You might also like

- Section 1: 10-K (10-K) : United States Securities and Exchange CommissionDocument129 pagesSection 1: 10-K (10-K) : United States Securities and Exchange CommissionSamir GhoshNo ratings yet

- 2015 Annual Report Complete enDocument236 pages2015 Annual Report Complete enSamir GhoshNo ratings yet

- 2015 Annual Report Compensation Report enDocument10 pages2015 Annual Report Compensation Report enSamir GhoshNo ratings yet

- Johnson & Johnson JNJ Stock-Sample Analysis Report Intrinsic ValueDocument12 pagesJohnson & Johnson JNJ Stock-Sample Analysis Report Intrinsic ValueOld School Value100% (2)

- Avanti Field Insights PDFDocument15 pagesAvanti Field Insights PDFSamir GhoshNo ratings yet

- Soa10134 DR 129329 - Good PDFDocument38 pagesSoa10134 DR 129329 - Good PDFSamir GhoshNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5783)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

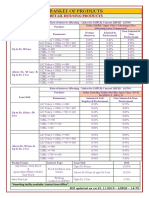

- BASKET OF RETAIL PRODUCTS RATESDocument3 pagesBASKET OF RETAIL PRODUCTS RATESVirendra K VermaNo ratings yet

- Vendor Supplier Registration Information SheetDocument3 pagesVendor Supplier Registration Information SheetEnzo MarquezNo ratings yet

- MPBFDocument6 pagesMPBFhiteshgauranaNo ratings yet

- Reverse Charge Mechanism in GST Regime With ChartDocument6 pagesReverse Charge Mechanism in GST Regime With ChartSwathi VikashiniNo ratings yet

- The Founding Fathers, 30 Years OnDocument8 pagesThe Founding Fathers, 30 Years OnJames WarrenNo ratings yet

- Financial Accounting and Accounting StandardDocument18 pagesFinancial Accounting and Accounting StandardZahidnsuNo ratings yet

- Week 10 Compiled PDFDocument12 pagesWeek 10 Compiled PDFChaNo ratings yet

- Presentation KenwoodDocument18 pagesPresentation KenwoodAsfand KhanNo ratings yet

- ISO 37001: Anti-Bribery Management System StandardDocument10 pagesISO 37001: Anti-Bribery Management System StandardNada ChraibiNo ratings yet

- Af ManifestDocument23 pagesAf ManifestCwasi Musicman100% (1)

- PMEGP Scheme प्रधानमंत्री रोजगार सृजन कार्यक्रमDocument31 pagesPMEGP Scheme प्रधानमंत्री रोजगार सृजन कार्यक्रमAbinash MandilwarNo ratings yet

- Table B5: Bank-Wise Non-Performing Assets (Npas) of Scheduled Commercial Banks - 2006Document2 pagesTable B5: Bank-Wise Non-Performing Assets (Npas) of Scheduled Commercial Banks - 2006Rekha BaiNo ratings yet

- Corporate Strategies: 10 Case StudiesDocument7 pagesCorporate Strategies: 10 Case StudiesBskTeja0% (2)

- DETAILS OF G.OsDocument16 pagesDETAILS OF G.OsRaghu Ram50% (2)

- Fiat Case StudyDocument10 pagesFiat Case StudyVipra PandeyNo ratings yet

- Principles of Taxation I SyllabusDocument7 pagesPrinciples of Taxation I SyllabusShreyaNo ratings yet

- NLRC Lacks Jurisdiction in Labor Case Involving Foreign EmployerDocument2 pagesNLRC Lacks Jurisdiction in Labor Case Involving Foreign EmployerAnsis Villalon PornillosNo ratings yet

- Internship Report NiB BankDocument10 pagesInternship Report NiB BankAbdul WaheedNo ratings yet

- Nestle USA Grainger purchases and paymentsDocument81 pagesNestle USA Grainger purchases and paymentsnelsonNo ratings yet

- Bella v1Document4 pagesBella v1ug8No ratings yet

- ElectroluxDocument3 pagesElectroluxRupeet Singh100% (1)

- Jack Trout - Trout On StrategyDocument5 pagesJack Trout - Trout On StrategyCosmin StefanNo ratings yet

- Office Order Unit HeadDocument31 pagesOffice Order Unit HeadRajkumar PrasadNo ratings yet

- Megaworld 1st Quarter 2019 Financial ReportDocument29 pagesMegaworld 1st Quarter 2019 Financial ReportRyan CervasNo ratings yet

- Global Strategy Mike PengDocument28 pagesGlobal Strategy Mike PengRui Fernando Correia FerreiraNo ratings yet

- Law DigestDocument4 pagesLaw DigestPatricia Adora AlcalaNo ratings yet

- Lista de Empresas Bolivianas Vinculadas en El Caso Panamá PapersDocument6 pagesLista de Empresas Bolivianas Vinculadas en El Caso Panamá PapersLos Tiempos DigitalNo ratings yet

- CEO Road Rules1Document233 pagesCEO Road Rules1sammyyankee100% (1)

- Novartis AcquistionDocument17 pagesNovartis AcquistionashkuchiyaNo ratings yet

- GE Commercial Distribution Finance Corporation v. Frost Hardware Company Et Al - Document No. 3Document3 pagesGE Commercial Distribution Finance Corporation v. Frost Hardware Company Et Al - Document No. 3Justia.comNo ratings yet