You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- IRS Form 1040es 2016Document12 pagesIRS Form 1040es 2016Freeman Lawyer100% (1)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Form No. 16: Part ADocument7 pagesForm No. 16: Part AFuture ArtistNo ratings yet

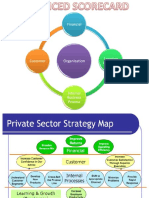

- Balanced Scorecard - Wells Fargo (BUSI0027D) PDFDocument12 pagesBalanced Scorecard - Wells Fargo (BUSI0027D) PDFRafaelKwong50% (4)

- Baher Isack Adem 2022 Tax ReturnDocument20 pagesBaher Isack Adem 2022 Tax Returnadammura043100% (1)

- CPA tax review questionsDocument10 pagesCPA tax review questionsRalph SantosNo ratings yet

- Gross IncomeDocument68 pagesGross IncomeNour Aira NaoNo ratings yet

- Chapter 13 Principles of DeductionDocument5 pagesChapter 13 Principles of DeductionJason Mables100% (1)

- SMChap 024Document35 pagesSMChap 024testbank67% (3)

- Quikchex CTC Calculator AprilDocument8 pagesQuikchex CTC Calculator Aprilravipati46No ratings yet

- Income Tax Act Basics: Section A Study Note 1Document62 pagesIncome Tax Act Basics: Section A Study Note 1amit kathait100% (1)

- Inventory Management of McDonald'sDocument2 pagesInventory Management of McDonald'sRafaelKwongNo ratings yet

- Percentage Taxes: Use BIR Form 2550MDocument17 pagesPercentage Taxes: Use BIR Form 2550Mcha11No ratings yet

- Filipino Estate Tax Calculation for Married IndividualDocument3 pagesFilipino Estate Tax Calculation for Married IndividualSharjaaah100% (2)

- Payslip 1Document1 pagePayslip 1bktsuna0201100% (2)

- MOS FY09 Financial Data PDFDocument9 pagesMOS FY09 Financial Data PDFRafaelKwongNo ratings yet

- Competitor AnalysisDocument4 pagesCompetitor AnalysisRafaelKwong100% (1)

- Case Study (Section 2.4)Document5 pagesCase Study (Section 2.4)RafaelKwongNo ratings yet

- Cost Control and AnalysisDocument2 pagesCost Control and AnalysisRafaelKwongNo ratings yet

- Management Accounting - Project 2Document3 pagesManagement Accounting - Project 2RafaelKwongNo ratings yet

- Ma - Capital Expenditure AnalysisDocument3 pagesMa - Capital Expenditure AnalysisRafaelKwongNo ratings yet

- Burger King-10K2009 PDFDocument128 pagesBurger King-10K2009 PDFRafaelKwongNo ratings yet

- Pizza Hutt 2009annualreportDocument220 pagesPizza Hutt 2009annualreportevojulzNo ratings yet

- Sales ForecastDocument2 pagesSales ForecastRafaelKwongNo ratings yet

- MADocument12 pagesMARafaelKwongNo ratings yet

- Management Accounting - Project 1Document7 pagesManagement Accounting - Project 1RafaelKwongNo ratings yet

- MA DisadvantageDocument1 pageMA DisadvantageRafaelKwongNo ratings yet

- MA Project 2 - McDonaldsDocument11 pagesMA Project 2 - McDonaldsRafaelKwongNo ratings yet

- Advantages of Balanced ScorecardDocument1 pageAdvantages of Balanced ScorecardRafaelKwongNo ratings yet

- McDonald's Advertising and Pricing IIDocument2 pagesMcDonald's Advertising and Pricing IIRafaelKwongNo ratings yet

- MA Presentation Slide Finalized - PPSXDocument33 pagesMA Presentation Slide Finalized - PPSXRafaelKwongNo ratings yet

- Cash BudgetDocument1 pageCash BudgetRafaelKwongNo ratings yet

- McDonald's Industry, Competitor and Marketing AnalysisDocument20 pagesMcDonald's Industry, Competitor and Marketing AnalysisRafaelKwongNo ratings yet

- IS PictureDocument1 pageIS PictureRafaelKwongNo ratings yet

- 1011 Group Project AssignmentDocument1 page1011 Group Project AssignmentRafaelKwongNo ratings yet

- Income Statement NeatDocument2 pagesIncome Statement NeatRafaelKwongNo ratings yet

- Management Accounting - Project 2Document3 pagesManagement Accounting - Project 2RafaelKwongNo ratings yet

- Chapter 16 LeadershipDocument18 pagesChapter 16 LeadershipRafaelKwongNo ratings yet

- Budgeted Balance SheetDocument2 pagesBudgeted Balance SheetRafaelKwongNo ratings yet

- Mini Interview Instruction SheetDocument2 pagesMini Interview Instruction SheetRafaelKwongNo ratings yet

- Taxation Q21 Handout v3 PDFDocument11 pagesTaxation Q21 Handout v3 PDFRafaelKwongNo ratings yet

- Answers For Question 2Document1 pageAnswers For Question 2RafaelKwongNo ratings yet

- Tax 302 Business and Transfer Tax Finals Answer.pdfDocument29 pagesTax 302 Business and Transfer Tax Finals Answer.pdfsunthatburns00No ratings yet

- BAM 208 - SAS - Day 8 - OUTDocument9 pagesBAM 208 - SAS - Day 8 - OUTAriane Grace Hiteroza MargajayNo ratings yet

- 2014 Taxation Law Bar Exam Questions and Suggested AnswersDocument30 pages2014 Taxation Law Bar Exam Questions and Suggested AnswersSyrine MallorcaNo ratings yet

- Payslip Feb 2022Document1 pagePayslip Feb 2022PRASHANT BANDAWARNo ratings yet

- Project Report On TaxationDocument51 pagesProject Report On TaxationsnehalNo ratings yet

- Monthly Digest Dec 2013Document134 pagesMonthly Digest Dec 2013innvolNo ratings yet

- MAY 21/NOV 21: Mock Test Solutions Upto Deduction From Gross Total IncomeDocument19 pagesMAY 21/NOV 21: Mock Test Solutions Upto Deduction From Gross Total IncomeUdaykiran BheemaganiNo ratings yet

- Chapter 12 (Income Tax On Corporations)Document10 pagesChapter 12 (Income Tax On Corporations)libraolrackNo ratings yet

- Short Notes On Important Central Labour Legislations: Juneja & AssociatesDocument36 pagesShort Notes On Important Central Labour Legislations: Juneja & AssociatesNaveen ChaudharyNo ratings yet

- Annualized Withholding TaxDocument22 pagesAnnualized Withholding Taxsai78No ratings yet

- Gross IncomeDocument54 pagesGross IncomeErneylou RanayNo ratings yet

- Petitioner Respondent: Lapanday Foods Corporation, - Commissioner of Internal RevenueDocument13 pagesPetitioner Respondent: Lapanday Foods Corporation, - Commissioner of Internal RevenueStephNo ratings yet

- Chapter 8 Governmental Accounting CPA FARDocument7 pagesChapter 8 Governmental Accounting CPA FARjklein2588No ratings yet

- LIC Development OfficerDocument12 pagesLIC Development OfficerVarun MalaniNo ratings yet

- Basic Concepts of ITDocument26 pagesBasic Concepts of ITAnishaAppuNo ratings yet

- Atlp Practice Questions Direct Tax & International TaxationDocument82 pagesAtlp Practice Questions Direct Tax & International Taxationharsh bangNo ratings yet

- Session 26 - Income TaxDocument23 pagesSession 26 - Income TaxUnnati RawatNo ratings yet

- Income Tax Software 2021-22 (AP) C Ramanjaneyulu 24-02-2022Document26 pagesIncome Tax Software 2021-22 (AP) C Ramanjaneyulu 24-02-2022boya maheswariNo ratings yet