Professional Documents

Culture Documents

Chap 3

Uploaded by

Brenda Banda0 ratings0% found this document useful (0 votes)

82 views33 pagesBankers and managers of other financial firms have evolved different organizational forms. The Financial-Services Industry has the greatest disparity in size of firms of virtually any industry. Banks and other financial firms are organized to carry out the roles assigned to them.

Original Description:

Original Title

chap3

Copyright

© © All Rights Reserved

Available Formats

PDF, TXT or read online from Scribd

Share this document

Did you find this document useful?

Is this content inappropriate?

Report this DocumentBankers and managers of other financial firms have evolved different organizational forms. The Financial-Services Industry has the greatest disparity in size of firms of virtually any industry. Banks and other financial firms are organized to carry out the roles assigned to them.

Copyright:

© All Rights Reserved

Available Formats

Download as PDF, TXT or read online from Scribd

0 ratings0% found this document useful (0 votes)

82 views33 pagesChap 3

Uploaded by

Brenda BandaBankers and managers of other financial firms have evolved different organizational forms. The Financial-Services Industry has the greatest disparity in size of firms of virtually any industry. Banks and other financial firms are organized to carry out the roles assigned to them.

Copyright:

© All Rights Reserved

Available Formats

Download as PDF, TXT or read online from Scribd

You are on page 1of 33

RoseHudgins: Bank

Management and Financial

Services, Seventh Edition

I. Introduction to the

Business of Banking and

FinancialServices

Management

3. The Organization and

Structure of Banking and

the FinancialServices

Industry

The McGrawHill

Companies, 2008

65

C H A P T E R T H R E E

The Organization and

Structure of Banking

and the Financial-Services

Industry

Key Topics in This Chapter

The Organization and Structure of the Commercial Banking Industry

Internal Organization of the Banking Firm: Community and Money-Center Banks

The Array of Organizational Structures in Banking: Unit, Branch, Holding Company and Electronic-Service

Providers

Interstate Banking and the Riegle-Neal Act

Two Alternative Types of Banking Organizations as the 21st Century Opened: The Financial Holding Company

and Bank Subsidiaries Model

Mergers and Acquisition

Banking Structure and Organization in Europe and Asia

The Changing Organization and Structure of Bankings Principal Competitors

Economies of Scale and Scope

31 Introduction

Chapter 1 of this text explored the many roles and services the modern bank and many of

its financial-service competitors offer. In that chapter we viewed banks and other financial

firms as providers of credit, channels for making payments, repositories of the publics sav-

ings, managers of business and household cash balances, trustees of customers property,

providers of risk protection, and brokers charged with carrying out purchases and sales of

securities and other assets to fulfill their customers wishes. Over the years, bankers and the

managers of other financial institutions have evolved different organizational forms to

perform these various roles and to supply the services their customers demand.

Truly, organizational form follows function, for banks and other financial firms usually

are organized to carry out the roles assigned to them by the marketplace as efficiently as

possible. Because larger institutions generally play a wider range of roles and offer more ser-

vices, size is also a significant factor in determining how financial firms are organized.

Indeed, the financial-services industry has the greatest disparity in size of firms of virtually

any industryfrom behemoths like J. P. Morgan Chase Bank, with offices all over the

RoseHudgins: Bank

Management and Financial

Services, Seventh Edition

I. Introduction to the

Business of Banking and

FinancialServices

Management

3. The Organization and

Structure of Banking and

the FinancialServices

Industry

The McGrawHill

Companies, 2008

world and close to a trillion dollars in assets to manage, to the Big Sky Bank of Gallatin

County, Montana, which, comparatively speaking, has relatively few assets to manage.

Thus, banking today reminds us a bit of the hardware industry with giant Wal-Mart at one

end of the size distribution and little Main Street Hardware at the other. Smaller firms

need a market niche where they can claim a service advantage or, eventually, they may be

driven from the industry.

However, a financial institutions role and size are not the only determinants of how it is

organized or of how well it performs. As we saw in Chapter 2, law and regulation, too, have

played a major role in shaping the performance and diversity of financial-service organiza-

tions around the globe. In this chapter we will see how changing public mobility and

changing demand for financial services, the rise of hundreds of potent competitors for the

financial-service customers business, and changing rules of the game have dramatically

changed the structure, size, and types of organizations dominating the financial-services

industry over time.

32 The Organization and Structure of the Commercial Banking Industry

Advancing Size and Concentration of Assets

In our exploration of the impact of organization and structure on the performance of banks

and their competitors we turn first to the leading financial-services industry, commercial

bankingthe dominant supplier of credit to businesses and the leading provider of deposits

accessible by check and debit card in the global financial system.

The structure of the American banking industry is somewhat unique compared to most

of the rest of the world. Most commercial banks in the United States are small by global

standards. For example, as Exhibit 31 shows, almost half of all U.S. insured banking

organizationsapproximately 3,600 commercial banksheld total assets of less than $100

million each in 2005. However, these smallest financial institutions, numerous as they are,

held only about 2 percent of total industry assets.

In contrast, the American banking industry also contains some of the largest financial-

service organizations on the planet. For example, Citigroup and J. P. Morgan Chase, both

based in New York City, and the Bank of America, based in Charlotte, North Carolina,

hold sufficient assetsapproximately a trillion dollars eachto rank these financial-

service providers among the very largest businesses in the world.

Moreover, banking continues to be increasingly concentrated not in the smallest or

mid-size range, but in the very largest of all financial firms. For example, the 10 largest

American banks now control close to half of all industry assets, while the 100 largest U.S.

banking organizations hold more than three-quarters of industrywide assets and their mar-

ket share has risen year after year. Today a quarter of all domestic deposits are controlled

by only three U.S. banking companies. In contrast, as Exhibit 32 illustrates, both small

and medium-size banks have lost substantial market share to the biggest banks holding

more than $25 billion in assets apiece.

Interestingly enough, not only industry assets but also profits tend to be concentrated

in the largest financial firms. For example, most American banks that lost money at the

opening of the 21st century were among the smallest banking organizations, holding less

than 1 percent of industry assets.

Although banking globally has become more concentrated in the largest institutions,

the concentration of bank assets and deposits at the local levelin the towns and cities

where most people workseems to have changed in a fairly limited way in recent years.

There appear to have been relatively small changes in the average number of banks and in

the percentage of assets under bank control in most cities and rural areas across America.

66 Part One Introduction to the Business of Banking and Financial-Services Management

Factoid

What is the largest

banking company in

the United States and

the fifth largest in

the world (measured

by total assets)?

Answer: Citigroup,

Inc., based in New York

City.

RoseHudgins: Bank

Management and Financial

Services, Seventh Edition

I. Introduction to the

Business of Banking and

FinancialServices

Management

3. The Organization and

Structure of Banking and

the FinancialServices

Industry

The McGrawHill

Companies, 2008

In part, this moderate change in banking structure in many local towns and cities

reflects the rise of local competition as more financial firms reach into local communi-

ties, sometimes from great distances away, using the rapidly exploding technology of

information.

Is a Countertrend Now under Way?

However, before we get too set in our views about whats happening to the structure of bank-

ing in the United States and around the world, we need to recognize that a new trend may

Chapter 3 The Organization and Structure of Banking and the Financial-Services Industry 67

$7,439 billion in assets held

by the largest banks (86.6%)

$963 billion in assets held

by medium-size banks (11.2%)

Assets Held by U.S. FDIC-insured Commercial Banks

(Total Industry Assets of $8,589 Billion in 2005)

Number of U.S. FDIC-insured Banks

(Total of 7,598 Banks Operating in 2005)

$188 billion in assets held

by smallest banks (2.2%)

445 largest banks (5.9%)

3,536 medium-size banks

(46.5%)

3,617 smallest banks (47.6%)

Smallest FDIC-insured banks with total assets

of up to $100 million each

Medium-size FDIC-insured banks with total assets

of more than $100 million up to $1 billion

Largest FDIC-insured banks with total assets

of $1 billion or more

EXHIBIT 31

The Structure of the

U.S. Commercial

Banking Industry,

March 31, 2005

Source: Federal Deposit

Insurance Corporation.

Key URL

If you are interested in

tracking changes over

time in the structure

and organization of the

U.S. banking industry,

see especially

www.fdic.gov/

individual/index.html.

RoseHudgins: Bank

Management and Financial

Services, Seventh Edition

I. Introduction to the

Business of Banking and

FinancialServices

Management

3. The Organization and

Structure of Banking and

the FinancialServices

Industry

The McGrawHill

Companies, 2008

68 Part One Introduction to the Business of Banking and Financial-Services Management

80

Market share (percent)

Small Banks Lose Market Share to Large Banks

Small Medium Large

70

60

50

40

30

20

10

0

84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05

EXHIBIT 32 Small and Medium-Size U.S. Banks Lose Market Share to the Largest Banking Institutions

Sources: Data: Call Report, FFIEC; Consumer Price Index for All Urban Consumers, Bureau of Labor Statistics. Graphical presentation: Jeffrey W. Gunther and Robert R.

Moore. Small Banks Competitors Loom Large, Southwest Economy, Federal Reserve Bank of Dallas, January/February 2004, p. 9.

Notes: Small banks belong to organizations with less than $1 billion in commercial bank assets, medium-sized banks to those with $1 billion to $25 billion in bank assets, and

large banks to those with more than $25 billion. Assets are measured in 2002 dollars. All data are year-end except 2005 data, which are as of June 30. The market share for

each size group is that groups proportion of total bank assets.

be emerging. True, smaller banks continue to disappear and the biggest banks are gobbling

up greater industry shares each year. But there are signs that this pattern of change may be

slowing down. Indeed, as FDIC economists Jones and Critchfield [14] suggest in a new study,

the long decline in the number of banking organizations may be nearing an end. Ultimately,

they suggest, the number of banking organizations inside the United States may stabilize in

perhaps 5 to 10 years.

Already the number of bank mergers has slowed substantially in the new century as the

remaining desirable targets for acquisition have fallen off. The industry may be approach-

ing a point where the number of mergers is approximately offset each year by the number

of newly chartered banking firms. That is, those leaving the industry may be roughly coun-

terbalanced by new start-ups. This suggests that, once industry stability is reached, there

may still be thousands of small banks in operation along with a handful of money-center,

globally reaching banks.

33 Internal Organization of the Banking Firm

Whether or not the above projections for the future of banking actually happen, the great

differences in size across the industry that have appeared in recent years have led to

marked differences in the way banks are organized internally and in the types and variety

of financial services each bank sells in the markets it chooses to serve.

Community Banks and Other Community-Oriented Financial Firms

The influence of size upon internal organization can be seen most directly by looking

at the typical organization chart supplied by the management of a small community

bank with about $250 million in assets and located in a smaller city in the Midwest.

(See Exhibit 33.) Like hundreds of financial firms serving smaller cities and towns,

RoseHudgins: Bank

Management and Financial

Services, Seventh Edition

I. Introduction to the

Business of Banking and

FinancialServices

Management

3. The Organization and

Structure of Banking and

the FinancialServices

Industry

The McGrawHill

Companies, 2008

this bank is heavily committed to attracting smaller household deposits and to making

household and small business loans.

A bank like this, devoted principally to the markets for smaller, locally based deposits and

loans, is also often referred to as a retail bank. Financial firms of this type stand in sharp con-

trast to wholesale banks, like J. P. Morgan Chase and Citibank of New York, which concentrate

mainly on serving commercial customers and making large corporate loans all over the globe.

The service operations of a community bank are usually monitored by a cashier and

auditor working in the accounting department and by the vice presidents heading up the

banks loan, fund-raising, marketing, and trust departments. These officers report to the

senior executives of the firm, consisting of the board chairman, the president (who usually

runs the bank from day to day), and the senior vice president (who is usually responsible

for long-range planning and for assisting heads of the various departments in solving their

most pressing problems). Senior management, in turn, reports periodically to members of

the board of directorsthe committee selected by the stockholders (owners) to set pol-

icy and monitor performance.

The organization chart in Exhibit 33 is not complicated. Close contact between top

management and the management and staff of each division is common. If smaller com-

munity banks have serious problems, they usually center on trying to find competent new

managers to replace aging administrators and struggling to afford the cost of new equip-

ment and keep pace with new regulations. Also, community banks are usually significantly

impacted by changes in the health of the local economy. For example, many are closely

tied to agriculture or to the condition of other locally based businesses, so when local sales

are depressed, the bank itself often experiences slowed growth and its earnings may fall.

Community banks often present limited opportunities for advancement or for the

development of new banking skills. Nevertheless, banks of this size and geographic loca-

tion may represent attractive employment opportunities because they place the banker

close to his or her customers and give bank employees the opportunity to see how their

actions can have a real impact on the quality of life in local cities and towns. Unlike some

larger institutions, community bankers usually know their customers well and are good at

monitoring the ever-changing fortunes of households and small businesses.

Despite these favorable features of community banking, these institutions have been

losing ground, both in numbers of institutions and in industry shares. For example, their

Chapter 3 The Organization and Structure of Banking and the Financial-Services Industry 69

Key URL

For further information

about community banks

and their management,

see Americas

Community Bankers at

www.acbankers.org.

Operations

(check clearing,

posting, account

verification, and

customer complaints)

Accounting and

Operations Division

Fund-Raising and

Marketing Division

Tellers

New Accounts

Advertising

and Planning

Accounting and

Audit Department

Business

Trusts

Personal

Trusts

Trust

Division

Commercial

Loan Officers

Consumer Loan

Officers

Lending Division

Chief Administrative Officers (including the

Board Chairman and President or CEO)

EXHIBIT 33

Organization Chart

for a Smaller

Community Bank

RoseHudgins: Bank

Management and Financial

Services, Seventh Edition

I. Introduction to the

Business of Banking and

FinancialServices

Management

3. The Organization and

Structure of Banking and

the FinancialServices

Industry

The McGrawHill

Companies, 2008

numbers (including commercial banks and thrift institutions combined) have fallen

from close to 14,000 community banks in 1985 to just over 7,000 in 2005. Over the

same time span their share of industry assets has dropped from about 26 percent to little

more than 12 percent. In contrast, the industry share claimed by the 25 largest money-

center banks in the United States rose from about 28 percent in 1985 to more than

60 percent in 2005.

Larger BanksMoney Center, Wholesale and Retail

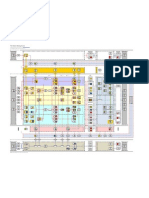

In comparison to smaller community banks, the organization chart of a large (multibil-

lion dollar) money center banklocated in a large city and wholesale or wholesale plus

retail in its focustypically looks far more complex than that of a smaller, community-

oriented bank. A fairly typical organization chart from an eastern U.S. money-center

bank with more than $25 billion in assets is shown in Exhibit 34. This bank is owned

and controlled by a holding company whose stockholders elect a board of directors to

oversee the bank and nonbank businesses allied with the same holding company.

Selected members of the holding companys board of directors serve on the banks

board as well. The key problem in such an organization is often the span of control. Top

management may be knowledgeable about banking practices but less well informed

about the products and services offered by subsidiary companies. Moreover, because the

bank itself offers so many different services in both domestic and foreign markets, seri-

ous problems may not surface for weeks or months. In recent years a number of the

largest banks have moved toward the profit-center approach, in which each major

department strives to maximize its contribution to profitability and closely monitors its

own performance.

70 Part One Introduction to the Business of Banking and Financial-Services Management

Key URL

If you would like to find

out how the structure of

banking is changing in

your home town, see,

for example, www2.

fdic.gov/idasp/main.asp.

Factoid

If you want to know

how a particular bank is

organized internally, try

typing its name into

your Web browser,

which often calls up

information on what

departments the bank

operates, what services

it offers, and where its

facilities are located.

International

Banking

Department

Global Finance

Foreign Offices Group

Administrative Services Group: Senior Executive Committee

Board Chairman, President or CEO, and Senior Vice Presidents

Commercial Credit

Funds-Allocation

Division

Commercial Financial

Services Group

Credit Cards

Commercial Real

Estate

Corporate Services

Loan Workout

Group

Loan Review

Group

Investments and

Funding Group

Portfolio Management

and Money-Market

Desk

Fund Raising and

Funds Management

Division

Capital Markets

Department

Asset/Liability

Management

Planning

Institutional

Banking Department

Operations Department

Auditing and Control Department

Branch Office Management

Computer Systems

Human Resources

Teller Department

Securities Department

Regulatory Compliance Group

Personal Financial

Services Division

Trust Services

Customer Services

Private Banking

Services

Residential Lending

Safe Deposit

Department

Motor, ATM, and

Internet Banking

Lobby Services

Group

Marketing

EXHIBIT 34 Organization Chart for a Money Center or Wholesale Bank Serving Domestic and International Markets

RoseHudgins: Bank

Management and Financial

Services, Seventh Edition

I. Introduction to the

Business of Banking and

FinancialServices

Management

3. The Organization and

Structure of Banking and

the FinancialServices

Industry

The McGrawHill

Companies, 2008

The largest money-center banks possess some advantages over smaller, community-ori-

ented institutions. Because the largest institutions serve many different markets with many

different services, they are better diversifiedboth geographically and by product line

to withstand the risks of a fluctuating economy. These institutions are rarely dependent on

the economic fortunes of a single industry or, in many cases, even a single nation. For

example, such banking companies as Citigroup, J. P. Morgan Chase, and Deutschebank

often receive half or more of their earnings from sources outside their home country. They

also possess the important advantage of being able to raise huge amounts of financial cap-

ital at relatively low cost. As interstate banking spreads across the United States and

global banking expands throughout Asia, Europe, and the Middle East, these banks should

be well positioned because of their greater capacity to accept the risks of entering new

markets and their potentially greater access to capital and managerial talent.

Trends in Organization

The tendency in recent years has been for most financial institutions to become more com-

plex organizations over time. When a financial firm begins to grow, it usually adds new ser-

vices and new facilities. With them come new departments and new divisions to help

management more effectively focus and control the firms resources.

Another significant factor influencing banking organizations today is the changing

makeup of the skills bankers need to function effectively. For example, with the global

spread of government deregulation and the resultant increase in the number of competitors

in major markets, more and more financial firms have become market driven and sales ori-

ented, more alert to the changing demands of their customers and also to the challenges

competitors pose.

These newer activities require the appointment of management and staff who can devote

more time to surveying customer service needs, developing new services, and modifying old

service offerings to reflect changing customer needs. Similarly, as the technology of financial

services production and delivery has shifted more toward computer-based systems and the

Internet, financial firms have needed growing numbers of people with computer skills and

the electronic equipment they work with. At the same time, automated book-keeping has

reduced the time managers spend in routine operations, thus allowing greater opportunity for

planning new services and thinking creatively about how to better serve customers.

Chapter 3 The Organization and Structure of Banking and the Financial-Services Industry 71

Concept Check

31. How would you describe the size distribution of

American banks and the concentration of industry

assets inside the United States? What is happening

in general to the size distribution and concentration

of banks in the United States and in other industrial-

ized nations and why?

32. Describe the typical organization of a smaller

community bank and a larger money-center bank.

What does each major division or administrative

unit within the organization do?

33. What trends are affecting the way banks and their

competitors are organized today?

Key URL

Retail-oriented banks

are represented in the

industry by the

Consumer Bankers

Association at

www.cbanet.org.

34 The Array of Organizational Structures and Types in the Banking Industry

There are so many different types of banks and other depository institutions in the finan-

cial system today that the distinctions between these different types of organizations often

get very confusing. For example, as Exhibit 35 points out, most depository institutions are

labeled insured because the great majority of American depositories have chosen to

RoseHudgins: Bank

Management and Financial

Services, Seventh Edition

I. Introduction to the

Business of Banking and

FinancialServices

Management

3. The Organization and

Structure of Banking and

the FinancialServices

Industry

The McGrawHill

Companies, 2008

apply for and receive federal insurance, mostly provided by the FDIC, to back their

deposits and reassure the public.

Moreover, as Exhibit 35 also indicates, a majority of banks and other depositories in

the United States are classified as state chartered because the financial-services com-

mission of a particular state has issued them a charter of incorporation. The remaining

institutions in the banking sector are labeled national banks because their charter has

been issued by a federal government agency, the Comptroller of the Currency. Similarly,

so-called member banks belong to the Federal Reserve System in the United States,

although most American banks are not members of the Fed. State-chartered, nonmember

banks are more numerous, but national and member banks tend to be larger and hold most

of the publics deposits.

Are these the only ways we can classify modern depository institutions? Hardly! We can

also classify them by their corporate or organizational structure. Their assets may be under the

control of a single corporation or they may be structured as multiple corporations linked to

each other through a common group of stockholders. They may sell all of their services

through a single office or offer those services through multiple facilities scattered all over the

region and around the globe. They may reach the public exclusively online, using computers

and the telephone, or set up scores of neighborhood branch offices (stores) to offer their

customers a physical presence near their homes or offices. Lets look closely at the different

types of organizational structures that have dominated the banking industry over the years.

72 Part One Introduction to the Business of Banking and Financial-Services Management

0%

1,864 FDIC-insured banks with national

(federal) charters (25%)

50% 100%

5,734 FDIC-insured banks with state charters

(75%)

7,598 banks with FDIC deposit insurance

coverage (98% of all U.S. commercial banks)

Est. 160 banks without FDIC insurance (2%)

2,771 FDIC-insured banks with membership

in the Federal Reserve System (36%)

4,827 FDIC-insured banks that were not

members of the Federal Reserve System (64%)

Percentage of all FDIC-insured bank deposits

held by state banks (45%)

*

Percent of all FDIC-Insured Banks

Percentage of all FDIC-insured bank deposits

held by national banks (55%)

*

Percentage held by member banks of the Federal

Reserve System of all FDIC-insured bank

deposits (77%)

Percentage of all FDIC-insured bank deposits

held by banks not members of the Federal Reserve

System (23%)

EXHIBIT 35

U.S. Commercial

Banks with Federal

versus State Charters,

Membership in the

Federal Reserve

System, and Deposit

Insurance from the

Federal Government

(as of March 31,

2005)

Source: Board of Governors of

the Federal Reserve System and

the Federal Deposit Insurance

Corporation.

Note: Figures are for June 2004.

RoseHudgins: Bank

Management and Financial

Services, Seventh Edition

I. Introduction to the

Business of Banking and

FinancialServices

Management

3. The Organization and

Structure of Banking and

the FinancialServices

Industry

The McGrawHill

Companies, 2008

Unit Banking Organizations

Unit banks, one of the oldest kinds, offer all of their services from one office, although some

services (such as taking deposits, cashing checks, or paying bills) may be offered from lim-

ited-service facilities, such as drive-up windows and automated teller machines (ATMs)

that are linked to the banks computer system. These organizations are still common in

U.S. banking today. For example, in 2004 just over 2,100 of the nations commercial

banks, about one-third, operated just one full-service office, compared to about 5,500

banks that had two or more full-service offices in operation.

One reason for the comparatively large number of unit banks is the rapid formation of

new banks, even in an age of electronic banking and megamergers among industry lead-

ers. About 15 percent of all community banks are less than 10 years old. Many customers

still seem to prefer small banks, which get to know their customers well. Between 1980

and 2005, about 4,800 new banks were chartered in the United States, or an average of

almost 200 per yearsubstantially more than the number of failing banks in most years,

as Table 31 relates.

Most new banks start out as unit organizations, in part because their capital, manage-

ment, and staff are severely limited until the bank can grow and attract additional

resources and professional staff. However, most banks desire to create multiple service

facilitiesbranch offices, electronic networks, Web sites, and other service outletsto

open up new markets and to diversify geographically in order to lower their overall risk

Chapter 3 The Organization and Structure of Banking and the Financial-Services Industry 73

Entry into the Industry Exit from the Industry

Newly Failures of Number of Unassisted

Chartered FDIC-Insured Mergers and

Bank Branches

Year Banks Banks Acquisitions Opened Closed

1980 205 10 126 2,397 287

1981 198 7 210 2,326 364

1982 317 32 256 1,666 443

1983 361 45 314 1,320 567

1984 391 78 330 1,405 889

1985 331 116 336 1,480 617

1986 257 141 341 1,387 763

1987 219 186 543 1,117 960

1988 229 209 598 1,676 1,082

1989 192 206 411 1,825 758

1990 165 158 393 2,987 926

1991 106 105 447 2,788 1,456

1992 72 98 428 1,677 1,313

1993 61 62 481 1,499 1,215

1994 50 11 548 2,461 1,146

1995 102 6 609 2,367 1,319

1996 145 5 554 2,487 1,870

1997 188 1 601 NA NA

1998 194 3 564 1,436 NA

1999 232 6 422 1,450 1,158

2000 192 6 456 1,286 NA

2001 129 3 360 1,010 NA

2002 91 10 217 1,285 1,137

2003 116 3 149 1,465 649

2004 126 3 236 2,078 666

2005 179 0 315 NA NA

TABLE 31

Entry and Exit in

U.S. Banking

Source: Board of Governors of

the Federal Reserve System and

the Federal Deposit Insurance

Corporation.

Key URL

One of the more

interesting bankers

associations is the NBA

or National Bankers

Associationa trade

group that serves to

protect the interests of

minority-owned banks,

including those owned

by African Americans,

Native Americans,

Hispanic Americans,

and women. See

especially

www.nationalbankers.

org for a fuller

description.

RoseHudgins: Bank

Management and Financial

Services, Seventh Edition

I. Introduction to the

Business of Banking and

FinancialServices

Management

3. The Organization and

Structure of Banking and

the FinancialServices

Industry

The McGrawHill

Companies, 2008

exposure. Bankers know that relying on a single location from which to receive customers

and income can be risky if the surrounding economy weakens and people and businesses

move away to other market areas.

74 Part One Introduction to the Business of Banking and Financial-Services Management

Concept Check

34. What are unit banks? 35. What advantages might a unit bank have over

banks of other organizational types? What disad-

vantages?

Branch Banking Organizations

As a unit bank grows larger in size it usually decides at some point to establish a branch

banking organization, particularly if it serves a rapidly growing region and finds itself

under pressure either to follow its business and household customers as they move into

new locations or lose them to more conveniently located financial-service competitors.

Branch banking organizations offer the full range of banking services from several loca-

tions, including a head office and one or more full-service branch offices. Such an orga-

nization is also likely to offer limited services through a supporting network of drive-in

windows, ATMs, computers electronically linked to the banks computers, point-of-sale

terminals in stores and shopping centers, the Internet, and other advanced communi-

cations systems.

Senior management of a branch banking organization is usually located at the home

office, though each full-service branch has its own management team with limited author-

ity to make decisions on customer loan applications and other facets of daily operations. For

example, a branch manager may be authorized to approve a customer loan of up to

$100,000. Larger loan requests, however, must be referred to the home office for a final deci-

sion. Thus, some services and functions in a branch banking organization are highly cen-

tralized, whereas others are decentralized at the individual service facility level. Exhibit 36

displays a typical branch banking organization.

Banking Corporation Chartered by State or Federal Governments

Home

or Head

Office

Full-Service

Branch

Offices

Full-Service

Branch

Offices

Automated

Teller Machines

and/or

Point-of-Sale

Terminals

in Stores and

Shopping Centers

Drive-up

Window

or

Pedestrian

Walk-up

Window

Facilities

Electronic

Communications

Networks

(including

telephones,

home and

office computers,

the Internet, etc.)

EXHIBIT 36

The Branch Banking

Organization

RoseHudgins: Bank

Management and Financial

Services, Seventh Edition

I. Introduction to the

Business of Banking and

FinancialServices

Management

3. The Organization and

Structure of Banking and

the FinancialServices

Industry

The McGrawHill

Companies, 2008

Branchings Expansion

Most branch banks in the United States are small compared to other banks around the

globe. For example, as the 21st century opened there were about 5,500 branch banking

organizations in the United States, operating close to 70,000 full-service branch office facil-

ities. As Table 31 reminds us, while the number of U.S. banks declined over this last half-

century from around 14,000 to about 7,500 today, the number of branch offices has soared

from only about 3,000 to about 70,000 full-service offices, not counting more than 300,000

computer-terminal banking facilities scattered across the United States in thousands of

stores, shopping centers, and lobbies, and at more than 3,000 service-providing Internet sites.

During the Great Depression of the 1930s, only one in five American banks, on aver-

age, operated a full-service branch office. By the beginning of the 21st century the average

U.S. bank operated about ten full-service branch offices, although some of the nations

leading banks, like Bank America and J. P. Morgan Chase, operate hundreds of branch

offices today. By and large, these limited numbers of U.S. branches per bank are small

potatoes compared to banks in Canada, Great Britain, and Western Europe that often

operate hundreds or thousands of branch outlets in addition to their computer terminal

and Internet customer connections.

This wide disparity in national banking structures arises from differences in public atti-

tudes toward branch banking. Early in the history of the United States, there was great fear

of the power of branch banks to eliminate competition and charge their customers exces-

sive prices for services. As a result, most states passed laws to limit branching activity.

Unfortunately, this antibranching attitude may have allowed some banks, freed from the

danger of outside entry by other banking organizations, to act as monopolies, raising prices

and restricting output. Today, however, all 50 states and the District of Columbia permit

some form of branch facilities.

Reasons behind Branchings Growth

The causes of the rapid growth in branch banking are many. One factor has been the exo-

dus of population over the past several decades from cities to suburban communities, forc-

ing many large downtown banks to either follow or lose their mobile customers. The

result has been the expansion of branch offices and automated tellers, radiating out from

downtown areas of major cities like the spokes of a wheel, with leading money-center

banks at the hub of the branching wheel. Bank failures have also spawned branching

activity as healthier banks have been allowed to take over sick ones and convert them

into branch offices. Business growth, too, has fueled the spread of branch banking; the

credit needs of rapidly growing corporations necessitate larger and more diversified banks

that can reach into many local markets for small deposits and pool those funds into large-

volume loans. Table 32 demonstrates how the concentration of U.S. banking facilities

has shifted from main offices to branch offices over the past half century.

The passage of the Riegle-Neal Interstate Banking and Branching Efficiency Act in

1994 provided the basis for an expansion of new bank branch offices nationwide (i.e.,

interstate banking). However, in recent years new bank branch office expansion appears

to have slowed somewhat and no single bank has yet established full-service branch offices

in all 50 states. One reason is a recent rise in full-service office closings as the burgeoning

cost of brick-and-mortar buildings has soared and some neighborhoods have declined and

become less attractive to bankers. Then, too, the Internet and other electronic access

media have taken over many routine financial transactions and there may be less need for

extensive full-service branch offices. Finally, as we saw in Chapter 2, U.S. legislation in

1994 that allows branching anywhere in the country now permits bankers to buy existing

branch networks in the most desirable communities, no matter where they are located,

rather than always having to build new offices.

Chapter 3 The Organization and Structure of Banking and the Financial-Services Industry 75

Key URL

Mergers and

acquisitions have had a

powerful impact upon

the growth of branch

offices and the trend

toward much larger

banking organizations

in the United States

and around the world.

To get a picture of

recent mergers and

acquisitions in this

field, see www.snl.com.

Key URL

You can learn more

about bank failures and

their causes by

following such Web

sites as

www.fdic.gov/bank/

historical/history/

index.html.

RoseHudgins: Bank

Management and Financial

Services, Seventh Edition

I. Introduction to the

Business of Banking and

FinancialServices

Management

3. The Organization and

Structure of Banking and

the FinancialServices

Industry

The McGrawHill

Companies, 2008

Advantages and Disadvantages of Branch Banking

Branch banking organizations often buy out smaller banks, converting them into

branches and concentrating the industrys assets into the hands of fewer firms. How-

ever, there is little or no evidence that this necessarily lessens competition. Customer

convenience seems to improve because more services are available at every branch

location and branching areas tend to have more offices per unit of population, reduc-

ing transactions costs for the average customer. However, some service fees seem to be

higher in branching areas, especially when branch banks acquire smaller institutions

and boost service charges after these acquisitions are made. However, the higher service

fees may reflect greater knowledge on the part of larger banks concerning the true cost

of each service.

Branch banks appear to be less prone to failure than banks without full-service branch

offices. For example, Canadawhere the typical bank operates hundreds of branches

experienced not a single bank failure during the Great Depression of the 1930s, whereas the

United Statesa nation of many small, frequently branchless banksexperienced thou-

sands of failures.

76 Part One Introduction to the Business of Banking and Financial-Services Management

Concept Check

36. What is a branch banking organization?

37. What trend in branch banking has been prominent

in the United States in recent years?

38. Do branch banks seem to perform differently than

unit banks? In what ways? Can you explain any dif-

ferences?

Electronic BranchingWeb Sites and Electronic Networks: An Alternative

or a Supplement to Traditional Bank Branch Offices?

As we saw in the preceding section, traditional brick-and-mortar bank branch offices con-

tinue to expand across the United States and in many other countries as well. Growing

somewhat faster today, however, are what some experts call electronic branches. These

Average Number

Number of Bank Number of Branch Total of All of Branches per

Year Home (Main) Offices Offices U.S. Bank Offices U.S. Bank

1934 14,146 2,985 17,131 0.21

1940 13,442 3,489 16,931 0.26

1952 13,439 5,486 18,925 0.41

1964 13,493 14,703 28,196 1.09

1970 13,511 21,810 35,321 1.61

1982* 14,451 39,784 54,235 2.75

1988 13,137 46,619 59,756 3.55

1993 10,960 52,868 63,828 4.82

1999 8,551 63,684 72,265 7.45

2001 8,096 64,938 73,034 8.02

2002 7,887 66,185 74,072 8.39

2003 7,769 67,390 75,159 9.67

2004 7,630 69,975 77,605 10.17

TABLE 32

Growth of

Commercial Bank

Branch Offices in the

United States

Source: Federal Deposit

Insurance Corporation.

*Beginning in 1982 remote service facilities (ATMs) were not included in the count of total branches. At year-end 1981, there were

approximately 3,000 remote service banking facilities.

RoseHudgins: Bank

Management and Financial

Services, Seventh Edition

I. Introduction to the

Business of Banking and

FinancialServices

Management

3. The Organization and

Structure of Banking and

the FinancialServices

Industry

The McGrawHill

Companies, 2008

include Web sites offering Internet banking services, automated teller machines (ATMs)

and ATM networks dispensing cash and accepting deposits, point-of-sale (POS) terminals

in stores and shopping centers to facilitate payment for goods and services, and personal

computers and telephone systems connecting the customer to his or her bank.

1

(See

Exhibit 37.) Through many of these computer- and telephone-based delivery systems cus-

tomers can check account balances, set up new accounts, move money between accounts,

pay bills, request loans, and invest spare funds any hour of the day or night. Moreover, if

you happen to be the holder of an electronic account, you do not necessarily have to

change financial-service institutions when you move.

Chapter 3 The Organization and Structure of Banking and the Financial-Services Industry 77

EXHIBIT 37 Electronic Banking Systems, Computer Networks, and Web Banking: An Effective Alternative

to Full-Service Branches?

Brick and

Mortar Full-

Service Branch

Offices Belonging

to Bank B

Brick and

Mortar Full-

Service Branch

Offices Belonging

to Bank C

Web site

for Bank C

Web site

for Bank B

Central Processing

Unit (Performing

account verification

services)

Network Switching

Equipment Center

(Sending transactions

to the correct

depository institution)

Automated Teller

Machines (ATMs)

in Stores, Shopping

Centers, Schools,

and Other Public

Facilities

Point of Sale Terminals

to Facilitate Payments

for Purchases of Goods

and Services in Stores,

Gas Stations, and Other

Locations

Web site

for Bank A

Computer for Bank

A(Accounts of

businesses and house-

holds credited or

debited based on their

transactions)

Brick and

Mortar Full-

Service Branch

Offices Belonging

to Bank A

Computer for Bank

B (Accounts of

businesses and house-

holds credited or

debited based on their

transactions)

Computer for Bank

C (Accounts of

businesses and house-

holds credited or

debited based on their

transactions)

1

The installation and use of these forms of electronic branches are discussed more fully in Chapter 4.

RoseHudgins: Bank

Management and Financial

Services, Seventh Edition

I. Introduction to the

Business of Banking and

FinancialServices

Management

3. The Organization and

Structure of Banking and

the FinancialServices

Industry

The McGrawHill

Companies, 2008

Most electronic branches seem to operate at far lower cost than do conventional brick-

and-mortar branch offices, at least for routine transactions. For example, a deposit made

through the Internet may be at least 10 times cheaper to execute than the same deposit

made through a nearby ATM.

Many banksespecially virtual banks that provide their services exclusively through

the Webare moving today to pass these Web-generated cost savings along to their cus-

tomers and gain a market advantage over depository institutions still relying heavily on

neighborhood brick-and-mortar branch offices. However, despite significantly lower trans-

actions costs, virtual banking firms have not yet demonstrated they can be consistently

profitable. Part of the reason may be their tendency to advertise much lower customer fees

than do many brick-and-mortar-oriented deposit institutions. Moreover, virtual banks

have to combat the fact that customers often feel more secure if they know that their

depository institution, besides being Web accessible, also has full-service branches where

they can go to straighten out serious problems. However, this picture seems to be chang-

ing as millions of new Internet-connected customers continue to switch from older ser-

vice-access channels toward instantly available online services.

Bank Holding Company Organizations

In earlier decades when governments prohibited or severely restricted branch banking,

the holding company often became the most attractive organizational alternative inside

the United States and in several other countries as well. A bank holding company is sim-

ply a corporation chartered for the purpose of holding the stock (equity shares) of at least

one bank.

Many holding companies hold only a small minority of the outstanding shares of one or

more banks, thereby escaping government regulation. However, if a holding company

seeks to control a U.S. bank, it must seek approval from the Federal Reserve Board to

become a registered bank holding company. Under the terms of the Bank Holding Com-

pany Act, control is assumed to exist if the holding company acquires 25 percent or more

of the outstanding equity shares of at least one bank or can elect at least two directors of

at least one bank. Once registered, the company must submit to periodic examinations by

the Federal Reserve Board and receive approval from the Fed when it reaches out to

acquire other businesses.

Why Holding Companies Have Grown

The growth of holding companies has been rapid in recent decades. As long ago as 1971

these organizations controlled banks holding about half of U.S. bank deposits. By 2004,

the nearly 6,000 bank holding companies operating in the United States controlled in

excess of 90 percent of the industrys assets. Just over 6,200 U.S. commercial banks were

affiliated with bank holding companies as 2004 drew to a close. (A list of the 10 largest

U.S. bank holding companies appears in Table 33.) The principal reasons for this rapid

upsurge in bank holding company activity include their greater ease of access to capital

markets in raising funds, their ability to use higher leverage (more debt capital relative to

equity capital) than nonaffiliated banking firms, their tax advantages in being able to off-

set profits from one business with losses generated by other firms that are part of the same

company, and their ability to expand into businesses outside banking.

One-Bank Holding Companies

Most registered bank holding companies in the United States are one-bank companies. By

the beginning of the 21st century, about 5,000 of the roughly 6,000 bank holding compa-

nies in the United States controlled stock in just one bank.

78 Part One Introduction to the Business of Banking and Financial-Services Management

RoseHudgins: Bank

Management and Financial

Services, Seventh Edition

I. Introduction to the

Business of Banking and

FinancialServices

Management

3. The Organization and

Structure of Banking and

the FinancialServices

Industry

The McGrawHill

Companies, 2008

However, these one-bank companies frequently owned and operated one or more nonbank busi-

nesses as well. Once a bank holding company registers with the Federal Reserve Board, any nonbank

business activities it starts or acquires must first be approved by the Fed. These nonbank businesses must

offer services closely related to banking that also yield public benefits, such as improved availability

of financial services or lower service prices. (See Table 34 for examples of nonbank businesses that reg-

istered holding companies are allowed to own and control.) Today, the principal advantage for bank

holding companies entering nonbank lines of business is the prospect of diversifying sources of revenue

and profits (and, therefore, reducing risk exposure).

Chapter 3 The Organization and Structure of Banking and the Financial-Services Industry 79

VIRTUAL BANKS

The rapid growth of Internet access and the millions of daily

Web transactions by the public soon brought thousands of

financial-service providers to the Internet. Most Web sites in

the early years were information-only sitesfor example,

describing services offered or explaining how to reach the

nearest branch office. As the 21st century began, however,

the most rapidly growing financial-service Web sites were of

the transactions variety where the customer could access

basic services (e.g., checking account balances, transferring

funds, and paying bills) and, in a growing number of cases,

access extended services (including access to credit and the

ability to make investments in securities).

Initially, most of these Web sites were established by con-

ventional banks that also operated brick-and-mortar, full-service

branch offices. More recently, however, a cadre of virtual banks

has emerged that do not operate conventional branches, but

work exclusively over the Internet and through the ATMs of the

banks. Some have qualified for FDIC deposit insurance and

offer an expanding menu of services, though many remain

unprofitable.

Some of the most prominent virtual banks are listed below

along with their Web site addresses. You may want to explore

how these banks are organized and what services they sell to

the public.

E-Trade Bank (www.etradebank.com)

Netbank (www.netbank.com)

First Internet Bank of Indiana (www.firstib.com)

National Interbank (www.nationalinterbank.com)

Bank of Internet USA (www.bankofinternet.com)

Juniper Bank (www.juniper.com)

E - B A NK I NG A ND E - C O MME R C E

Bank Holding Company Name Location of Headquarters Total Assets ($Bill)

Citigroup, Inc. New York City, New York $1,490

(www.citigroup.com)

Bank of America Corporation Charlotte, North Carolina 1,214

(www.BankofAmerica.com)

JPMorgan Chase & Co. New York City, New York 1,178

(www.jpmorganchase.com)

Wachovia Corporation Charlotte, North Carolina 507

(www.wachovia.com)

Wells Fargo & Company San Francisco, California 435

(www.wellsfargo.com)

Taunus Corporation New York City, New York 362

(www.taunus.com)

HSBC North America Holdings Inc. Prospect Heights, Illinois 351

(www.hsbcusa.com)

U.S. Bancorp Minneapolis, Minnesota 199

(www.usbank.com)

SunTrust Banks, Inc. Atlanta, Georgia 165

(www.suntrust.com)

Citizens Financial Group, Inc. Providence, Rhode Island 142

(www.citizensbank.com)

TABLE 33

The 10 Largest Bank

Holding Companies

Operating in the

United States

(Total Assets as

Reported on March

31, 2005)

Source: National Information

Center, Federal Reserve

System.

Key URL

Banks not affiliated with

holding companies are

represented in industry and

legislative affairs by the

Independent Community

Bankers of America at

www.ibaa.org.

RoseHudgins: Bank

Management and Financial

Services, Seventh Edition

I. Introduction to the

Business of Banking and

FinancialServices

Management

3. The Organization and

Structure of Banking and

the FinancialServices

Industry

The McGrawHill

Companies, 2008

80 Part One Introduction to the Business of Banking and Financial-Services Management

TABLE 34

The Most Important

Nonbank Financially

Related Businesses

Registered Holding

Companies Can

Acquire under U.S.

Banking Regulations

Finance Companies

Lend funds to businesses and households.

Mortgage Companies

Provide short-term credit to improve real

property for residential or commercial use.

Data Processing Companies

Provide computer processing services and

information transmission.

Factoring Companies

Purchase accounts receivable from businesses

in exchange for supplying temporary financing.

Security Brokerage Firms

Execute customer buy and sell orders for

securities, foreign exchange, financial futures,

and option contracts.

Financial Advising

Advise institutions and high-net-worth individual

customers on managing assets, mergers,

reorganizations, raising capital, and feasibility

studies.

Credit Insurance Underwriters

Supply insurance coverage to customers

borrowing money to guarantee repayment

of a loan.

Merchant Banking

Invest in corporate stock as well as loan money

to help finance the start of new ventures or

to support the expansion of existing businesses.

Investment Banking Firms

Purchase new U.S. government and municipal

bonds and corporate stocks and bonds from

issuers and offer these securities to buyers

(permissible for well-managed and well-

capitalized holding companies).

Trust Companies

Manage the property of businesses, individuals,

and nonprofit organizations and place

customers securities with private investors.

Credit Card Companies

Provide short-term credit to individuals and

businesses in order to support retail trade.

Leasing Companies

Purchase and lease assets for businesses and

individuals needing the use of these assets.

Insurance Companies and Agencies

Sell or underwrite insurance polices to

businesses and individuals in order to provide

risk protection.

Real Estate Services

Supply real estate appraisals, arrange for the

financing of real estate projects, and broker real

properties.

Savings Associations

Offer savings deposit plans and housing-related

credit, predominantly to individuals and families.

The holding company form permits the de jure (legal) separation between banks and

nonbank businesses having greater risk, allowing these different firms to be owned by the

same group of stockholders. Outside the United States, the holding company form is usu-

ally legal but not often used. Instead most industrialized countries allow banks themselves

to offer more services or permit a bank to set up a subsidiary company under direct bank

ownership and sell services that banks themselves are not allowed to offer.

Multibank Holding Companies

A minority of bank holding company organizations are multibank holding companies.

Multibank companies number just under 900 but control close to 70 percent of the total

assets of all U.S. banking organizations. Prior to the Riegle-Neal Act (1994), this form of

banking organization appealed especially to bank stockholders and managers who wanted

to set up an interstate banking organization composed of several formerly independent

banking firms. One very dramatic effect of holding company expansion has been a sharp

decline in the number of independently owned banking organizations.

A bank holding company that wishes to acquire 5 percent or more of the equity shares

of an additional bank must seek approval from the Federal Reserve Board and demonstrate

that such an acquisition will not significantly damage competition, will promote public

convenience, and will better serve the publics need for financial services. Banks acquired

by holding companies are referred to as affiliated banks. (See Exhibit 38.) Banks that are

not owned by holding companies are known as independent banks.

RoseHudgins: Bank

Management and Financial

Services, Seventh Edition

I. Introduction to the

Business of Banking and

FinancialServices

Management

3. The Organization and

Structure of Banking and

the FinancialServices

Industry

The McGrawHill

Companies, 2008

Chapter 3 The Organization and Structure of Banking and the Financial-Services Industry 81

Multibank Holding Corporation

Affiliated

nonbank

businesses

Affiliated

bank

Affiliated

bank

Affiliated

bank

EXHIBIT 38

The Multibank

Holding Company

Advantages and Disadvantages of Holding Company Banking

Many of the advantages and disadvantages associated with branch banking have also

been claimed by proponents and opponents of holding company banking. Thus, holding

company banking has been blamed for reducing competition as it swallows up formerly

independent banks, for overcharging customers, for ignoring the credit needs of smaller

towns and cities, and for accepting too much risk. In contrast, supporters of the holding

company movement claim greater efficiency, more services available to customers, lower

probability of organizational failure, and higher and more stable profits.

If holding companies actually reduce competition, we might expect this to result in higher

profits for holding company banks relative to other banks. There is, however, little convinc-

ing evidence that this has happened. But while individual banks may not benefit from acqui-

sition by holding companies, the holding company as a whole tends to be more profitable

than banking organizations that do not form holding companies. Moreover, the failure rate for

holding company banks appears to be below that of comparable-size independent banks.

There is at least anecdotal evidence that multibank holding companies drain scarce

capital from some communities and may sometimes weaken smaller towns and rural areas.

For example, there may be a tendency in some small cities for local funds to be siphoned

away in an effort to shore up troubled lead banks of major holding companies, meaning

that less credit may be available for local community projects. Some customers of holding-

company banks complain about the rapid turnover of bank personnel, the lack of person-

alized service, and long delays when local office managers were forced to refer questions to

the companys home office.

As we saw earlier, holding companies have reached outside the banking business in

recent years, acquiring or starting insurance companies, security underwriting firms, and

other businesses. Have these nonbank acquisitions paid off? If added profitability was the

goal, the results must be described as disappointing thus far. Frequently, acquiring compa-

nies have lacked sufficient experience with nonbank products to manage their nonbank

firms successfully. However, not all nonbank business ventures of holding companies have

been unprofitable. Certainly, the attractiveness of using nonbank firms as a vehicle for

interstate expansion has declined somewhat with the continuing spread of full-service

interstate banking across the United States.

Factoid

Which type of banking

organization holds more

than 90 percent of all U.S.

banking assets?

Answer: Holding

companies.

Concept Check

39. What is a bank holding company?

310. When must a holding company register with the

Federal Reserve Board?

311. What nonbank businesses are bank holding com-

panies permitted to acquire under the law?

312. Are there any significant advantages or disadvan-

tages for holding companies or the public if these

companies acquire banks or nonbank business

ventures?

Factoid

Which type of banking

organization holds more

than 90 percent of all

U.S. banking assets?

Answer: Holding

companies.

RoseHudgins: Bank

Management and Financial

Services, Seventh Edition

I. Introduction to the

Business of Banking and

FinancialServices

Management

3. The Organization and

Structure of Banking and

the FinancialServices

Industry

The McGrawHill

Companies, 2008

35 Interstate Banking and the Riegle-Neal Interstate Banking

and Branching Efficiency Act of 1994

Many authorities today confidently predict that full-service interstate banking eventually

will invade virtually every corner of the United States. We saw in Chapter 2 that the fed-

eral government took a giant step toward this goal when the U.S. Congress passed the

Riegle-Neal Interstate Banking and Branching Efficiency Act of 1994an action sup-

ported by most of the states. Riegle-Neal allows holding companies operating in the

United States to acquire banks throughout the nation without needing any states permis-

sion to do so and to establish branch offices across state lines in every state (except Mon-

tana, which opted out of interstate branching).

Why did the federal government enact and the states support interstate banking laws

in 1994 after so many years of resistance, especially by community banks, to the very idea

of interstate expansion? Multiple factors were at work:

The need to bring in new capital to revive struggling local economies.

The expansion of financial-service offerings by nonbank financial institutions that face

few restrictions on their ability to expand nationwide.

A strong desire on the part of the largest banks to geographically diversify their opera-

tions and open up new marketing opportunities.

The belief among regulators that large banks may be more efficient and less prone to

failure.

Advances in the technology of financial-services delivery, permitting banks to serve

customers over broader geographic areas.

Proponents of interstate banking believe that it will bring new capital into states that

are rapidly growing and short of investment capital, result in greater convenience for the

customer (especially if the customer is traveling or changing residence to another state),

and stimulate competitive rivalry that will promote greater efficiency and lower prices for

financial services. Interstate expansion may also bring greater stability by allowing indi-

vidual banking organizations to further diversify their operations across different markets,

offsetting losses that may arise in one market with gains in other markets.

Not everyone agrees, however. Some economists contend that interstate banking may

lead to increases in market concentration as smaller banks are merged into larger interstate

organizations, possibly leading to less competition and higher prices and to the draining of

funds from local areas into distant financial centers. Indeed, on a nationwide basis concen-

tration of resources in the largest banks has significantly increased. The top 100 U.S. banks

held only about half of all U.S. domestic banking assets in 1980, but by 2000 their propor-

tion of the nations domestic banking assets had climbed to more than 70 percent. By 2005

the three largest U.S. banking companies controlled nearly a quarter of all domestic deposits

and the largest domestic bank, Bank of America, accounted for nearly 10 percent of nation-

wide deposits. However, small banks seem to have little to fear from large interstate organi-

zations if the former are willing to compete aggressively for their customers business.

Doesnt this national concentration trend suggest possible damage to the consumer? Not

necessarily. Many experts believe that those customers most likely to be hurt by a reduced

number of competitorsthe potentially most damaged marketare households and small

businesses that trade for financial services mainly in smaller cities and towns. Interestingly

enough, there has apparently been little change in the concentration of bank deposits at

the local level in many metropolitan areas and rural counties. Therefore, it appears that in

the interstate banking movement, thus far, many customers, particularly the smallest, have

seen little change in their many alternatives for obtaining financial services.

82 Part One Introduction to the Business of Banking and Financial-Services Management

RoseHudgins: Bank

Management and Financial

Services, Seventh Edition

I. Introduction to the

Business of Banking and

FinancialServices

Management

3. The Organization and

Structure of Banking and

the FinancialServices

Industry

The McGrawHill

Companies, 2008

Concentration in the United States, measured by the share of assets and deposits held

by the largest banks in the system, is among the lowest in the world. For example, while

the three largest banking organizations in the United States hold about a quarter of the

U.S. banking industrys assets, in most other industrialized countries (such as Canada,

France, Germany, the Netherlands, Spain, Sweden, and Switzerland), half or more of all

banking assets rest in the hands of the three largest banking companies. No American

bank yet has a banking franchise physically present in all 50 states.

Research on Interstate Banking

Recent research suggests that the actual benefits the public and bank stockholders can

expect from the expansion of full-service interstate banking may be limited. For example,

an interesting study by Goldberg and Hanweck [4] of the few early interstate banking

organizations protected by grandfather provisions of federal law found that banks previ-

ously acquired across state lines did not gain on their in-state competitors. In fact, these

older interstate-controlled banks actually lost market share over time and were, on aver-

age, no more profitable than were neighboring banks serving the same states. Moreover,

studies by Rose [6, 7] of interstate bank acquisitions found that many of the banks acquired

across state lines were in poor financial condition, which limited the growth and prof-

itability of the interstate banking firms that acquired them.

Employees seem to have more opportunity for promotions in an expanding interstate

banking organization. However, many of the largest interstate firms (for example, J. P.

Morgan Chase and Bank of America) frequently have laid off substantial numbers of

employees in acquired businesses in an effort to cut expenses and increase efficiency. On

the other hand, some interstate firms have experienced an increase in the market value

of their stock when laws were passed permitting interstate banking, suggesting that stock

market investors regarded the trend toward nationwide banking as a positive event for

the industry.

In theory at least, if an interstate organization can acquire banks in states where

bank earnings have a negative or low-positive correlation with bank earnings in those

states where the interstate company is already represented, a portfolio effect could

occur. Earnings losses at banks in one group of states could offset profits earned at banks

in other states, resulting in lower overall earnings risk for the interstate banking firm as

a whole. However, research by Levonian [5] and Rose [8] suggests that reduction of

bank earnings risk does not occur automatically simply because a banking organization

crosses state lines. To achieve at least some reduction in earnings risk, interstate banks

must expand into a number of different states (at least four) and different regions (at

least two economically distinct regions of the nation). The bottom line is that interstate

banking organizations must be selective about which states they enter if risk reduction is an

important consideration.

36 Two Alternative Types of Banking Organizations Available as the 21st

Century Opened: Financial Holding Companies (FHCs) and Bank Subsidiaries

In 1999 the landmark Gramm-Leach-Bliley (GLB) Act moved U.S. banking closer to the

concept of universal banking, popular in Europe, in which banks merge with security and

insurance firms and sell other financial products as well. To allow banks to offer selected

nonbank financial services (especially selling or underwriting insurance and trading in or

underwriting securities) the new law opened wide the door to two forms of banking orga-

nizations: the financial holding company and the bank subsidiaries type organization, as

illustrated in Exhibit 39.

Chapter 3 The Organization and Structure of Banking and the Financial-Services Industry 83

Key URL

The most important

banking industry trade

association,

representing the

industry as a whole, is

the American Bankers

Association at

www.aba.com.

RoseHudgins: Bank

Management and Financial

Services, Seventh Edition

I. Introduction to the

Business of Banking and

FinancialServices

Management

3. The Organization and

Structure of Banking and

the FinancialServices

Industry

The McGrawHill

Companies, 2008

The Financial Holding Company (FHC)

Financial Services Holding

Company

Bank

Insurance

Agencies Selling

Policies

Security

Purchases

and Sales

Travel Agencies

and Other

Subsidiaries

Insurance

Agencies

Selling Policies

and Insurance

Underwriting

Commercial

Bank or

Banks

Security

Purchases and

Sales and

Investment Banking

(Underwriting)

Merchant

Bank

Travel Agencies

and Other

Affiliates

Real Estate

Development

Company

Affiliated Firms Affiliated Firms

The Bank Subsidiaries Approach

Subsidiary Firms

EXHIBIT 39

Two New Bank

Organization

Models

Real Banks, Real Decisions

THE SUPER STORE NEXT DOOR

While depository institutions have been branching across the nation and forming holding companies

to offer a bewildering array of new services, they have suddenly found themselves facing a potentially

formidable foe from the retailing sector. Many financial firms have discovered recently that their

toughest competitor of the future may not be the bank, finance company, or insurance agency next

door but a super store giant that has been remarkably successful in reaching into hundreds of

towns in every state and beyond. Wal-Martthe worlds biggest retailerseems to be creeping into

financial services, perhaps slowly at first but with an apparent momentum that few can safely ignore.

For example, in 2005 Wal-Mart submitted an application to the State of Utah, in an effort to estab-

lish an industrial bankessentially a small finance company providing loans and savings accounts to

industrial workers. Earlier Wal-Mart apparently had attempted to purchase an industrial bank in Cali-

fornia and also reached across the Canadian border in an effort to partner with Toronto-Dominion

Bank. However, these adventures seemed to hit a stone wall.

Undaunted, Wal-Mart found other promising pathways and today its financial-services division

appears to be outgrowing many of its older lines of goods and services. It now sells money orders,

wires money to distant locations (including Mexico), partners with Discover in a credit-card program,