1 Center for American Progress | Important Insights on College Choice and the Burden of Student-Loan Debt

Important Insights on College Choice

and the Burden of Student-Loan Debt

By Elizabeth Baylor and Olivia Murray June 24, 2014

Completing higher education afer high school continues to be the most reliable way

for Americans to expand their economic opportunity. Students gain skills that not only

let them achieve a secure economic future, but also allow them to experience fulflling

professional opportunities. For many students and families, this means taking on debt to

pay for a degree at a college, university, or technical training center.

During the 2011-12 school year, higher-education institutions collected $154 billion in

tuition and fees; families and students fnanced these costs with $106 billion in loans

from federal student-aid programs.

1

Given this level of borrowing, it is important that

the United States reform its fnancial aid system so that students can make the best

educational choices to ensure their fnancial success. Te country must also provide

loan repayment options that allow people to manage the debt they take on in order to

get their degrees.

Late last year, the Center for American Progress highlighted the importance of under-

standing the role that student debt plays in the college selection process.

2

In particular,

the CAP column discussed the fact that many people choose a college without a clear

sense of how student-loan debt will afect their lives afer they leave school.

Te people most suited to provide insight into a discussion about the impact of stu-

dent-loan debt are those who are working hard to pay of student loans. Terefore, this

analysis describes results from a survey of the indebted individuals that CAP frst wrote

about in December 2013.

3

Tis brief outlines the perspectives of student borrowers in

the ongoing conversation about student debt and college success and presents some

important policies that can help minimize student-loan borrowing and make repay-

ment more afordable.

2 Center for American Progress | Important Insights on College Choice and the Burden of Student-Loan Debt

Survey of borrower perspectives on student-loan debt and

college choice

As members of the Higher Ed, Not Debt campaign, the Center for American Progress

and its youth-advocacy team, Generation Progress, conducted a survey of former

students with loans and asked them questions about whether they thought about debt

when choosing a college. Te survey asked these students how likely they would be now,

afer experiencing loan repayment, to consider debt important to their college choice.

A total of 27,686 former students answered the four survey questions examined for this

analysis. By its design and defnition, it included the perspectives of people who are con-

cerned about student-loan debt; students who did not borrow to fnance their education

are less likely to respond to a survey that covers these topics. Te survey sought informa-

tion about how borrowers evaluated the impact of debt afer leaving the postsecondary

education system in order to see if it is possible to beter direct the choices of incoming

students so they can minimize their student-loan debt.

Tis issue brief examines the survey results across four key topics: level of education, the

amount of debt owed, the factors considered upon college enrollment, and the factors

most important afer leaving school and entering loan repayment. It organizes this infor-

mation based on the amount of debt students had when they lef school and the level

of degree they atained. Te brief also compares this information to the respondents

answers about their top factors for choosing a school at the time of enrollment versus

their top factors now. In particular, it examines if borrowers included net price as one

of their top fve factors for selecting a college at either point. Net price is defned as the

amount paid for tuition and fees afer discounting scholarships and grants that do not

need to be repaid.

About the survey respondents

As stated above, this survey collected responses on the four survey questions from

27,686 people with various levels of education and debt. Tis analysis provides insights

into the priorities and situations of students with varying degree levels. Table 1 lists the

education levels of those surveyed and the number of respondents at each level.

3 Center for American Progress | Important Insights on College Choice and the Burden of Student-Loan Debt

Te debt levels for people who responded to this survey are worrying, but they are

likely higher than the debt levels of all former students. Te Institute for College Access

and Success estimated that 71 percent of all students from the class of 2012 who earned

a bachelors degree borrowed to fnance their education, and the average amount of

debt incurred was $29,400.

4

CAPs survey, which included graduates, nongraduates,

and students at every education level, found that only 11 percent of borrowers had debt

levels equal to or less than $10,000. At the other end of the spectrum, 24 percent of

survey respondents had very high debt levelsmore than $100,000. And 72 percent

had high or very high debt levelsmore than $30,000. (see Figure 1) Tis information

provides an opportunity to understand the factors that people struggling with student-

loan debt considered when they enrolled in college, as well as how their atitudes have

changed over time.

TABLE 1

Number of respondents by degree level and amount of debt owed

Level of education

Number of

respondents

Low levels of debt,

less than $10,000

Moderate levels

of debt,

$10,000$30,000

High levels of debt,

$30,000$100,000

Very high levels of

debt, more than

$100,000

Some college 2,663 650 788 1,058 167

Associate's degree 2,016 366 634 935 81

Bachelor's degree 9,691 1,037 1,948 5,340 1,366

Master's degree 9,496 720 922 5,072 2,782

Professional degree 2,397 149 110 573 1,565

Ph.D. 1,423 211 104 418 690

Total 27,686 3,133 4,506 13,396 6,651

Source: Authors analysis of survey responses.

FIGURE 1

Share of borrowers at each debt level

Debt range

6%

2%

3%

7%

Source: Authors' analysis of survey responses.

None

$0$5,000

$5,000$10,000

$10,000$20,000

$20,000$30,000

$30,000$40,000

$40,000$50,000

$50,000$100,000

$100,000$150,000

$150,000$200,000

$200,000 or more

9%

9%

10%

13%

6%

5%

29%

4 Center for American Progress | Important Insights on College Choice and the Burden of Student-Loan Debt

Student borrowers at all debt levels now recognize the importance of

college cost

Te most signifcant takeaway from this analysis is that student borrowers paying

back their loans weigh the importance of a colleges cost more heavily now than they

did when they were making their selection. Indeed, the more debt students hold,

the more pronounced the gap is between weighing the importance of debt then and

weighing the importance of debt now. Across all survey respondents, 24.6 percent of

borrowers said that net price was one of their top fve most important factors while

they were selecting a college, and 60.3 percent of respondents said they would put it

in their top fve now. (see Table 2)

TABLE 2

Share of respondents who said cost was important both when choosing a

college and now

Debt owed Percent at enrollment Percent now

None 26.6% 39.1%

$0$5,000 31.4% 49.3%

$5,000$10,000 28.5% 51.5%

$10,000$20,000 30.4% 57.4%

$20,000$30,000 28.5% 62.3%

$30,000$40,000 24.9% 62.6%

$40,000$50,000 25.7% 65.5%

$50,000$100,000 22.1% 67.9%

$100,000$150,000 17.8% 68.8%

$150,000$200,000 18.0% 68.7%

$200,000 or more 17.1% 70.0%

All respondents 24.6% 60.3%

Source: Authors analysis of survey responses.

Te responses show those who are most likely and those who are least likely to consider

net price as one of the most important factors in school selection. Te students who

accumulated the most debt were the least likely to put net price in their top fve factors

when they enrolled in college and the most likely to put it in their top fve factors now.

Students who accumulated the least amount of debt were the most likely to put net price

in their top fve factors while choosing a college and the least likely to put it in their top

fve factors now.

5 Center for American Progress | Important Insights on College Choice and the Burden of Student-Loan Debt

It is notable that the more debt student borrowers hold, the less likely they are to have

considered cost when enrolling in school. Only 18 percent of those who lef school

with very high levels of debtmore than $100,000listed net price among their

top fve initial factors, while 28 percent of those with low levels of debtless than

$10,000did so.

Low levels of debt

Very high levels of debt

FIGURE 3

Share of respondents who considered cost when enrolling in college

Source: Authors' analysis of survey responses.

28%

18%

At every level of education and debt, more respondents put net price as a current top

factor for choosing a college. Te smallest percentage-point increase from the time of

choosing a college to now was 12.6 percentage points for those with no debt; the biggest

increase was 52.9 percentage points for those with more than $200,000 of debt. Tis dif-

ference suggests that those who did highly value the cost generally do not leave school

wishing they had not. It is therefore important for lawmakers, educational leaders, and

federal aid administrators to create a lending environment in which minimizing student-

loan debt is the goal.

Debt range

When choosing a college

Now

FIGURE 2

Share of respondents who said cost was important both when

choosing a college and now

Source: Authors' analysis of survey responses.

None

$0$5,000

$5,000$10,000

$10,000$20,000

$20,000$30,000

$30,000$40,000

$40,000$50,000

$50,000$100,000

$100,000$150,000

$150,000$200,000

$200,000 or more

27%

31% 49%

29% 52%

30%

29% 62%

25% 63%

26% 66%

22% 68%

18% 69%

18% 69%

17% 70%

39%

57%

6 Center for American Progress | Important Insights on College Choice and the Burden of Student-Loan Debt

Present all student borrowers with a standardized shopping sheet to

evaluate college cost

Te Obama administration released its Financial Aid Shopping Sheet in July 2012,

which was aimed at promoting college afordability by demystifying the debt students

will incur when they enroll in a program.

5

Te form communicates information related

to fnancial aid and makes clear the diference between institutional aid, grant aid that

does not have to be repaid, and the amount of student loans that will be required to

meet educational expenses. In particular, it includes information about the potential

monthly payments that students would have to pay if they enrolled in particular institu-

tions. It is designed to help students compare potential debt levels and aimed at simpli-

fying the cost information students and their families receive so it is easier for them to

make informed comparisons among institutions.

Te shopping sheet is a common-sense reform that will help incoming students easily

understand potential debt. Tis type of information has been presented successfully in

other contexts: For example, the Credit CARD Act mandated that credit card statements

present standardized information on how long it would take [users] to pay of the card if

they made only minimum paymentsand how much interest they would be charged.

6

However, some institutions have resisted. Inside Higher Ed reported that some colleges

consider the shopping sheet to be too one-size-fts-all.

7

A standardized approach to

fnancial aid award leters would provide exactly the change needed. It is critical that stu-

dents considering multiple institutions understand the diferences between fnancial aid

ofers before accepting one. It is also important that students understand how much of

their aid package has to be repaid. Currently, 2,072 institutions have voluntarily adopted

the U.S. Department of Educations Financial Aid Shopping Sheet.

8

Undergraduate stu-

dents at these institutions represent 47 percent of total enrollment at the undergraduate

level; this level of participation is a great start, but it is not enough.

Te Financial Aid Shopping Sheet should be mandatory for institutions that participate

in federal student-loan programs. Tis recommendation is not new: CAP frst called

for this urgently needed reform in its 2011 report, New Financial Aid Award Leters

Should Be Mandatory: Tey Need to Be Comparable to Be Efective.

9

Standardize student loans to make repayment plans affordable

Most borrowers are working hard to responsibly make their monthly payments,

but many still struggle with burdensome debt. On June 9, President Barack Obama

announced steps his administration is taking to make student debt easier to repay and

college more afordable and accessible.

10

His plan would expand the Pay As You Earn, or

PAYE, plan to all direct-loan borrowers, which would provide approximately 5 million

7 Center for American Progress | Important Insights on College Choice and the Burden of Student-Loan Debt

people with relief by capping their payments at 10 percent of their monthly incomes.

Afer 20 years of payments, any balance that remains will be forgiven. Te goal of

President Obamas announcement is to make this expanded eligibility available to bor-

rowers by December 2015.

11

PAYE promises to keep student debt manageable for the borrowers who are eligible,

but repayment options for all student-loan borrowers need to be enhanced. To date, no

borrower enrolled in the PAYE plan has reached the 20-year threshold for loan forgive-

ness.

12

To ensure that people are not burdened at the back end, loan forgiveness should

not be subject to federal income tax.

Conclusion

Many analyses, including this one, show that student-loan debt is a problem, but it is

clear that college is well worth the fnancial investment.

13

Student borrowers are work-

ing hard to beter their economic circumstances through education, but the choices

they make about where to atend school and how much to borrow have lasting efects.

It is critically important to intervene at the enrollment point so that students know the

impact of taking out loans, as well as to foster a culture at higher-education institutions

that minimizes student-loan debt. It is also important to focus on making repayment

more afordable.

Elizabeth Baylor is Associate Director of Postsecondary Education at the Center for American

Progress. Olivia Murray is an intern with the Postsecondary Education Policy team at the Center.

8 Center for American Progress | Important Insights on College Choice and the Burden of Student-Loan Debt

Endnotes

1 David A. Bergeron, What Does Value Look Like in Higher

Education?, Center for American Progress, January 29, 2014,

available at http://americanprogress.org/issues/higher-

education/news/2014/01/29/83094/what-does-value-look-

like-in-higher-education/.

2 Elizabeth Baylor and Sarah Audelo, What Do You Wish You

Had Known About Student-Loan Debt and College Choice?,

Center for American Progress, December 12, 2013, available

at http://americanprogress.org/issues/higher-education/

news/2013/12/12/80908/what-do-you-wish-you-had-

known-about-student-loan-debt-and-college-choice/.

3 Ibid.

4 The Institute for College Access & Success, Student Debt

and the Class of 2012 (2013), available at http://projecton-

studentdebt.org/fles/pub/classof2012.pdf.

5 Cecilia Muoz, New Shopping Sheet Will Make It Easier for

Students to Know Before They Owe,The White House Blog,

July 24, 2012, available at http://www.whitehouse.gov/

blog/2012/07/24/new-shopping-sheet-will-make-it-easier-

students-know-they-owe.

6 Joe Valenti, Protecting Consumers Five Years After Credit

Card Reform (Washington: Center for American Progress,

2014), available at http://americanprogress.org/issues/

economy/report/2014/05/22/90198/protecting-consumers-

fve-years-after-credit-card-reform.

7 Libby A. Nelson, Tangling Over Accountability, Inside

Higher Ed, February 5, 2013, available at http://www.inside-

highered.com/news/2013/02/05/heated-discussion-federal-

regulations-naicu-panel#sthash.h4gQ3FtZ.CeoP6Ykj.dpbs.

8 U.S. Department of Education, Institutions that have adopted

the Shopping Sheet (2014), available at http://www2.ed.gov/

policy/highered/guid/aid-ofer/index.html.

9 Julie Margetta Morgan, New Financial Aid Award Letters

Should Be Mandatory: They Need to Be Comparable to Be

Efective, Center for American Progress, September 12,

2011, available at http://americanprogress.org/issues/labor/

news/2011/09/12/10221/new-fnancial-aid-award-letters-

should-be-mandatory/.

10 The White House, FACTSHEET: Making Student Loans

More Afordable, Press release, June 9, 2014, available at

http://www.whitehouse.gov/the-press-ofce/2014/06/09/

factsheet-making-student-loans-more-afordable.

11 Ibid.

12 Ibid.

13 The Domestic Policy Council and the Council of Economic

Advisors, Taking Action: Higher Education and Student Debt

(The White House, 2014), available at http://www.white-

house.gov/sites/default/fles/docs/student_debt_report_f-

nal.pdf

You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Housing The Extended FamilyDocument57 pagesHousing The Extended FamilyCenter for American Progress100% (1)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Preventing Problems at The Polls: North CarolinaDocument8 pagesPreventing Problems at The Polls: North CarolinaCenter for American ProgressNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- An Infrastructure Plan For AmericaDocument85 pagesAn Infrastructure Plan For AmericaCenter for American ProgressNo ratings yet

- Fast Facts: Economic Security For Arizona FamiliesDocument4 pagesFast Facts: Economic Security For Arizona FamiliesCenter for American ProgressNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- America Under Fire: An Analysis of Gun Violence in The United States and The Link To Weak Gun LawsDocument46 pagesAmerica Under Fire: An Analysis of Gun Violence in The United States and The Link To Weak Gun LawsCenter for American Progress0% (1)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Workin' 9 To 5: How School Schedules Make Life Harder For Working ParentsDocument91 pagesWorkin' 9 To 5: How School Schedules Make Life Harder For Working ParentsCenter for American ProgressNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hyde Amendment Has Perpetuated Inequality in Abortion Access For 40 YearsDocument10 pagesThe Hyde Amendment Has Perpetuated Inequality in Abortion Access For 40 YearsCenter for American ProgressNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Costs of Climate InactionDocument9 pagesThe Costs of Climate InactionCenter for American ProgressNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Missing LinkDocument25 pagesThe Missing LinkCenter for American ProgressNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Home Visiting 101Document2 pagesHome Visiting 101Center for American ProgressNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- ENG - (Press Release) PermataBank and Kredivo Team Up For Rp1 Trillion Credit LineDocument2 pagesENG - (Press Release) PermataBank and Kredivo Team Up For Rp1 Trillion Credit LineTubagus Aditya NugrahaNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Microeconomics ProjectDocument5 pagesMicroeconomics ProjectRakesh ChoudharyNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Garuda Indonesia Vs Others, Winning The Price WarDocument16 pagesGaruda Indonesia Vs Others, Winning The Price Waryandhie570% (1)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- "Training and Action Research of Rural Development Academy (RDA), Bogra, Bangladesh." by Sheikh Md. RaselDocument101 pages"Training and Action Research of Rural Development Academy (RDA), Bogra, Bangladesh." by Sheikh Md. RaselRasel89% (9)

- Application of Memebership Namrata DubeyDocument2 pagesApplication of Memebership Namrata DubeyBHOOMI REALTY AND CONSULTANCY - ADMINNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- 5% Compound PlanDocument32 pages5% Compound PlanArvind SinghNo ratings yet

- Ministry-Wise Schemes and Developments Prelims 2019 PDFDocument214 pagesMinistry-Wise Schemes and Developments Prelims 2019 PDFAditya KumarNo ratings yet

- Tentative Renovation Cost EstimatesDocument6 pagesTentative Renovation Cost EstimatesMainit VOnNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- C2 PPT Pipe Jacking PVCDocument43 pagesC2 PPT Pipe Jacking PVCvroogh primeNo ratings yet

- Avtex W270TSDocument1 pageAvtex W270TSAre GeeNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Center For Strategic and International Studies (CSIS)Document13 pagesCenter For Strategic and International Studies (CSIS)Judy Ann ShengNo ratings yet

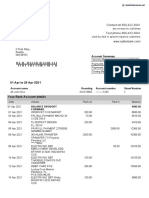

- Acct Statement XX1924 01122022Document10 pagesAcct Statement XX1924 01122022Yakshit YadavNo ratings yet

- Understanding EntrepreneurshipDocument277 pagesUnderstanding Entrepreneurshiphannaatnafu100% (1)

- DSA 2016 Malaysian ExhibitorsDocument6 pagesDSA 2016 Malaysian ExhibitorsShenie GutierrezNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- JournalsDocument6 pagesJournalsharmen-bos-9036No ratings yet

- Outward Remittance Form PDFDocument2 pagesOutward Remittance Form PDFAbhishek GuptaNo ratings yet

- Folder Gründen in Wien Englisch Web 6-10-17Document6 pagesFolder Gründen in Wien Englisch Web 6-10-17rodicabaltaNo ratings yet

- Guidance Note On GSTDocument50 pagesGuidance Note On GSTkjs gurnaNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Sutton Bank StatementDocument2 pagesSutton Bank StatementNadiia AvetisianNo ratings yet

- Voyage Accounting ExampleDocument4 pagesVoyage Accounting Exampledharmawan100% (1)

- Day Trading StrategiesDocument3 pagesDay Trading Strategiesswetha reddy100% (2)

- Evio Productions Company ProfileDocument45 pagesEvio Productions Company ProfileObliraj KrishnarajNo ratings yet

- Health Mitra PamphletDocument2 pagesHealth Mitra Pamphletharshavardhanak23No ratings yet

- Ikhlayel 2018Document41 pagesIkhlayel 2018Biswajit Debnath OffcNo ratings yet

- United States of America v. George PeltzDocument10 pagesUnited States of America v. George PeltzWHYY NewsNo ratings yet

- 617 NP BookletDocument77 pages617 NP BookletDexie Cabañelez ManahanNo ratings yet

- HM ExpansionDocument21 pagesHM Expansionafatonys0% (1)

- Chapter 7Document6 pagesChapter 7jobhihtihjrNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- 5 Examples of Arrangements of The GHS Label ElementsDocument7 pages5 Examples of Arrangements of The GHS Label ElementsBayu KristyonoNo ratings yet

- Scaffold Tube Storage Racks: 1 of 6 August 2021Document6 pagesScaffold Tube Storage Racks: 1 of 6 August 2021Matthew PowellNo ratings yet