You might also like

- Credit Report Secrets: How to Understand What Your Credit Report Says About You and What You Can Do About It!From EverandCredit Report Secrets: How to Understand What Your Credit Report Says About You and What You Can Do About It!Rating: 1 out of 5 stars1/5 (1)

- Debt Collector Disclosure Statement For Credit Card Same As One For PDFDocument6 pagesDebt Collector Disclosure Statement For Credit Card Same As One For PDFMichael Plaster100% (4)

- I GIVE YOU CREDIT: A DO IT YOURSELF GUIDE TO CREDIT REPAIRFrom EverandI GIVE YOU CREDIT: A DO IT YOURSELF GUIDE TO CREDIT REPAIRNo ratings yet

- B - Letter 1 - 1st Dispute Letter To Pretend LenderDocument5 pagesB - Letter 1 - 1st Dispute Letter To Pretend Lenderbigwheel897% (32)

- Declaration of Fraud - Debt CollectorDocument3 pagesDeclaration of Fraud - Debt CollectorJulie Hatcher-Julie Munoz Jackson100% (33)

- Credit Freeze and Data Repair StrategiesFrom EverandCredit Freeze and Data Repair StrategiesRating: 5 out of 5 stars5/5 (2)

- Dealing With Credit Card StatementsDocument3 pagesDealing With Credit Card Statementsjpes100% (6)

- How to Get Rid of Your Unwanted Debt: A Litigation Attorney Representing Homeowners, Credit Card Holders & OthersFrom EverandHow to Get Rid of Your Unwanted Debt: A Litigation Attorney Representing Homeowners, Credit Card Holders & OthersRating: 3 out of 5 stars3/5 (1)

- Validation of Debt PackDocument9 pagesValidation of Debt Packpreston_40200378% (9)

- Debt Validation Proof of ClaimDocument5 pagesDebt Validation Proof of ClaimPhil95% (66)

- Debt Validation #1: Always Mail Certified Return Signature RequestedDocument7 pagesDebt Validation #1: Always Mail Certified Return Signature RequestedMooreTrust88% (24)

- Debt Validation Letter 2020Document6 pagesDebt Validation Letter 2020Nat Williams97% (29)

- How to Make Your Credit Card Rights Work for You: Save MoneyFrom EverandHow to Make Your Credit Card Rights Work for You: Save MoneyNo ratings yet

- Affidavit of Loan Denial - FDCPADocument4 pagesAffidavit of Loan Denial - FDCPAPublic Knowledge98% (49)

- Affidavit ExperianDocument2 pagesAffidavit ExperianMill Bey80% (5)

- CCA DisputeLettersDocument45 pagesCCA DisputeLettersgabby maca100% (3)

- Credit Restore Secrets They Never Wanted You to KnowFrom EverandCredit Restore Secrets They Never Wanted You to KnowRating: 4 out of 5 stars4/5 (3)

- AFFIDAVIT Debt CollectorDocument1 pageAFFIDAVIT Debt Collector1bruceman100% (2)

- Prove A Creditor Is in Violation - Automatic Win For $1000Document7 pagesProve A Creditor Is in Violation - Automatic Win For $1000FreedomofMind100% (11)

- Validation of Debt Disbute LetterDocument2 pagesValidation of Debt Disbute Lettercolemanbe07No ratings yet

- Attack The Debt CollectorDocument9 pagesAttack The Debt CollectorMichael Peterson97% (32)

- 14 Debt ValidationDocument6 pages14 Debt Validationstarhoney82% (11)

- Debt Validation & Proof of Claim IIDocument2 pagesDebt Validation & Proof of Claim IIPhil98% (40)

- Debt Validation InstructionsDocument2 pagesDebt Validation InstructionsKNOWLEDGE SOURCE100% (18)

- Affidavit of Demand For Verification of DebtDocument2 pagesAffidavit of Demand For Verification of DebtZelimir100% (4)

- Debt Validation & Proof of Claim IIDocument2 pagesDebt Validation & Proof of Claim IIPhil95% (20)

- First Presentment Verification of DebtDocument8 pagesFirst Presentment Verification of DebtHorsetail Goatsfoot100% (8)

- Debt Elimination StatementDocument2 pagesDebt Elimination StatementKeith Kauhi100% (6)

- Sample Student Loan Debt Validation LetterDocument3 pagesSample Student Loan Debt Validation LetterStan Burman100% (20)

- Credit Repair Letter To Send After Debt DischargeDocument6 pagesCredit Repair Letter To Send After Debt Dischargeamenelbey78% (9)

- Tough Debt Validation Letter 1Document2 pagesTough Debt Validation Letter 1Elcana Mathieu90% (10)

- Collection Letter - StrongDocument6 pagesCollection Letter - StrongPublic Knowledge95% (22)

- Stop Paying Affidavit (Template)Document3 pagesStop Paying Affidavit (Template)Akil Bey93% (27)

- Sprint UtilitiesDocument4 pagesSprint Utilitiesgordon scottNo ratings yet

- Truth in Lending - Affidavit - TemplateDocument12 pagesTruth in Lending - Affidavit - TemplateMarsha Maines100% (14)

- Debt Collector Verification LetterDocument2 pagesDebt Collector Verification LetterPublic Knowledge100% (20)

- Have Fun With Debt CollectorsDocument3 pagesHave Fun With Debt CollectorsTitle IV-D Man with a plan94% (16)

- Credit Repair Letter This Is An Attempt To Validate A DebtDocument7 pagesCredit Repair Letter This Is An Attempt To Validate A DebtZIONCREDITGROUP89% (9)

- Better Creditor LetterDocument2 pagesBetter Creditor LetterMarc Beaumont100% (1)

- Debt Validation Letter 2019-04-22Document4 pagesDebt Validation Letter 2019-04-22Brandy sisson100% (1)

- The 3 Must Send Letters On Validation of DebtDocument5 pagesThe 3 Must Send Letters On Validation of Debtwicholacayo96% (73)

- Bankster in Dishonour - Updated: Notice of Acceptance For ValueDocument56 pagesBankster in Dishonour - Updated: Notice of Acceptance For ValueKNOWLEDGE SOURCE100% (4)

- FDCPA PitfallsDocument35 pagesFDCPA Pitfallsspcbanking100% (2)

- Awesome Debt Validation LetterDocument27 pagesAwesome Debt Validation Letterbalestrery85% (55)

- CleanUpCreditProcedures STEP 2Document3 pagesCleanUpCreditProcedures STEP 2Michael Kovach50% (4)

- Debt Validation Proof Default 2Document6 pagesDebt Validation Proof Default 2spcbanking80% (5)

- TILA Rescission Success Without Tender - HENRY BOTELHO, Plaintiff, V. U.S. BANK, N.a., As Trustee For The LXS 2007-4N Trust, DefendantDocument6 pagesTILA Rescission Success Without Tender - HENRY BOTELHO, Plaintiff, V. U.S. BANK, N.a., As Trustee For The LXS 2007-4N Trust, DefendantForeclosure Fraud100% (4)

- Notice of Dispute - Proof of Claim - Debt Validation Template 8-10-10 Copy 3Document4 pagesNotice of Dispute - Proof of Claim - Debt Validation Template 8-10-10 Copy 3Nessie Jenkins95% (43)

- Sample Debt Verification LetterDocument22 pagesSample Debt Verification LetterCurt E Daniels100% (3)

- Debt Validation LetterDocument2 pagesDebt Validation Letterha1392100% (5)

- CRDT CRD LTR 1 - Template - (Proof of Claim)Document4 pagesCRDT CRD LTR 1 - Template - (Proof of Claim)Julie Hatcher-Julie Munoz Jackson100% (10)

- Dispute The Debt LetterDocument4 pagesDispute The Debt Lettercamwills2100% (5)

- 2013.06.28 Debt Validation LetterDocument3 pages2013.06.28 Debt Validation Letteraquacool21No ratings yet

- Remove My Name From Mailing List 4Document1 pageRemove My Name From Mailing List 4KNOWLEDGE SOURCE100% (3)

- Credit Repair Retainer AgreementDocument3 pagesCredit Repair Retainer AgreementKNOWLEDGE SOURCE100% (2)

- Nimrod TeachingDocument10 pagesNimrod TeachingKNOWLEDGE SOURCENo ratings yet

- ConqeringDocument5 pagesConqeringKNOWLEDGE SOURCENo ratings yet

- Moonphases Seminar by Lew WhiteDocument67 pagesMoonphases Seminar by Lew WhiteLew White100% (3)

- 6 Non Response Creditor Refused To RespondDocument2 pages6 Non Response Creditor Refused To RespondKNOWLEDGE SOURCE100% (2)

- Virginia Power Stop FC LawsDocument3 pagesVirginia Power Stop FC LawsKNOWLEDGE SOURCENo ratings yet

- Interrogatories RequestDocument6 pagesInterrogatories RequestKNOWLEDGE SOURCE100% (1)

- Why Credit Restoration WorksDocument3 pagesWhy Credit Restoration WorksKNOWLEDGE SOURCE100% (3)

- Untitled 1 MotivationDocument4 pagesUntitled 1 MotivationKNOWLEDGE SOURCE100% (1)

- Delete Judgements and Accounts CraDocument6 pagesDelete Judgements and Accounts CraKNOWLEDGE SOURCE100% (30)

- Transunion Follow UpDocument1 pageTransunion Follow UpKNOWLEDGE SOURCENo ratings yet

- Use For Mortgage CompanyDocument4 pagesUse For Mortgage CompanyKNOWLEDGE SOURCE100% (6)

- Untitled 1 3Document13 pagesUntitled 1 3KNOWLEDGE SOURCE100% (2)

- Form 96Document3 pagesForm 96KNOWLEDGE SOURCE0% (1)

- Virginia Power Stop FC LawsDocument3 pagesVirginia Power Stop FC LawsKNOWLEDGE SOURCENo ratings yet

- Top Kicking ValidationDocument7 pagesTop Kicking ValidationKNOWLEDGE SOURCE60% (5)

- Delete Judgements and Accounts CraDocument6 pagesDelete Judgements and Accounts CraKNOWLEDGE SOURCE100% (30)

- Virginia Power Stop FC LawsDocument3 pagesVirginia Power Stop FC LawsKNOWLEDGE SOURCENo ratings yet

- 12 2 10KeatingOnAngelaStarkDocument3 pages12 2 10KeatingOnAngelaStarkKNOWLEDGE SOURCE100% (11)

- Virginia Power Stop FC LawsDocument3 pagesVirginia Power Stop FC LawsKNOWLEDGE SOURCENo ratings yet

- Advice For Closing MortgagesDocument4 pagesAdvice For Closing MortgagesMegan McAuley83% (6)

- 9 01 2005 FTB Hop 2Document9 pages9 01 2005 FTB Hop 2KNOWLEDGE SOURCENo ratings yet

- 08 ReinertDocument29 pages08 ReinertKNOWLEDGE SOURCENo ratings yet

- Affidavit 3Document5 pagesAffidavit 3KNOWLEDGE SOURCE100% (2)

- Bankster in Dishonour - Updated: Notice of Acceptance For ValueDocument56 pagesBankster in Dishonour - Updated: Notice of Acceptance For ValueKNOWLEDGE SOURCE100% (4)

- 2nd Letter To BureauDocument8 pages2nd Letter To BureauKNOWLEDGE SOURCENo ratings yet

- Fcra Section 609 and 605 LetterDocument15 pagesFcra Section 609 and 605 LetterKNOWLEDGE SOURCE96% (51)

- Fix Google ChromeDocument5 pagesFix Google ChromeKNOWLEDGE SOURCENo ratings yet

- 609 2Document2 pages609 2KNOWLEDGE SOURCE67% (3)

- Wiley - Chapter 7: Cash and ReceivablesDocument33 pagesWiley - Chapter 7: Cash and ReceivablesIvan Bliminse100% (2)

- Partnership - Installment Liquidation Joint Ventures: Roxas, Soto, and TodaDocument27 pagesPartnership - Installment Liquidation Joint Ventures: Roxas, Soto, and TodamarieieiemNo ratings yet

- Business Math DictionaryDocument25 pagesBusiness Math DictionaryReinan Ezekiel Sotto Llagas100% (1)

- Intacc 1a Reviewer Conceptual Framework and Accounting StandardsDocument32 pagesIntacc 1a Reviewer Conceptual Framework and Accounting StandardsKrizahMarieCaballeroNo ratings yet

- NCERT Solutions For Class 11 Accountancy Chapter 10 Financial Statements - 2Document90 pagesNCERT Solutions For Class 11 Accountancy Chapter 10 Financial Statements - 2Badal singh ThakurNo ratings yet

- Bank Branch Audit and RBI GuidelineDocument62 pagesBank Branch Audit and RBI Guidelinebudi.hw748No ratings yet

- Accounting For Pensions and Postretirement Benefits: Assignment Classification Table (By Topic)Document71 pagesAccounting For Pensions and Postretirement Benefits: Assignment Classification Table (By Topic)Andreas AndreanoNo ratings yet

- CH 07Document8 pagesCH 07Antonios FahedNo ratings yet

- Customer Inquiry ReportDocument4 pagesCustomer Inquiry ReportHartito HargiastoNo ratings yet

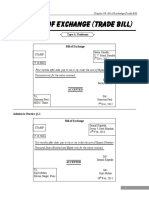

- 09 Bills of ExchangeDocument37 pages09 Bills of ExchangeAnas shaikh100% (1)

- Misc. Problem Items To Be Researched: GL Account #Document8 pagesMisc. Problem Items To Be Researched: GL Account #komaliNo ratings yet

- 7160 - FAR Preweek ProblemDocument14 pages7160 - FAR Preweek ProblemMAS CPAR 93No ratings yet

- Amalgamation: Question Text Option - A Option - B Option - C Option - D SolutionDocument13 pagesAmalgamation: Question Text Option - A Option - B Option - C Option - D SolutionPAWAN CHHABRIANo ratings yet

- AOM 2023-001 UpperDocument16 pagesAOM 2023-001 UpperKen BocsNo ratings yet

- 6072-P1-Lembar JawabanDocument32 pages6072-P1-Lembar JawabanFitria NingrumNo ratings yet

- Cambridge O Level: ACCOUNTING 7707/22Document20 pagesCambridge O Level: ACCOUNTING 7707/22Tapiwa MT (N1c3isH)No ratings yet

- Statement of Accounts: Dealer DetailsDocument4 pagesStatement of Accounts: Dealer Detailssanju maneppagolNo ratings yet

- Accountant Answer Key All SessionDocument123 pagesAccountant Answer Key All Sessiontongocharli100% (1)

- Exercise DayDocument30 pagesExercise DayThai Anh HoNo ratings yet

- Pre and Post of Accounting 2Document14 pagesPre and Post of Accounting 2Nancy AtentarNo ratings yet

- Home Depot Financial QuestionDocument3 pagesHome Depot Financial Questionmktg1990No ratings yet

- Gmernacej W5C5 AssigmentOLDDocument6 pagesGmernacej W5C5 AssigmentOLDalmaNo ratings yet

- Class 11 Accountancy Part 1 Chapter 1Document9 pagesClass 11 Accountancy Part 1 Chapter 1Ioanna Maria MonopoliNo ratings yet

- ReSA B45 AFAR First PB Exam - Questions, Answers - SolutionsDocument23 pagesReSA B45 AFAR First PB Exam - Questions, Answers - SolutionsDhainne Enriquez100% (1)

- Accounts ReceivableDocument5 pagesAccounts ReceivableDianna DayawonNo ratings yet

- Ca xxxxx09 009 2021331Document8 pagesCa xxxxx09 009 2021331lauraNo ratings yet

- Learning Check Chapter 14Document12 pagesLearning Check Chapter 14ratihspNo ratings yet

- MBA 2 Accounting For Decision Making Jan 2014Document208 pagesMBA 2 Accounting For Decision Making Jan 2014rajabbanda100% (1)

- The Adjustment Process: Prepaid. Unearned RevenueDocument10 pagesThe Adjustment Process: Prepaid. Unearned RevenueEliz Saw0% (1)

- Oartnership: AccouDocument1 pageOartnership: AccouShoyo HinataNo ratings yet