You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- AFC3240 Topic 03 S1 2011Document36 pagesAFC3240 Topic 03 S1 2011sittmoNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

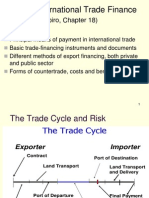

- Topic 2: International Trade Finance: (Reading: Shapiro, Chapter 18)Document15 pagesTopic 2: International Trade Finance: (Reading: Shapiro, Chapter 18)sittmoNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- International Parity Relationship: Topic 4Document32 pagesInternational Parity Relationship: Topic 4sittmoNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- AFC3240 Topic 09 S1 2011Document17 pagesAFC3240 Topic 09 S1 2011sittmoNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- AFC3240 Topic 06 S1 2011Document27 pagesAFC3240 Topic 06 S1 2011sittmoNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- AFC3240 Topic 07 S1 2011Document12 pagesAFC3240 Topic 07 S1 2011sittmoNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- AFC3240 Topic 01 S2 2010Document18 pagesAFC3240 Topic 01 S2 2010sittmoNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- AFC3240 Topic 08 S1 2011Document24 pagesAFC3240 Topic 08 S1 2011sittmoNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Sec 03Document24 pagesSec 03sittmoNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Topic Determination of Exchange Rate: Balance of Payments (BOP)Document27 pagesTopic Determination of Exchange Rate: Balance of Payments (BOP)sittmoNo ratings yet

- Sec 04Document32 pagesSec 04sittmoNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Section 2 Section 2 Intervention in Markets Intervention in MarketsDocument18 pagesSection 2 Section 2 Intervention in Markets Intervention in MarketssittmoNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Sec 01Document35 pagesSec 01sittmoNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Solving Inhomogenous Recurrence Relations 3Document4 pagesSolving Inhomogenous Recurrence Relations 3sittmoNo ratings yet

- Solving Inhomogenous Recurrence RelationsDocument3 pagesSolving Inhomogenous Recurrence Relationssittmo0% (1)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Solving Inhomogenous Recurrence Relations 2Document2 pagesSolving Inhomogenous Recurrence Relations 2sittmoNo ratings yet

- Worldwide Cost of Living 2019 Free ReportDocument14 pagesWorldwide Cost of Living 2019 Free ReportwefNo ratings yet

- Chapter1A - Financial Accounting, Fourth Canadian EditionDocument14 pagesChapter1A - Financial Accounting, Fourth Canadian EditionMuktar Ibrahim BockNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Andrejs VII International Woodwind CompetitionDocument6 pagesAndrejs VII International Woodwind CompetitionAlbani CórdovaNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- 101 Globalisation and Culture 1225869777273912 9Document35 pages101 Globalisation and Culture 1225869777273912 9Gilm AutismeNo ratings yet

- S o SpotoptionDocument8 pagesS o Spotoptionapi-165143782No ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Maths Shortcut KeysDocument7 pagesMaths Shortcut KeysRohan MalthumkarNo ratings yet

- 0320 US Fixed Income Markets WeeklyDocument96 pages0320 US Fixed Income Markets WeeklycwuuuuNo ratings yet

- Private: Managing National ParksDocument4 pagesPrivate: Managing National ParksAllãn SinclairNo ratings yet

- 2 Lease of Bank Instrument - Pof Block Funds 002aDocument1 page2 Lease of Bank Instrument - Pof Block Funds 002aapi-255857738No ratings yet

- HW1-time Value of Money SOLUÇÃODocument6 pagesHW1-time Value of Money SOLUÇÃOSahid Xerfan NetoNo ratings yet

- Annual Report Nordea Bank AB 2017 PDFDocument244 pagesAnnual Report Nordea Bank AB 2017 PDFNana DyNo ratings yet

- Analysis of Financial StatementsDocument33 pagesAnalysis of Financial StatementsAsim Mahato100% (3)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- FIN301 Outline FinalDocument13 pagesFIN301 Outline FinalArsalan AqeeqNo ratings yet

- Regional Economic IntegrationDocument56 pagesRegional Economic IntegrationberitahrNo ratings yet

- The Contemporary WorldDocument7 pagesThe Contemporary WorldRental System100% (1)

- Notes To The Annual Review 2005: DisclaimerDocument41 pagesNotes To The Annual Review 2005: DisclaimerAditya ArfanNo ratings yet

- U.S. HHS Budget For Administration For Children and Families FY 2012Document400 pagesU.S. HHS Budget For Administration For Children and Families FY 2012Beverly TranNo ratings yet

- Best Forex Indicators For Scalping: What Is A Scalping Strategy?Document9 pagesBest Forex Indicators For Scalping: What Is A Scalping Strategy?jpvjpvNo ratings yet

- Sourcing - Report SEE 2019Document23 pagesSourcing - Report SEE 2019Jovan KolovNo ratings yet

- Keown8 ch17Document30 pagesKeown8 ch17samir249No ratings yet

- The Role of Banks, Non-Banks and The Central Bank in The Money Creation ProcessDocument21 pagesThe Role of Banks, Non-Banks and The Central Bank in The Money Creation Processwm100% (1)

- Berri Case StudyDocument22 pagesBerri Case StudyNeha SinghNo ratings yet

- Quanto Options: Uwe Wystup Mathfinance Ag Waldems, GermanyDocument12 pagesQuanto Options: Uwe Wystup Mathfinance Ag Waldems, Germanyshubg87No ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Leaving The Euro A Practical Guide SummaryDocument3 pagesLeaving The Euro A Practical Guide SummaryTee RexNo ratings yet

- CEPS Activities Report 2010-2011Document40 pagesCEPS Activities Report 2010-2011kathamailNo ratings yet

- Belgian Consulting IndustryDocument18 pagesBelgian Consulting Industrystavros7No ratings yet

- Bankruptcy AccountingDocument13 pagesBankruptcy AccountingTarun SinghNo ratings yet

- Unit 5 International Monetary SystemDocument19 pagesUnit 5 International Monetary SystemerikericashNo ratings yet

- FX Options Hedging Strategies PDFDocument43 pagesFX Options Hedging Strategies PDFmarijana_jovanovikNo ratings yet

- New Ebook .How To Invest in Private Placement ProgramsDocument30 pagesNew Ebook .How To Invest in Private Placement ProgramsVicente Piqueras100% (2)

- Financial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassFrom EverandFinancial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassNo ratings yet