You might also like

- Livro Química Analítica Qualitativa - VogelDocument617 pagesLivro Química Analítica Qualitativa - VogelDaniel PrettiNo ratings yet

- Precision of Internal Standard and External Standard Methods in High Performance Liquid ChromatographyDocument15 pagesPrecision of Internal Standard and External Standard Methods in High Performance Liquid ChromatographySoma GhoshNo ratings yet

- WHO guidelines on good agricultural and collection practices for medicinal plantsDocument80 pagesWHO guidelines on good agricultural and collection practices for medicinal plantsGarnasih Putri RastitiNo ratings yet

- GACP Trainers ManualDocument23 pagesGACP Trainers ManualSoma GhoshNo ratings yet

- Part IV - Coastal Wetlands Pp. 155-156Document3 pagesPart IV - Coastal Wetlands Pp. 155-156Soma GhoshNo ratings yet

- The Complete Guide To Global Social Media Marketing - HubSpotDocument71 pagesThe Complete Guide To Global Social Media Marketing - HubSpotRudy Torres VillegasNo ratings yet

- Cambridge Books OnlineDocument3 pagesCambridge Books OnlineSoma GhoshNo ratings yet

- QA PharmaceuticalDocument413 pagesQA Pharmaceuticalalhalili100% (9)

- GMP1Document247 pagesGMP1OHanbaliNo ratings yet

- Mee270 ch12Document51 pagesMee270 ch12Soma GhoshNo ratings yet

- Part V - Rocky Shores Pp. 207-208Document3 pagesPart V - Rocky Shores Pp. 207-208Soma GhoshNo ratings yet

- Cambridge Books OnlineDocument3 pagesCambridge Books OnlineSoma GhoshNo ratings yet

- Threads and Fasteners Smith IVCCDocument26 pagesThreads and Fasteners Smith IVCCNathan GarciaNo ratings yet

- Part Vi - Soft Shores Pp. 261-262Document3 pagesPart Vi - Soft Shores Pp. 261-262Soma GhoshNo ratings yet

- Part Viii Part Vii SynthesisDocument2 pagesPart Viii Part Vii SynthesisSoma GhoshNo ratings yet

- Cambridge Books OnlineDocument3 pagesCambridge Books OnlineSoma GhoshNo ratings yet

- 23 - Trends and Global Prospects of The Earth's Aquatic Ecosystems Pp. 353-365Document14 pages23 - Trends and Global Prospects of The Earth's Aquatic Ecosystems Pp. 353-365Soma GhoshNo ratings yet

- Cambridge Books OnlineDocument3 pagesCambridge Books OnlineSoma GhoshNo ratings yet

- ContentsDocument2 pagesContentsSoma GhoshNo ratings yet

- 19 - Continental-Shelf Benthic Ecosystems Prospects For An Improved Environmental Future Pp. 295-308Document15 pages19 - Continental-Shelf Benthic Ecosystems Prospects For An Improved Environmental Future Pp. 295-308Soma GhoshNo ratings yet

- 20 - The Marine Pelagic Ecosystem Perspectives On Humanity's Role in The Future Pp. 311-318Document9 pages20 - The Marine Pelagic Ecosystem Perspectives On Humanity's Role in The Future Pp. 311-318Soma GhoshNo ratings yet

- 22 - The Near Future of The Deep-Sea Floor Ecosystems Pp. 334-350Document18 pages22 - The Near Future of The Deep-Sea Floor Ecosystems Pp. 334-350Soma GhoshNo ratings yet

- 18 - Seagrass Ecosystems Their Global Status and Prospects Pp. 281-294Document15 pages18 - Seagrass Ecosystems Their Global Status and Prospects Pp. 281-294Soma GhoshNo ratings yet

- 21 - Polar and Ice-Edge Marine Systems Pp. 319-333Document16 pages21 - Polar and Ice-Edge Marine Systems Pp. 319-333Soma GhoshNo ratings yet

- 14 - Rocky Intertidal Shores Prognosis For The Future Pp. 209-225Document18 pages14 - Rocky Intertidal Shores Prognosis For The Future Pp. 209-225Soma GhoshNo ratings yet

- 15 - Current Status and Future Trends in Kelp Forest Ecosystems Pp. 226-241Document17 pages15 - Current Status and Future Trends in Kelp Forest Ecosystems Pp. 226-241Soma GhoshNo ratings yet

- 17 - Sandy Shores of The Near Future Pp. 263-280Document19 pages17 - Sandy Shores of The Near Future Pp. 263-280Soma GhoshNo ratings yet

- 16 - Projecting The Current Trajectory For Coral Reefs Pp. 242-260Document20 pages16 - Projecting The Current Trajectory For Coral Reefs Pp. 242-260Soma GhoshNo ratings yet

- 12 - Future of Mangrove Ecosystems To 2025 Pp. 172-187Document17 pages12 - Future of Mangrove Ecosystems To 2025 Pp. 172-187Soma GhoshNo ratings yet

- 13 - Environmental Future of Estuaries Pp. 188-206Document20 pages13 - Environmental Future of Estuaries Pp. 188-206Soma GhoshNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5783)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Distributing Printer Via The InternetDocument12 pagesDistributing Printer Via The InternetWaroeng Panggoeng100% (1)

- Incoterms: Eneral NformationDocument4 pagesIncoterms: Eneral NformationrooswahyoeNo ratings yet

- Varsha GoyalDocument36 pagesVarsha Goyalajay sharmaNo ratings yet

- Intangibles PDFDocument5 pagesIntangibles PDFJer RamaNo ratings yet

- Tan Shuy v. MaulawinDocument1 pageTan Shuy v. MaulawinJennilyn Tugelida100% (1)

- PhilAm LIFE vs. Secretary of Finance Case DigestDocument2 pagesPhilAm LIFE vs. Secretary of Finance Case DigestDenn Reed Tuvera Jr.No ratings yet

- Carrefour's Asian Market StrategiesDocument2 pagesCarrefour's Asian Market StrategiesAisha AliNo ratings yet

- 491 Leigh Ave Version 2Document2 pages491 Leigh Ave Version 2justusleagueNo ratings yet

- Mysore Sandal Baby Soap - ReportDocument30 pagesMysore Sandal Baby Soap - Reportabhijitg22No ratings yet

- Mis Case StudyDocument1 pageMis Case StudyAnirudh PrabhuNo ratings yet

- Selling Price: Rate WorkDocument4 pagesSelling Price: Rate WorkLara SinapiloNo ratings yet

- Gears Magazine March 2013Document76 pagesGears Magazine March 2013Rodger Bland100% (7)

- TracoDocument47 pagesTracokiran rajNo ratings yet

- BCG Mocks IcebergDocument5 pagesBCG Mocks IcebergGerman VegaNo ratings yet

- Vice President Merchandising Production in NYC Resume Wendie SchuermanDocument2 pagesVice President Merchandising Production in NYC Resume Wendie SchuermanWendieSchuerman100% (1)

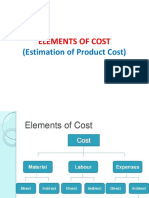

- Elements of CostDocument42 pagesElements of CostNinad MirajgaonkarNo ratings yet

- Run Worldwide: With SAP® Global Trade ServicesDocument17 pagesRun Worldwide: With SAP® Global Trade ServicesNagesh Caparthy100% (1)

- Mckinsey Full ArticleDocument6 pagesMckinsey Full Articleakhi_bheNo ratings yet

- Ethics and AirbusDocument3 pagesEthics and AirbusgobindaNo ratings yet

- Indirect Channel Partner Agreement - ROW Aug 2019 Confidential Information Page 1 of 28Document28 pagesIndirect Channel Partner Agreement - ROW Aug 2019 Confidential Information Page 1 of 28Rifki NugrahaNo ratings yet

- Case Analysis WalMart3Document6 pagesCase Analysis WalMart3Pei Wing GanNo ratings yet

- WIKI - The Income StatementDocument2 pagesWIKI - The Income StatementHanna GeguillanNo ratings yet

- Yummy Ice Cream Presentation SummaryDocument34 pagesYummy Ice Cream Presentation SummaryUsamaNo ratings yet

- How To Fill Up Product Replacement FormDocument7 pagesHow To Fill Up Product Replacement FormDoraaina100% (1)

- Chapter IIDocument16 pagesChapter IIMaria Ryzza Corlet DelenNo ratings yet

- Merchandising Operations Income StatementDocument8 pagesMerchandising Operations Income StatementMondy MondyNo ratings yet

- Effects of Accounting TransactionsDocument3 pagesEffects of Accounting TransactionsDella IsabellaNo ratings yet

- Ma2451 Engineering Economics and Cost AnalysisDocument5 pagesMa2451 Engineering Economics and Cost AnalysisRamaswamy SubbiahNo ratings yet

- Direct Posting From FI - MM To CO-PADocument6 pagesDirect Posting From FI - MM To CO-PAManas Kumar SahooNo ratings yet

- Business Plan Photography StudioDocument32 pagesBusiness Plan Photography StudioMandeep Batra38% (8)