal TubrazyNo ratings yet

- International Financial Management Chapter 6 - Government Influence On Exchang RateDocument54 pagesInternational Financial Management Chapter 6 - Government Influence On Exchang RateAmelya Husen100% (2)

- Pro Forma Invoice: Proline TechnologiesDocument1 pagePro Forma Invoice: Proline TechnologiesKanth KodaliNo ratings yet

- Aavas FinanciersDocument8 pagesAavas FinanciersSirish GopalanNo ratings yet

- Credit Risk ManagementDocument4 pagesCredit Risk ManagementinspectorsufiNo ratings yet

- Vip No.8 - MeslDocument4 pagesVip No.8 - Meslkj gandaNo ratings yet

- List of Consultants For Solar Power Plant InstallationDocument6 pagesList of Consultants For Solar Power Plant InstallationSanjeev Agarwal0% (1)

- Fertilizer - Urea Offtake Update - AHLDocument3 pagesFertilizer - Urea Offtake Update - AHLmuddasir1980No ratings yet