You might also like

- Asia Small and Medium-Sized Enterprise Monitor 2020: Volume IV: Technical Note—Designing a Small and Medium-Sized Enterprise Development IndexFrom EverandAsia Small and Medium-Sized Enterprise Monitor 2020: Volume IV: Technical Note—Designing a Small and Medium-Sized Enterprise Development IndexNo ratings yet

- A Study On Performance of BanksDocument115 pagesA Study On Performance of BanksAnuj KadelNo ratings yet

- Indonesia and the Asian Development Bank: Fifty Years of Development in IndonesiaFrom EverandIndonesia and the Asian Development Bank: Fifty Years of Development in IndonesiaNo ratings yet

- Npa Management SbiDocument104 pagesNpa Management Sbiparth jani100% (1)

- Human Capital Development in South Asia: Achievements, Prospects, and Policy ChallengesFrom EverandHuman Capital Development in South Asia: Achievements, Prospects, and Policy ChallengesNo ratings yet

- Report On Mutual Fund AnalysisDocument56 pagesReport On Mutual Fund AnalysisYv Vardar100% (1)

- The Social Protection Indicator: Assessing Results for AsiaFrom EverandThe Social Protection Indicator: Assessing Results for AsiaNo ratings yet

- Sip ProjectDocument126 pagesSip Projectsolanki_dipen2000100% (2)

- Realizing the Potential of Public–Private Partnerships to Advance Asia's Infrastructure DevelopmentFrom EverandRealizing the Potential of Public–Private Partnerships to Advance Asia's Infrastructure DevelopmentNo ratings yet

- Final Sip Mba Project PDFDocument87 pagesFinal Sip Mba Project PDFRinkesh Modi93% (14)

- Snapshot of Sustainable Development Goals at the Subnational Government Level in IndonesiaFrom EverandSnapshot of Sustainable Development Goals at the Subnational Government Level in IndonesiaNo ratings yet

- Non-Performing Assets: A Study of State Bank of India: Dr.D.Ganesan R.SanthanakrishnanDocument8 pagesNon-Performing Assets: A Study of State Bank of India: Dr.D.Ganesan R.SanthanakrishnansusheelNo ratings yet

- In Partial Fulfillment of Requirements For The Award of Requirement ofDocument30 pagesIn Partial Fulfillment of Requirements For The Award of Requirement ofSanket KambleNo ratings yet

- Azerbaijan: Moving Toward More Diversified, Resilient, and Inclusive DevelopmentFrom EverandAzerbaijan: Moving Toward More Diversified, Resilient, and Inclusive DevelopmentNo ratings yet

- Research Study On Loan Default by SHGDocument101 pagesResearch Study On Loan Default by SHGramaknta100% (1)

- A Case Study of Barclays LoansDocument64 pagesA Case Study of Barclays Loansaditya_naluNo ratings yet

- The Evolution of NBFCS: Analysing Financial Performance of Selected NBFCs in IndiaDocument11 pagesThe Evolution of NBFCS: Analysing Financial Performance of Selected NBFCs in IndiaSeetanNo ratings yet

- Post-Graduate Programme in Management: To The Aravali Institute of Management, JodhpurDocument54 pagesPost-Graduate Programme in Management: To The Aravali Institute of Management, JodhpurJitendra Singh SolankiNo ratings yet

- PRABHJOTDocument86 pagesPRABHJOTgurjeet08No ratings yet

- Financial Performance of Sri Bharamaramba Pattina Souharda Sahakari Niyamita MaskiDocument3 pagesFinancial Performance of Sri Bharamaramba Pattina Souharda Sahakari Niyamita MaskiBasavaraj KustagiNo ratings yet

- Lecturer of Business Management Project Report Submitted in Partial Fulfillment For The Award of Degree ofDocument93 pagesLecturer of Business Management Project Report Submitted in Partial Fulfillment For The Award of Degree ofsohailsamNo ratings yet

- Globalization of Indian Banking SectorDocument15 pagesGlobalization of Indian Banking SectorRimpiKaur60% (5)

- Duplict. A Study On Performance Evaluation of Icici and Sbi Using Fundamental and Technical AnalysisDocument52 pagesDuplict. A Study On Performance Evaluation of Icici and Sbi Using Fundamental and Technical AnalysisRahul NairNo ratings yet

- Demat Feasibility Working of HSL As A Depository ParticipaDocument88 pagesDemat Feasibility Working of HSL As A Depository ParticipaNeeraj Katewa100% (1)

- Mba Winter 2019Document3 pagesMba Winter 2019fsdNo ratings yet

- Positioning Strategy For Pulsar and Its EffectDocument65 pagesPositioning Strategy For Pulsar and Its EffectSuresh Babu Reddy100% (1)

- Summary O. F Findings, Conclusion: and SuggestionsDocument18 pagesSummary O. F Findings, Conclusion: and SuggestionsVįňäý Ğøwđã VįñîNo ratings yet

- Sbi Project 2021Document44 pagesSbi Project 2021rasnapowderNo ratings yet

- Summer Internship Project of Icicidirect - Com On Comparative AnalysisDocument123 pagesSummer Internship Project of Icicidirect - Com On Comparative Analysisjatin92% (26)

- Jagriti CUSTOMER ATTITUDE TOWARDS HDFC CREDIT CARDSDocument103 pagesJagriti CUSTOMER ATTITUDE TOWARDS HDFC CREDIT CARDSAkash SinghNo ratings yet

- A Study On Trend Analysis of Maruti Suzu PDFDocument8 pagesA Study On Trend Analysis of Maruti Suzu PDFSanyam SinghNo ratings yet

- A Study On Trend Analysis of Maruti Suzuki India Limited': M. Yasodha, G. Sharmila, A. S. Subashree & K. YamunadeviDocument8 pagesA Study On Trend Analysis of Maruti Suzuki India Limited': M. Yasodha, G. Sharmila, A. S. Subashree & K. YamunadeviTJPRC PublicationsNo ratings yet

- Deepika Singh Six Sigma 1101Document34 pagesDeepika Singh Six Sigma 1101Amit SinghNo ratings yet

- Muthootfincorpltd 130220131348 Phpapp02Document123 pagesMuthootfincorpltd 130220131348 Phpapp02Abner Alexander Luiz100% (1)

- Abhudaya Bank ProfileDocument57 pagesAbhudaya Bank ProfileMona KonarNo ratings yet

- SIP ProjectDocument43 pagesSIP ProjectTina WaghmareNo ratings yet

- Sip Report - 1908480700001 Aamir SuhailDocument169 pagesSip Report - 1908480700001 Aamir SuhailAkash SinghNo ratings yet

- BankingDocument75 pagesBankingGenesian Nikhilesh PillayNo ratings yet

- Agrani Bank LimitedDocument47 pagesAgrani Bank Limitedgoogle accountNo ratings yet

- Prestige Institute of Management & Research, Indore: "Analysis of Stock Market at Arihant Capital"Document27 pagesPrestige Institute of Management & Research, Indore: "Analysis of Stock Market at Arihant Capital"Samyak JainNo ratings yet

- Project Report On SIP in Mutual FundsDocument76 pagesProject Report On SIP in Mutual FundsAnubhav Sood100% (6)

- Ipru Value Discovery FundDocument4 pagesIpru Value Discovery FundJ.K. GarnayakNo ratings yet

- Recent Trends of PE Funding in IndiaDocument38 pagesRecent Trends of PE Funding in IndiaProf Dr Chowdari PrasadNo ratings yet

- Admission Schedule 1920Document13 pagesAdmission Schedule 1920Kallol Kumar DihingiaNo ratings yet

- BDV01I03P0207Document9 pagesBDV01I03P0207BusinessdimensionsNo ratings yet

- Mukesh Yadav Kingfisher Project in JaipurDocument89 pagesMukesh Yadav Kingfisher Project in JaipurMUKESH YADAVNo ratings yet

- ICICIdirect MahindraLifespace Coverage PDFDocument27 pagesICICIdirect MahindraLifespace Coverage PDFsantu13No ratings yet

- Chapter - 6 Summary of Conclusions, Findings, Recommendations and Direction For Future ResearchDocument11 pagesChapter - 6 Summary of Conclusions, Findings, Recommendations and Direction For Future ResearchDushyant MudgalNo ratings yet

- SAIL Internship Project 2010-11Document47 pagesSAIL Internship Project 2010-11Avneet Ahuja91% (11)

- Summer Internship Project Report On Analysis of Credit Appraisal at Bank of IndiaDocument127 pagesSummer Internship Project Report On Analysis of Credit Appraisal at Bank of IndiaGaurav Narang82% (11)

- Dissertation Report On: Marketing Strategy of Dabur Vatika Hair Oil & Dabur Chyawanprash'Document54 pagesDissertation Report On: Marketing Strategy of Dabur Vatika Hair Oil & Dabur Chyawanprash'su_pathriaNo ratings yet

- Business Correspondant Model in FI-ProjectDocument51 pagesBusiness Correspondant Model in FI-ProjectcprabhashNo ratings yet

- Banking & InsuranceDocument11 pagesBanking & InsuranceDinesh BhandariNo ratings yet

- Summer Intership Project Bajaj FinservDocument51 pagesSummer Intership Project Bajaj FinservAMBIYA JAGIRDAR50% (2)

- 1053 1006 FileDocument324 pages1053 1006 FiledibyaNo ratings yet

- A Study On Financial Perpormance at Muthoot Finance LTDDocument6 pagesA Study On Financial Perpormance at Muthoot Finance LTDCenu Roman33% (3)

- Sharekhan Internship ProjectDocument74 pagesSharekhan Internship Projectayush goyalNo ratings yet

- Archi Summer ReportDocument44 pagesArchi Summer Reportadhiraj singhNo ratings yet

- Programme Structure For PG-BDocument35 pagesProgramme Structure For PG-BrssnathanNo ratings yet

- 47-Corporate Salary Package - CSPDocument3 pages47-Corporate Salary Package - CSPmevrick_guyNo ratings yet

- IBPS Interview Prep - Graduation Related Questions BE, BCom, BADocument33 pagesIBPS Interview Prep - Graduation Related Questions BE, BCom, BAmevrick_guyNo ratings yet

- 9th Issue E-Gyan May, 2014 PDFDocument17 pages9th Issue E-Gyan May, 2014 PDFmevrick_guyNo ratings yet

- NIOS Culture NotesDocument71 pagesNIOS Culture Notesmevrick_guy0% (1)

- 1st Issue E-Gyan, July-2013Document13 pages1st Issue E-Gyan, July-2013mevrick_guyNo ratings yet

- 01.15 Bod EodDocument25 pages01.15 Bod Eodmevrick_guy100% (1)

- 01.20 Government BusinessDocument48 pages01.20 Government Businessmevrick_guyNo ratings yet

- 01.09-User System ManagementDocument12 pages01.09-User System Managementmevrick_guyNo ratings yet

- 01 21-RBIremittanceDocument11 pages01 21-RBIremittancemevrick_guyNo ratings yet

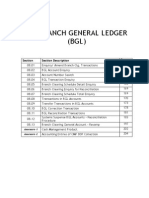

- 8 To 8 Functionality: Section Section DescriptionDocument7 pages8 To 8 Functionality: Section Section Descriptionmevrick_guyNo ratings yet

- 01.19 Safe CustodyDocument9 pages01.19 Safe Custodymevrick_guyNo ratings yet

- 01.15 Bod EodDocument25 pages01.15 Bod Eodmevrick_guy100% (1)

- 01.17 Currency ChestDocument10 pages01.17 Currency Chestmevrick_guyNo ratings yet

- 01.13 ClearingDocument38 pages01.13 Clearingmevrick_guy0% (1)

- 01.14 Maker Checker FunctionalitiesDocument19 pages01.14 Maker Checker Functionalitiesmevrick_guyNo ratings yet

- 01.10 RemittancesDocument40 pages01.10 Remittancesmevrick_guyNo ratings yet

- 01.12 Posting RestrictionsDocument14 pages01.12 Posting Restrictionsmevrick_guyNo ratings yet

- 01.05 Transaction ProcessingDocument23 pages01.05 Transaction Processingmevrick_guyNo ratings yet

- 01.04-DepositAccounts Other FunctionalitiesDocument30 pages01.04-DepositAccounts Other Functionalitiesmevrick_guyNo ratings yet

- 01 08-BGLDocument40 pages01 08-BGLmevrick_guy100% (2)

- Customer Service - Point of EncounterDocument3 pagesCustomer Service - Point of Encountermevrick_guyNo ratings yet

- IT-Mobile Banking & Wallet: P-REVIEW March 2012Document10 pagesIT-Mobile Banking & Wallet: P-REVIEW March 2012mevrick_guyNo ratings yet

- 01 02-CifDocument25 pages01 02-Cifmevrick_guyNo ratings yet

- 01 06-CashDocument21 pages01 06-Cashmevrick_guyNo ratings yet

- 01.03-Deposit Accounts OpeningDocument38 pages01.03-Deposit Accounts Openingmevrick_guy0% (1)

- Promotion Book 2011Document535 pagesPromotion Book 2011mevrick_guy100% (1)

- 532-27-10-2009 - Gold Debit CardDocument3 pages532-27-10-2009 - Gold Debit Cardmevrick_guyNo ratings yet

- Measuring Customer Satisfaction in The Banking IndustryDocument9 pagesMeasuring Customer Satisfaction in The Banking Industrymevrick_guyNo ratings yet

- 01.01 IntroductionDocument16 pages01.01 Introductionmevrick_guyNo ratings yet

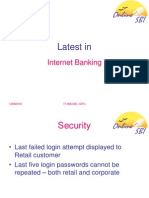

- Latest In: Internet BankingDocument9 pagesLatest In: Internet Bankingmevrick_guyNo ratings yet

- Managing Your Innovation Portfolio Puneet Agarwal (EPGP Roll No: 1914002) Individual AssignmentDocument1 pageManaging Your Innovation Portfolio Puneet Agarwal (EPGP Roll No: 1914002) Individual AssignmentPuneet AgarwalNo ratings yet

- ZTMB Name ChangeDocument4 pagesZTMB Name Changeshenaz khanNo ratings yet

- Action To Recover DamagesDocument4 pagesAction To Recover DamagesSui100% (1)

- Ifrs at A Glance: IFRS 12 Disclosure of Interests in OtherDocument6 pagesIfrs at A Glance: IFRS 12 Disclosure of Interests in OtherJoshua Capa FrondaNo ratings yet

- T3TSL - Syndicated Loans - R14Document283 pagesT3TSL - Syndicated Loans - R14tayutaNo ratings yet

- FRMJorion 14 Hedging Linear RiskDocument51 pagesFRMJorion 14 Hedging Linear RiskZishan KhanNo ratings yet

- Great Cash Wonder (Launch) Write-UpDocument8 pagesGreat Cash Wonder (Launch) Write-UpAlex GeorgeNo ratings yet

- Linde India Limited - Delisting Letter of Offer - 140120191028Document48 pagesLinde India Limited - Delisting Letter of Offer - 140120191028Arushi ChaudharyNo ratings yet

- Agency ProblemDocument6 pagesAgency ProblemZarkaif KhanNo ratings yet

- Chapter 7 Financial Statement Analysis 2011Document49 pagesChapter 7 Financial Statement Analysis 2011Mohd Fathil Pok SuNo ratings yet

- Fundamental and Technical Analysis For Idiots Part 2Document33 pagesFundamental and Technical Analysis For Idiots Part 2Nataraja UpadhyaNo ratings yet

- Interviews Value InvestingDocument87 pagesInterviews Value Investinghkm_gmat4849100% (1)

- FIN 420 Chapter 9 (Long Term Financing)Document17 pagesFIN 420 Chapter 9 (Long Term Financing)Halim NordinNo ratings yet

- Forbes India January 19 2018Document105 pagesForbes India January 19 2018FASHION HUTNo ratings yet

- Strategies LOW VOLATILITYDocument8 pagesStrategies LOW VOLATILITYbla blaNo ratings yet

- StrategiesDocument1 pageStrategiesMiksi 6No ratings yet

- prc-2015-spl Pays Cir Memo 3572 DT 18-6-15Document3 pagesprc-2015-spl Pays Cir Memo 3572 DT 18-6-15api-215249734No ratings yet

- SPE 134014 (Olsen) Reserves Overbooking Problem We Re Going To Talk AboutDocument11 pagesSPE 134014 (Olsen) Reserves Overbooking Problem We Re Going To Talk AboutHUGO BARRIOS DRULLISNo ratings yet

- Marketing QuestionsDocument3 pagesMarketing QuestionsNAZMUL HAQUENo ratings yet

- CBAE BSBAFM 1stterm1stsem FM211Document62 pagesCBAE BSBAFM 1stterm1stsem FM211Nikka NatadNo ratings yet

- Bank LendingDocument32 pagesBank LendingFRANCIS JOSEPHNo ratings yet

- Director Investment Banking in NYC NY Resume Pascal KabembaDocument2 pagesDirector Investment Banking in NYC NY Resume Pascal KabembaPascalKabemba100% (1)

- Effect of Foreign Institutional Investors On Corporate Board Attributes A Literature ReviewDocument7 pagesEffect of Foreign Institutional Investors On Corporate Board Attributes A Literature ReviewRiya CassendraNo ratings yet

- Securities Fraud in The Courts by Bo WaltersDocument27 pagesSecurities Fraud in The Courts by Bo WaltersBrady James85% (13)

- Adaptive Markets - Andrew LoDocument22 pagesAdaptive Markets - Andrew LoQuickie Sanders100% (4)

- Trade StoryDocument12 pagesTrade Storyamos amosNo ratings yet

- Full Text of Federal Reserve Chairman Ben Bernanke's Speech in Jackson Hole, Wyo.Document8 pagesFull Text of Federal Reserve Chairman Ben Bernanke's Speech in Jackson Hole, Wyo.lawrenceNo ratings yet

- Ethics Finance SyllabusDocument6 pagesEthics Finance SyllabusAfiqah RasidiNo ratings yet

- CHAPTER 14 Business Combination PFRS 3Document3 pagesCHAPTER 14 Business Combination PFRS 3Richard DuranNo ratings yet

- Microfinance in Developed CountriesDocument11 pagesMicrofinance in Developed CountriesSomesh SrivastavaNo ratings yet

- The Compound Effect by Darren Hardy - Book Summary: Jumpstart Your Income, Your Life, Your SuccessFrom EverandThe Compound Effect by Darren Hardy - Book Summary: Jumpstart Your Income, Your Life, Your SuccessRating: 5 out of 5 stars5/5 (456)

- Summary of 12 Rules for Life: An Antidote to ChaosFrom EverandSummary of 12 Rules for Life: An Antidote to ChaosRating: 4.5 out of 5 stars4.5/5 (294)

- Can't Hurt Me by David Goggins - Book Summary: Master Your Mind and Defy the OddsFrom EverandCan't Hurt Me by David Goggins - Book Summary: Master Your Mind and Defy the OddsRating: 4.5 out of 5 stars4.5/5 (386)

- Summary: Atomic Habits by James Clear: An Easy & Proven Way to Build Good Habits & Break Bad OnesFrom EverandSummary: Atomic Habits by James Clear: An Easy & Proven Way to Build Good Habits & Break Bad OnesRating: 5 out of 5 stars5/5 (1636)

- The Body Keeps the Score by Bessel Van der Kolk, M.D. - Book Summary: Brain, Mind, and Body in the Healing of TraumaFrom EverandThe Body Keeps the Score by Bessel Van der Kolk, M.D. - Book Summary: Brain, Mind, and Body in the Healing of TraumaRating: 4.5 out of 5 stars4.5/5 (266)

- Summary of Eat to Beat Disease by Dr. William LiFrom EverandSummary of Eat to Beat Disease by Dr. William LiRating: 5 out of 5 stars5/5 (52)

- Summary of The Anxious Generation by Jonathan Haidt: How the Great Rewiring of Childhood Is Causing an Epidemic of Mental IllnessFrom EverandSummary of The Anxious Generation by Jonathan Haidt: How the Great Rewiring of Childhood Is Causing an Epidemic of Mental IllnessNo ratings yet

- Summary of The New Menopause by Mary Claire Haver MD: Navigating Your Path Through Hormonal Change with Purpose, Power, and FactsFrom EverandSummary of The New Menopause by Mary Claire Haver MD: Navigating Your Path Through Hormonal Change with Purpose, Power, and FactsNo ratings yet

- The One Thing: The Surprisingly Simple Truth Behind Extraordinary ResultsFrom EverandThe One Thing: The Surprisingly Simple Truth Behind Extraordinary ResultsRating: 4.5 out of 5 stars4.5/5 (709)

- How To Win Friends and Influence People by Dale Carnegie - Book SummaryFrom EverandHow To Win Friends and Influence People by Dale Carnegie - Book SummaryRating: 5 out of 5 stars5/5 (557)

- Summary of The Algebra of Wealth by Scott Galloway: A Simple Formula for Financial SecurityFrom EverandSummary of The Algebra of Wealth by Scott Galloway: A Simple Formula for Financial SecurityNo ratings yet

- Mindset by Carol S. Dweck - Book Summary: The New Psychology of SuccessFrom EverandMindset by Carol S. Dweck - Book Summary: The New Psychology of SuccessRating: 4.5 out of 5 stars4.5/5 (328)

- The War of Art by Steven Pressfield - Book Summary: Break Through The Blocks And Win Your Inner Creative BattlesFrom EverandThe War of Art by Steven Pressfield - Book Summary: Break Through The Blocks And Win Your Inner Creative BattlesRating: 4.5 out of 5 stars4.5/5 (274)

- Summary of Million Dollar Weekend by Noah Kagan and Tahl Raz: The Surprisingly Simple Way to Launch a 7-Figure Business in 48 HoursFrom EverandSummary of Million Dollar Weekend by Noah Kagan and Tahl Raz: The Surprisingly Simple Way to Launch a 7-Figure Business in 48 HoursNo ratings yet

- The Whole-Brain Child by Daniel J. Siegel, M.D., and Tina Payne Bryson, PhD. - Book Summary: 12 Revolutionary Strategies to Nurture Your Child’s Developing MindFrom EverandThe Whole-Brain Child by Daniel J. Siegel, M.D., and Tina Payne Bryson, PhD. - Book Summary: 12 Revolutionary Strategies to Nurture Your Child’s Developing MindRating: 4.5 out of 5 stars4.5/5 (57)

- Make It Stick by Peter C. Brown, Henry L. Roediger III, Mark A. McDaniel - Book Summary: The Science of Successful LearningFrom EverandMake It Stick by Peter C. Brown, Henry L. Roediger III, Mark A. McDaniel - Book Summary: The Science of Successful LearningRating: 4.5 out of 5 stars4.5/5 (55)

- The 5 Second Rule by Mel Robbins - Book Summary: Transform Your Life, Work, and Confidence with Everyday CourageFrom EverandThe 5 Second Rule by Mel Robbins - Book Summary: Transform Your Life, Work, and Confidence with Everyday CourageRating: 4.5 out of 5 stars4.5/5 (329)

- Steal Like an Artist by Austin Kleon - Book Summary: 10 Things Nobody Told You About Being CreativeFrom EverandSteal Like an Artist by Austin Kleon - Book Summary: 10 Things Nobody Told You About Being CreativeRating: 4.5 out of 5 stars4.5/5 (128)

- Essentialism by Greg McKeown - Book Summary: The Disciplined Pursuit of LessFrom EverandEssentialism by Greg McKeown - Book Summary: The Disciplined Pursuit of LessRating: 4.5 out of 5 stars4.5/5 (188)

- How Not to Die by Michael Greger MD, Gene Stone - Book Summary: Discover the Foods Scientifically Proven to Prevent and Reverse DiseaseFrom EverandHow Not to Die by Michael Greger MD, Gene Stone - Book Summary: Discover the Foods Scientifically Proven to Prevent and Reverse DiseaseRating: 4.5 out of 5 stars4.5/5 (84)

- Blink by Malcolm Gladwell - Book Summary: The Power of Thinking Without ThinkingFrom EverandBlink by Malcolm Gladwell - Book Summary: The Power of Thinking Without ThinkingRating: 4.5 out of 5 stars4.5/5 (114)

- Summary of Atomic Habits by James ClearFrom EverandSummary of Atomic Habits by James ClearRating: 5 out of 5 stars5/5 (169)

- Summary of The Galveston Diet by Mary Claire Haver MD: The Doctor-Developed, Patient-Proven Plan to Burn Fat and Tame Your Hormonal SymptomsFrom EverandSummary of The Galveston Diet by Mary Claire Haver MD: The Doctor-Developed, Patient-Proven Plan to Burn Fat and Tame Your Hormonal SymptomsNo ratings yet

- Good to Great by Jim Collins - Book Summary: Why Some Companies Make the Leap...And Others Don'tFrom EverandGood to Great by Jim Collins - Book Summary: Why Some Companies Make the Leap...And Others Don'tRating: 4.5 out of 5 stars4.5/5 (64)

- Summary of "Measure What Matters" by John Doerr: How Google, Bono, and the Gates Foundation Rock the World with OKRs — Finish Entire Book in 15 MinutesFrom EverandSummary of "Measure What Matters" by John Doerr: How Google, Bono, and the Gates Foundation Rock the World with OKRs — Finish Entire Book in 15 MinutesRating: 4.5 out of 5 stars4.5/5 (62)

- Summary of When Things Fall Apart: Heart Advice for Difficult Times by Pema ChödrönFrom EverandSummary of When Things Fall Apart: Heart Advice for Difficult Times by Pema ChödrönRating: 4.5 out of 5 stars4.5/5 (22)

- Book Summary of Ego Is The Enemy by Ryan HolidayFrom EverandBook Summary of Ego Is The Enemy by Ryan HolidayRating: 4.5 out of 5 stars4.5/5 (388)

- Summary of Supercommunicators by Charles Duhigg: How to Unlock the Secret Language of ConnectionFrom EverandSummary of Supercommunicators by Charles Duhigg: How to Unlock the Secret Language of ConnectionNo ratings yet