You might also like

- U04 Cost Accumulation SystemDocument30 pagesU04 Cost Accumulation SystemIslam AhmedNo ratings yet

- Journal EntriesDocument2 pagesJournal EntriesMelody Lim DayagNo ratings yet

- CFW Discussed Reflective EssayDocument6 pagesCFW Discussed Reflective EssayAila Grace Albero-Quirante MaribaoNo ratings yet

- Discontinued OperationsDocument4 pagesDiscontinued OperationsStacy SmithNo ratings yet

- Forgery Defenses; Bank LiabilitiesDocument24 pagesForgery Defenses; Bank LiabilitiesbrendamanganaanNo ratings yet

- Modified - What Do We Know About Capital Structure Ppt-Anindya, PijushDocument51 pagesModified - What Do We Know About Capital Structure Ppt-Anindya, PijushAnindya MitraNo ratings yet

- HW2Document6 pagesHW2LiamNo ratings yet

- Accounting For Partnerships: Basic Considerations and FormationDocument38 pagesAccounting For Partnerships: Basic Considerations and FormationRaihanah008100% (2)

- CH 9 - Completing The Cycle - MerchandisingDocument38 pagesCH 9 - Completing The Cycle - MerchandisingJem Bobiles100% (1)

- Given The Learning Materials and Activities of This Chapter, They Will Be Able ToDocument14 pagesGiven The Learning Materials and Activities of This Chapter, They Will Be Able Toedniel maratasNo ratings yet

- CFAS AssignmentDocument32 pagesCFAS AssignmentAlexander FloresNo ratings yet

- Preparation of Financial StatementsDocument3 pagesPreparation of Financial StatementsMarc Eric Redondo0% (1)

- Acc EqDocument5 pagesAcc EqBianca BgnNo ratings yet

- FULL DISCLOSURE Test BankDocument11 pagesFULL DISCLOSURE Test Bankzee abadillaNo ratings yet

- Chapter 2Document5 pagesChapter 2Sundaramani SaranNo ratings yet

- 5A Review of Accounting Process PDFDocument7 pages5A Review of Accounting Process PDFAldrin Jay SalcedoNo ratings yet

- Basic Accounting ReviewDocument75 pagesBasic Accounting ReviewSofie SergioNo ratings yet

- BASIC ACCOUNTING RECORDS AND TRANSACTIONSDocument30 pagesBASIC ACCOUNTING RECORDS AND TRANSACTIONSvaibhav bhavsarNo ratings yet

- Accounting adjustments and financial statementsDocument12 pagesAccounting adjustments and financial statementsKwaku DanielNo ratings yet

- Module 2Document8 pagesModule 2ysa tolosaNo ratings yet

- 03-IAS 8 Accounting Policies, Changes in Estimates and Correction of ErrorsDocument20 pages03-IAS 8 Accounting Policies, Changes in Estimates and Correction of Errorsrfhunxaie100% (2)

- Responsibility AccountingDocument3 pagesResponsibility AccountinglulughoshNo ratings yet

- PAS/PFRS Updates ReviewerDocument6 pagesPAS/PFRS Updates ReviewerPrincessAngelaDeLeonNo ratings yet

- Completing The Accounting CycleDocument64 pagesCompleting The Accounting CycleThelearningHights100% (1)

- Adjusting Entries QuizDocument2 pagesAdjusting Entries QuizOfelia YanosNo ratings yet

- St. Louis College of Bulanao: Purok 6, Bulanao, Tabuk City, Kalinga 3800Document9 pagesSt. Louis College of Bulanao: Purok 6, Bulanao, Tabuk City, Kalinga 3800Cath TacisNo ratings yet

- Accounting Perpetual & Periodic ComparisonDocument1 pageAccounting Perpetual & Periodic ComparisonAbbey LiNo ratings yet

- Conceptual Framework PPT 090719 PDFDocument53 pagesConceptual Framework PPT 090719 PDFSheena OroNo ratings yet

- Sales & Production BudgetsDocument14 pagesSales & Production BudgetsAnkur TripathyNo ratings yet

- Factors Affecting Currency Exchange RatesDocument2 pagesFactors Affecting Currency Exchange RatesEmmanuelle RojasNo ratings yet

- Chapter 2: Accounting Equation and The Double-Entry SystemDocument15 pagesChapter 2: Accounting Equation and The Double-Entry SystemSteffane Mae SasutilNo ratings yet

- CQCF - Qualitative CharacteristicsDocument4 pagesCQCF - Qualitative CharacteristicsEllen MaskariñoNo ratings yet

- Overview of Economic Development in 40 CharactersDocument22 pagesOverview of Economic Development in 40 CharactersAnna WilliamsNo ratings yet

- Accounting Concepts and PrinciplesDocument26 pagesAccounting Concepts and PrinciplesWindelyn Iligan100% (2)

- Lesson Plan in Fundamentals of Accounting EditedDocument6 pagesLesson Plan in Fundamentals of Accounting Editedjovelyn leeNo ratings yet

- AdjustmentDocument5 pagesAdjustmentBeta TesterNo ratings yet

- Accounting ConceptsDocument4 pagesAccounting ConceptsAjmal KhanNo ratings yet

- Finn 22 - Financial Management Questions For Chapter 2 QuestionsDocument4 pagesFinn 22 - Financial Management Questions For Chapter 2 QuestionsJoongNo ratings yet

- 04 Completing The Accounting Cycle PDFDocument39 pages04 Completing The Accounting Cycle PDFcyics TabNo ratings yet

- Course Syllabus-Strategic Cost MGTDocument7 pagesCourse Syllabus-Strategic Cost MGTJesel CatchoniteNo ratings yet

- Segmented Income Statements Using Variable CostingDocument34 pagesSegmented Income Statements Using Variable CostingalliahnahNo ratings yet

- Ia2 Prob 1-32 & 33Document1 pageIa2 Prob 1-32 & 33maryaniNo ratings yet

- Projected FinancialsDocument42 pagesProjected FinancialsAries Gonzales CaraganNo ratings yet

- Test of ControlsDocument3 pagesTest of ControlsMuzic HolicNo ratings yet

- Multiple ChoiceDocument14 pagesMultiple Choiceايهاب غزالة100% (2)

- ACC10 L1 01 Fundamentals of Accounting CgomezDocument6 pagesACC10 L1 01 Fundamentals of Accounting CgomezccgomezNo ratings yet

- Individual Income Tax Filing RequirementsDocument4 pagesIndividual Income Tax Filing RequirementsRoseanneNo ratings yet

- Basic Accounting EquationDocument4 pagesBasic Accounting EquationMuhammad AhmadNo ratings yet

- Audit Report: - Communicating Key Audit Matters in The Independent Auditor's ReportDocument30 pagesAudit Report: - Communicating Key Audit Matters in The Independent Auditor's Reportyea okayNo ratings yet

- Finman ReviewerDocument89 pagesFinman Reviewersharon5lotino100% (1)

- Topic 4 - Completing The Accounting CycleDocument52 pagesTopic 4 - Completing The Accounting CycleLA Syamsul100% (1)

- DYBSAAap313 - Auditing & Assurance Principles (PRELIM MODULE) PDFDocument10 pagesDYBSAAap313 - Auditing & Assurance Principles (PRELIM MODULE) PDFJonnafe Almendralejo IntanoNo ratings yet

- Introduction To Management, The Controller, and Cost AccountingDocument4 pagesIntroduction To Management, The Controller, and Cost Accountingdekambas100% (1)

- SHS Business Finance Chapter 3Document17 pagesSHS Business Finance Chapter 3Ji BaltazarNo ratings yet

- FABM1 Lesson8-1 Five Major Accounts-LIABILITIESDocument13 pagesFABM1 Lesson8-1 Five Major Accounts-LIABILITIESWalter MataNo ratings yet

- AIOU Financial Accounting ChecklistDocument9 pagesAIOU Financial Accounting ChecklistAhmad RazaNo ratings yet

- Accounting ReviewerDocument9 pagesAccounting ReviewerG Rosal, Denice Angela A.No ratings yet

- Financial InstrumentsDocument32 pagesFinancial InstrumentsSulochanaNo ratings yet

- 12 x10 Financial Statement AnalysisDocument19 pages12 x10 Financial Statement AnalysisGS DmpsNo ratings yet

- Cfas Pas 41 AgricultureDocument4 pagesCfas Pas 41 AgricultureMeg sharkNo ratings yet

- BUSINESS STRATEGY AND MERGER TYPESDocument5 pagesBUSINESS STRATEGY AND MERGER TYPESSteffany RoqueNo ratings yet

- Ratio AnalysisDocument4 pagesRatio AnalysisPrecious Vercaza Del Rosario100% (1)

- Review of Accounting ProcessDocument8 pagesReview of Accounting ProcessVenn Bacus RabadonNo ratings yet

- Share Based CompensationDocument5 pagesShare Based CompensationStacy Smith0% (1)

- EPS Calculation GuideDocument10 pagesEPS Calculation GuideStacy SmithNo ratings yet

- Inventories (PAS No. 2)Document14 pagesInventories (PAS No. 2)Da Eun LeeNo ratings yet

- Intangible AssetsDocument17 pagesIntangible AssetsJadeFerrerNo ratings yet

- IAS 1 Presentation of Financial Statements Revised KEY CHANGESDocument2 pagesIAS 1 Presentation of Financial Statements Revised KEY CHANGESStacy SmithNo ratings yet

- Debt Securities - BondsDocument6 pagesDebt Securities - BondsStacy SmithNo ratings yet

- InvestmentDocument8 pagesInvestmentStacy SmithNo ratings yet

- Introduction To Financial InstrumentsDocument2 pagesIntroduction To Financial InstrumentsStacy Smith100% (1)

- Customer Loyalty ProgrammesDocument3 pagesCustomer Loyalty ProgrammesStacy SmithNo ratings yet

- 101 Things To Do To Pass The CPA Board ExamsDocument4 pages101 Things To Do To Pass The CPA Board ExamsReden Balt ManaloNo ratings yet

- Correction of ErrorsDocument2 pagesCorrection of ErrorsStacy SmithNo ratings yet

- Conceptual FDocument1 pageConceptual FStacy SmithNo ratings yet

- Salient Differences Between IAS 39 and IFRS 9 Parameter IAS 39 Ifrs 9 NameDocument2 pagesSalient Differences Between IAS 39 and IFRS 9 Parameter IAS 39 Ifrs 9 NameStacy SmithNo ratings yet

- IfrsDocument1 pageIfrsStacy SmithNo ratings yet

- Salient Differences Between IAS 39 and IFRS 9 Parameter IAS 39 Ifrs 9 NameDocument1 pageSalient Differences Between IAS 39 and IFRS 9 Parameter IAS 39 Ifrs 9 NameStacy SmithNo ratings yet

- IfrsDocument1 pageIfrsStacy SmithNo ratings yet

- MANABIK Pension Scheme Provides Rs 1000 Monthly AidDocument8 pagesMANABIK Pension Scheme Provides Rs 1000 Monthly AidpriyamdawnNo ratings yet

- 9.2更新-2022 ACE实习信息汇总Document228 pages9.2更新-2022 ACE实习信息汇总Zack ZhangNo ratings yet

- Stock Market Valuation of Ubid and Creative ComputersDocument2 pagesStock Market Valuation of Ubid and Creative ComputersdikaNo ratings yet

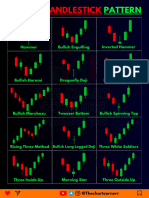

- Chart Pattern Cheat Sheet-1Document18 pagesChart Pattern Cheat Sheet-1YASHANK VISHWAKARMANo ratings yet

- True / False Questions: Foreign Exchange RiskDocument44 pagesTrue / False Questions: Foreign Exchange Risklatifa hnNo ratings yet

- Managerial Accounting Reviewer PreFinalsxDocument10 pagesManagerial Accounting Reviewer PreFinalsxGenelyn BalancarNo ratings yet

- Bank Strategic Planning and Budgeting ProcessDocument18 pagesBank Strategic Planning and Budgeting ProcessBaby KhorNo ratings yet

- International Valuation Standards - 2020 MCQDocument18 pagesInternational Valuation Standards - 2020 MCQNikhil Tidke100% (2)

- Comparing SBI Magnum and IDFC Mutual Fund RatiosDocument4 pagesComparing SBI Magnum and IDFC Mutual Fund RatiosJenifer Chrisla TNo ratings yet

- COMP255 Question Bank Chapter 7Document9 pagesCOMP255 Question Bank Chapter 7Ferdous RahmanNo ratings yet

- CH 03 Sample QsDocument6 pagesCH 03 Sample QsSourovNo ratings yet

- Law Project - The Negotiable Instrument Act - RevisedV1Document48 pagesLaw Project - The Negotiable Instrument Act - RevisedV1Teena Varma100% (3)

- AMD Form N-01b Buyer InfoDocument1 pageAMD Form N-01b Buyer InfoadobopinikpikanNo ratings yet

- CalPERS Annual Investment Report SummaryDocument296 pagesCalPERS Annual Investment Report SummaryChris WatkinsNo ratings yet

- "Corporate Strategy": by H I AnsoffDocument14 pages"Corporate Strategy": by H I AnsoffjashanNo ratings yet

- Iowa Committee On Political Education - AFL-CIO - 6060 - DR2 - SummaryDocument1 pageIowa Committee On Political Education - AFL-CIO - 6060 - DR2 - SummaryZach EdwardsNo ratings yet

- Auto - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDocument6 pagesAuto - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNo ratings yet

- Forex QuotationsDocument13 pagesForex QuotationsKamalSoniNo ratings yet

- By Otmar, B.A: Leasing PreparedDocument53 pagesBy Otmar, B.A: Leasing PreparedAnna Mwita100% (1)

- Interview QuestionsDocument42 pagesInterview Questionsbathula veerahanumanNo ratings yet

- Solution Manual For Accounting Information Systems 13th Edition Romney SteinbartDocument10 pagesSolution Manual For Accounting Information Systems 13th Edition Romney SteinbartErick Febrianto (Youtubers Cilik)No ratings yet

- INTRO TO UNLISTED SHARES: A PRIV MARKETDocument1 pageINTRO TO UNLISTED SHARES: A PRIV MARKETArvind KothariNo ratings yet

- Reimbursement Rate Update MemoDocument2 pagesReimbursement Rate Update MemoBrad AndersonNo ratings yet

- RedhatDocument216 pagesRedhatRobert Sunho LeeNo ratings yet

- What is Share Capital? Types and DefinitionsDocument1 pageWhat is Share Capital? Types and DefinitionsJuhaima BayaoNo ratings yet

- DOJ Opinion Denies UE Stock SaleDocument5 pagesDOJ Opinion Denies UE Stock Salea_vlaureNo ratings yet