You might also like

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Tata Nano - Perceptual Study PDFDocument10 pagesTata Nano - Perceptual Study PDFWilliam McconnellNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Sap mm01Document1 pageSap mm01Jayashree ChatterjeeNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Chisquare in Spss 1209705384088874 8Document10 pagesChisquare in Spss 1209705384088874 8Jayashree ChatterjeeNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- EconomicsDocument8 pagesEconomicsJayashree ChatterjeeNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- EconomicsDocument8 pagesEconomicsJayashree ChatterjeeNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- D.K. Yadav Vs J.M.A. Industries LTD On 7 May, 1993 PDFDocument9 pagesD.K. Yadav Vs J.M.A. Industries LTD On 7 May, 1993 PDFJayashree ChatterjeeNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Factor AnalysisDocument36 pagesFactor AnalysisJayashree Chatterjee100% (2)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Celebrating Cerebration 2013 - QuizTalkDocument9 pagesCelebrating Cerebration 2013 - QuizTalkJayashree ChatterjeeNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Ohrabrujuce Liderstvo I Kreativnost Zaposlenih8Document23 pagesOhrabrujuce Liderstvo I Kreativnost Zaposlenih8Ana StevanovicNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- AISHE201011Document140 pagesAISHE201011Jayashree ChatterjeeNo ratings yet

- Automobile Industry in IndiaDocument37 pagesAutomobile Industry in IndiaKiran DuggarajuNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- PV Industry 201103Document15 pagesPV Industry 201103Aditya SharmaNo ratings yet

- ZUST Marketing Lecture 3 - Segmenting and Targeting MarketsDocument34 pagesZUST Marketing Lecture 3 - Segmenting and Targeting MarketsJayashree ChatterjeeNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- HM Annual Report 2010 11 (With Subsidiaries)Document138 pagesHM Annual Report 2010 11 (With Subsidiaries)mrgauravaNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Apprentice Trainee Management Development Plan April 2012Document6 pagesApprentice Trainee Management Development Plan April 2012Jayashree ChatterjeeNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- ZUST Marketing Lecture 3 - Segmenting and Targeting MarketsDocument34 pagesZUST Marketing Lecture 3 - Segmenting and Targeting MarketsJayashree ChatterjeeNo ratings yet

- Annual Report and Accounts 2011 2012Document146 pagesAnnual Report and Accounts 2011 2012Surbhi JainNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Educational Statistics at A GlanceDocument45 pagesEducational Statistics at A GlanceJayashree ChatterjeeNo ratings yet

- Intro ERP Using GBI GBI Slides en v2.20Document15 pagesIntro ERP Using GBI GBI Slides en v2.20Jayashree ChatterjeeNo ratings yet

- AISHE201011Document140 pagesAISHE201011Jayashree ChatterjeeNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- AISHE201011Document140 pagesAISHE201011Jayashree ChatterjeeNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Boosting Indias Manufacturing Exports 140512Document25 pagesBoosting Indias Manufacturing Exports 140512Jayashree ChatterjeeNo ratings yet

- Intro ERP Using GBI SAP Slides en v2.20Document14 pagesIntro ERP Using GBI SAP Slides en v2.20Jayashree ChatterjeeNo ratings yet

- CIL Sample Questions MT2012 05072012Document8 pagesCIL Sample Questions MT2012 05072012Jayashree ChatterjeeNo ratings yet

- SAP IntroductionDocument27 pagesSAP Introductiongundala_thejokarthikNo ratings yet

- Methods To Initiate Ventures: Leoncio, Ma. Aira Grabrielle R. Mamigo, Princess Nicole B. G12-AB126Document21 pagesMethods To Initiate Ventures: Leoncio, Ma. Aira Grabrielle R. Mamigo, Princess Nicole B. G12-AB126Precious MamigoNo ratings yet

- Indian Economic Social History Review-1979-Henningham-53-75Document24 pagesIndian Economic Social History Review-1979-Henningham-53-75Dipankar MishraNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Test Bank For Entrepreneurship The Art Science and Process For Success 3rd Edition Charles Bamford Garry BrutonDocument15 pagesTest Bank For Entrepreneurship The Art Science and Process For Success 3rd Edition Charles Bamford Garry Brutonsaleburrock1srNo ratings yet

- Shantilal Shah Engineering College, Bhavnagar: Submission of Proposal For Project/ModelDocument7 pagesShantilal Shah Engineering College, Bhavnagar: Submission of Proposal For Project/Modelparth patelNo ratings yet

- Economic Engineering - Inflation - Lectures 1&2Document66 pagesEconomic Engineering - Inflation - Lectures 1&21k subs with no videos challengeNo ratings yet

- IET Educational (Xiao-Ping Zhang)Document17 pagesIET Educational (Xiao-Ping Zhang)Mayita ContrerasNo ratings yet

- Grammar Vocabulary 1star Unit7 PDFDocument1 pageGrammar Vocabulary 1star Unit7 PDFLorenaAbreuNo ratings yet

- L12022 Laser Cutter Flyer SinglesDocument4 pagesL12022 Laser Cutter Flyer SinglesPablo Marcelo Garnica TejerinaNo ratings yet

- Acctg 1 PS 1Document3 pagesAcctg 1 PS 1Aj GuanzonNo ratings yet

- KFC Offer T&C: SL - No Outlet Name CityDocument16 pagesKFC Offer T&C: SL - No Outlet Name Cityanita rajenNo ratings yet

- MNCDocument25 pagesMNCPiyush SoniNo ratings yet

- Borjas 2013 Power Point Chapter 8Document36 pagesBorjas 2013 Power Point Chapter 8Shahirah Hafit0% (1)

- Dummy VariableDocument21 pagesDummy VariableMuhammad MudassirNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- ForEx Hidden SystemsDocument123 pagesForEx Hidden SystemsWar Prince100% (2)

- Social Integration Approaches and Issues, UNRISD Publication (1994)Document16 pagesSocial Integration Approaches and Issues, UNRISD Publication (1994)United Nations Research Institute for Social DevelopmentNo ratings yet

- Certificate - BG. MARINE POWER 3028 - TB. KIETRANS 23Document3 pagesCertificate - BG. MARINE POWER 3028 - TB. KIETRANS 23Habibie MikhailNo ratings yet

- Chap 3 MCDocument29 pagesChap 3 MCIlyas SadvokassovNo ratings yet

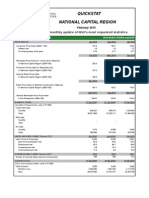

- Quickstat National Capital Region: A Monthly Update of NSO's Most Requested StatisticsDocument3 pagesQuickstat National Capital Region: A Monthly Update of NSO's Most Requested StatisticsDaniel John Cañares LegaspiNo ratings yet

- 0413 Germany Yapp PDFDocument9 pages0413 Germany Yapp PDFBharatNo ratings yet

- Real Estate Player in BangaloreDocument20 pagesReal Estate Player in BangaloreAnkit GoelNo ratings yet

- Abu Dhabi EstidamaDocument63 pagesAbu Dhabi Estidamagolashdi100% (3)

- Carbon Footprint CalculatorDocument1 pageCarbon Footprint CalculatorLadylee AcuñaNo ratings yet

- IGCSE Economics U1 AnsDocument4 pagesIGCSE Economics U1 AnsChristy SitNo ratings yet

- 18 043Document3 pages18 043cah7rf9099No ratings yet

- Daniela Del Bene e Kesang ThakurDocument23 pagesDaniela Del Bene e Kesang ThakurYara CerpaNo ratings yet

- © 2019 TOKOIN. All Rights ReservedDocument47 pages© 2019 TOKOIN. All Rights ReservedPutra KongkeksNo ratings yet

- Globalization and The Sociology of Immanuel Wallerstein: A Critical AppraisalDocument23 pagesGlobalization and The Sociology of Immanuel Wallerstein: A Critical AppraisalMario__7No ratings yet

- Woodward Life Cycle CostingDocument10 pagesWoodward Life Cycle CostingmelatorNo ratings yet

- AIRTITEDocument2 pagesAIRTITEMuhammad AtifNo ratings yet

- Model Sale AgreementDocument4 pagesModel Sale AgreementNagaraj KumbleNo ratings yet

- Summary of The Anxious Generation by Jonathan Haidt: How the Great Rewiring of Childhood Is Causing an Epidemic of Mental IllnessFrom EverandSummary of The Anxious Generation by Jonathan Haidt: How the Great Rewiring of Childhood Is Causing an Epidemic of Mental IllnessNo ratings yet

- The Compound Effect by Darren Hardy - Book Summary: Jumpstart Your Income, Your Life, Your SuccessFrom EverandThe Compound Effect by Darren Hardy - Book Summary: Jumpstart Your Income, Your Life, Your SuccessRating: 5 out of 5 stars5/5 (456)

- The One Thing: The Surprisingly Simple Truth Behind Extraordinary ResultsFrom EverandThe One Thing: The Surprisingly Simple Truth Behind Extraordinary ResultsRating: 4.5 out of 5 stars4.5/5 (709)

- Can't Hurt Me by David Goggins - Book Summary: Master Your Mind and Defy the OddsFrom EverandCan't Hurt Me by David Goggins - Book Summary: Master Your Mind and Defy the OddsRating: 4.5 out of 5 stars4.5/5 (383)

- The Body Keeps the Score by Bessel Van der Kolk, M.D. - Book Summary: Brain, Mind, and Body in the Healing of TraumaFrom EverandThe Body Keeps the Score by Bessel Van der Kolk, M.D. - Book Summary: Brain, Mind, and Body in the Healing of TraumaRating: 4.5 out of 5 stars4.5/5 (266)

- Summary: Atomic Habits by James Clear: An Easy & Proven Way to Build Good Habits & Break Bad OnesFrom EverandSummary: Atomic Habits by James Clear: An Easy & Proven Way to Build Good Habits & Break Bad OnesRating: 5 out of 5 stars5/5 (1635)