You might also like

- Hallmark SonaliDocument4 pagesHallmark SonaliMilon SultanNo ratings yet

- Solutions Chapter 13Document4 pagesSolutions Chapter 13Imroz MahmudNo ratings yet

- Effect of Dividend Announcement On Shareholders' Value Evidence From Dhaka Stock ExchangeDocument17 pagesEffect of Dividend Announcement On Shareholders' Value Evidence From Dhaka Stock ExchangeMD. REZAYA RABBINo ratings yet

- Current Affairs BCS SpecialDocument240 pagesCurrent Affairs BCS SpecialImroz MahmudNo ratings yet

- Chapter 07 Solutions ManualDocument12 pagesChapter 07 Solutions ManualImroz MahmudNo ratings yet

- Research TypesDocument8 pagesResearch TypesImroz MahmudNo ratings yet

- Criteria of A Good ResearchDocument2 pagesCriteria of A Good ResearchImroz Mahmud67% (9)

- IpoDocument5 pagesIpoImroz MahmudNo ratings yet

- Research ProblemDocument4 pagesResearch ProblemImroz MahmudNo ratings yet

- Measuring Exposure To Exchange Rate FluctuationsDocument38 pagesMeasuring Exposure To Exchange Rate FluctuationsImroz MahmudNo ratings yet

- Multinational Capital BudgetingDocument17 pagesMultinational Capital BudgetingImroz MahmudNo ratings yet

- Country Risk AnalysisDocument32 pagesCountry Risk AnalysisImroz MahmudNo ratings yet

- Global Financial Crisis and Its Impact On Bangladesh's EconomyDocument55 pagesGlobal Financial Crisis and Its Impact On Bangladesh's EconomyImroz Mahmud0% (1)

- Time Value of MoneyDocument36 pagesTime Value of MoneyImroz MahmudNo ratings yet

- Business Plan of A Theme ParkDocument73 pagesBusiness Plan of A Theme ParkImroz Mahmud60% (5)

- Stock Market of BangladeshDocument31 pagesStock Market of BangladeshImroz Mahmud88% (8)

- Beta Calculation & Analysis of Bangladesh Leather IndustryDocument22 pagesBeta Calculation & Analysis of Bangladesh Leather IndustryImroz Mahmud100% (1)

- The 14th Dhaka International Trade FairDocument5 pagesThe 14th Dhaka International Trade FairImroz MahmudNo ratings yet

- TitanDocument52 pagesTitanImroz MahmudNo ratings yet

- E-Commerce:: E-Business Is The Use of The Internet and Other Networks andDocument13 pagesE-Commerce:: E-Business Is The Use of The Internet and Other Networks andImroz MahmudNo ratings yet

- Problem & Solutions of Toyota Motor CorporationDocument5 pagesProblem & Solutions of Toyota Motor CorporationImroz Mahmud73% (15)

- SugarcaneDocument37 pagesSugarcaneImroz MahmudNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- 39 1 Vijay KelkarDocument14 pages39 1 Vijay Kelkargrooveit_adiNo ratings yet

- Mock Meeting Perhentian Kecil IslandDocument3 pagesMock Meeting Perhentian Kecil IslandMezz ShiemaNo ratings yet

- Anser Key For Class 8 Social Science SA 2 PDFDocument5 pagesAnser Key For Class 8 Social Science SA 2 PDFSoumitraBagNo ratings yet

- Full Download Business in Action 6th Edition Bovee Solutions ManualDocument35 pagesFull Download Business in Action 6th Edition Bovee Solutions Manuallincolnpatuc8100% (32)

- 64 Development of Power Operated WeederDocument128 pages64 Development of Power Operated Weedervinay muleyNo ratings yet

- Veit Tunel 1Document7 pagesVeit Tunel 1Bladimir SolizNo ratings yet

- Portfolio October To December 2011Document89 pagesPortfolio October To December 2011rishad30No ratings yet

- Sustainability in The Built Environment Factors AnDocument7 pagesSustainability in The Built Environment Factors AnGeorges DoungalaNo ratings yet

- Filetype PDF Journal of Real Estate Finance and EconomicsDocument2 pagesFiletype PDF Journal of Real Estate Finance and EconomicsJennaNo ratings yet

- Salary Slip Template V12Document5 pagesSalary Slip Template V12Matthew NiñoNo ratings yet

- Od124222428139339000 4Document2 pagesOd124222428139339000 4biren shahNo ratings yet

- 6 The Neoclassical Summary Free Trade As Economic GoalDocument4 pages6 The Neoclassical Summary Free Trade As Economic GoalOlga LiNo ratings yet

- N 1415 Iso - CD - 3408-5 - (E) - 2003 - 08Document16 pagesN 1415 Iso - CD - 3408-5 - (E) - 2003 - 08brunoagandraNo ratings yet

- SMR0275 Four Horsemen of The American Apocalypse ReportDocument44 pagesSMR0275 Four Horsemen of The American Apocalypse Reportmaat3x3No ratings yet

- New Economic Policy of IndiaDocument23 pagesNew Economic Policy of IndiaAbhishek Singh Rathor100% (1)

- Booking Invoice M06ai23i01024843Document2 pagesBooking Invoice M06ai23i01024843AkshayMilmileNo ratings yet

- IELTS Writing Task 1 Sample - Bar Chart - ZIMDocument28 pagesIELTS Writing Task 1 Sample - Bar Chart - ZIMPhương Thư Nguyễn HoàngNo ratings yet

- Udai Pareek Scal For SES RuralDocument3 pagesUdai Pareek Scal For SES Ruralopyadav544100% (1)

- Pasamuros PTD 308 - PentairDocument5 pagesPasamuros PTD 308 - PentairJ Gabriel GomezNo ratings yet

- Clean Wash EN 2Document2 pagesClean Wash EN 2Sean HongNo ratings yet

- Superstocks Final Advance Reviewer'sDocument250 pagesSuperstocks Final Advance Reviewer'sbanman8796% (24)

- Womens Hostel in BombayDocument5 pagesWomens Hostel in BombayAngel PanjwaniNo ratings yet

- Partnership Dissolution Lecture NotesDocument7 pagesPartnership Dissolution Lecture NotesGene Marie PotencianoNo ratings yet

- Advantages and Disadvantages of Shares and DebentureDocument9 pagesAdvantages and Disadvantages of Shares and Debenturekomal komal100% (1)

- Attacking and Defending Through Operations - Fedex: Assignment Submitted By: Pradeep DevkarDocument14 pagesAttacking and Defending Through Operations - Fedex: Assignment Submitted By: Pradeep Devkarsim4misNo ratings yet

- Dennis Redmond Adorno MicrologiesDocument14 pagesDennis Redmond Adorno MicrologiespatriceframbosaNo ratings yet

- Bill 1.1Document2 pagesBill 1.1Александр ТимофеевNo ratings yet

- Report Sugar MillDocument51 pagesReport Sugar MillMuhammadAyyazIqbal100% (1)

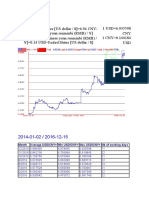

- Month Average USD/CNY Min USD/CNY Max USD/CNY NB of Working DaysDocument3 pagesMonth Average USD/CNY Min USD/CNY Max USD/CNY NB of Working DaysZahid RizvyNo ratings yet

- ChartsDocument4 pagesChartsMyriam GGoNo ratings yet