You might also like

- Circular Letter: Republic of The PhilippinesDocument2 pagesCircular Letter: Republic of The Philippinesapi-247793055No ratings yet

- Bureau of Internal Revenue: Revenue vs. Michel J. Lhuillier Pawnshop, Inc. (G.R. No. 150947), Declared RevenueDocument1 pageBureau of Internal Revenue: Revenue vs. Michel J. Lhuillier Pawnshop, Inc. (G.R. No. 150947), Declared Revenueapi-247793055No ratings yet

- Bureau of Internal Revenue: N-5 RBVDocument1 pageBureau of Internal Revenue: N-5 RBVapi-247793055No ratings yet

- Revenue Memorandum Circular No.: Bureau of Internal RevenueDocument2 pagesRevenue Memorandum Circular No.: Bureau of Internal Revenueapi-247793055No ratings yet

- Bureau of Internal RevenueDocument1 pageBureau of Internal Revenueapi-247793055No ratings yet

- RikksDocument1 pageRikksapi-247793055No ratings yet

- rikksDocument1 pagerikksapi-247793055No ratings yet

- 22 2004Document2 pages22 2004api-247793055No ratings yet

- Bureau of Internal Revenue: Republic of The Philippines Department of FinanceDocument1 pageBureau of Internal Revenue: Republic of The Philippines Department of Financeapi-247793055No ratings yet

- Bureau of Internal RevenueDocument14 pagesBureau of Internal Revenueapi-247793055No ratings yet

- Bureau of Internal RevenueDocument1 pageBureau of Internal Revenueapi-247793055No ratings yet

- Bureau of Internal Revenue: EducationalDocument2 pagesBureau of Internal Revenue: Educationalapi-247793055No ratings yet

- Bureau of Internal Revenue: Shall No Longer Be Assessed Nor Be Collected"Document2 pagesBureau of Internal Revenue: Shall No Longer Be Assessed Nor Be Collected"api-247793055No ratings yet

- rikksDocument1 pagerikksapi-247793055No ratings yet

- 09-2004 Banks and Non Banks Financial IntermediariesDocument4 pages09-2004 Banks and Non Banks Financial Intermediariesapi-247793055No ratings yet

- SubjectDocument2 pagesSubjectapi-247793055No ratings yet

- 10-2004 Gross Receipts TaxDocument3 pages10-2004 Gross Receipts Taxapi-247793055No ratings yet

- Bureau of Internal RevenueDocument1 pageBureau of Internal Revenueapi-247793055No ratings yet

- 02-2004 Vat Philippine Port Authority PpaDocument3 pages02-2004 Vat Philippine Port Authority Ppaapi-247793055No ratings yet

- Bureau of Internal RevenueDocument1 pageBureau of Internal Revenueapi-247793055No ratings yet

- Revenue Memorandum Circular No. 80-2003: Bureau of Internal RevenueDocument1 pageRevenue Memorandum Circular No. 80-2003: Bureau of Internal Revenueapi-247793055No ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- 05 - Ratio and ProportionDocument17 pages05 - Ratio and ProportionRupesh RoshanNo ratings yet

- GST - Unit 2 (Illustration Sums)Document10 pagesGST - Unit 2 (Illustration Sums)subash minecraft creatorNo ratings yet

- Trustee ObjectionDocument2 pagesTrustee ObjectionAnthony WarrenNo ratings yet

- Group Activity Mina HanDocument4 pagesGroup Activity Mina HanLevi's DishwasherNo ratings yet

- SyllabusDocument76 pagesSyllabusamattirkeyNo ratings yet

- Dabur NepalDocument19 pagesDabur Nepalbajracharyasandeep100% (1)

- Corporate Social Responsibility (CSR) As A Model of "Extended" Corporate Governance. An Explanation Based On The Economic Theories of Social Contract, Reputation and Reciprocal ConformismDocument49 pagesCorporate Social Responsibility (CSR) As A Model of "Extended" Corporate Governance. An Explanation Based On The Economic Theories of Social Contract, Reputation and Reciprocal ConformismronaqvNo ratings yet

- PSA 300 RedraftedDocument5 pagesPSA 300 RedraftedKenneth M. GonzalesNo ratings yet

- TicketsDocument1 pageTicketsYuvraj SinghNo ratings yet

- BURTON, The Roman Imperial State, Provincial Governors and The Public Finances of Provincial Cities, 27 B.C.-A.D. 235Document33 pagesBURTON, The Roman Imperial State, Provincial Governors and The Public Finances of Provincial Cities, 27 B.C.-A.D. 235seminariodigenovaNo ratings yet

- Tax Calculator FormulaDocument5 pagesTax Calculator FormulaKerwin Lester MandacNo ratings yet

- Template - Deed of Pledge - Shares of StocksDocument5 pagesTemplate - Deed of Pledge - Shares of StocksJerome FlojoNo ratings yet

- HWK - 6Document3 pagesHWK - 6Karen Nicole Lopez0% (1)

- Summary: Giving Up On The Reform of Administration and of Public Management, ContradictoryDocument18 pagesSummary: Giving Up On The Reform of Administration and of Public Management, ContradictorySergiu GanganNo ratings yet

- Canada Tax SetupDocument41 pagesCanada Tax SetupRajendran SureshNo ratings yet

- Deductions From Gross Income Part 2 Illustrative ProblemsDocument2 pagesDeductions From Gross Income Part 2 Illustrative ProblemsJohn Rich GamasNo ratings yet

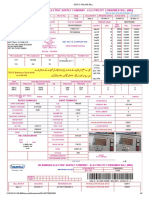

- Islamabad Electric Supply Company - Electricity Consumer Bill (Mdi)Document2 pagesIslamabad Electric Supply Company - Electricity Consumer Bill (Mdi)saleem khanNo ratings yet

- 519 986 1 SMDocument17 pages519 986 1 SMvenipin416No ratings yet

- Internal TradeDocument17 pagesInternal TradeUmesh PanchalNo ratings yet

- Up Taxation Law Reviewer 2017 PDFDocument267 pagesUp Taxation Law Reviewer 2017 PDFManny Aragones100% (3)

- Taxation Ii Atty. Deborah S. Acosta-Cajustin: Over But Not Over The Tax Shall Be Plus of The Excess OverDocument42 pagesTaxation Ii Atty. Deborah S. Acosta-Cajustin: Over But Not Over The Tax Shall Be Plus of The Excess OverRodel Cadorniga Jr.No ratings yet

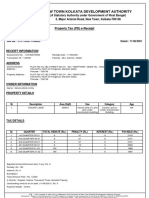

- New Town Kolkata Development Authority: Property Tax (PD) E-ReceiptDocument2 pagesNew Town Kolkata Development Authority: Property Tax (PD) E-ReceiptSSK DEVELOPERSNo ratings yet

- WEF Making Affordable Housing A Reality in Cities ReportDocument60 pagesWEF Making Affordable Housing A Reality in Cities ReportAnonymous XUFoDm6dNo ratings yet

- Maceda Vs ERBDocument13 pagesMaceda Vs ERBMargrein M. GreganaNo ratings yet

- Stamp PapersDocument2 pagesStamp PapersAyesha ChhatwalNo ratings yet

- Philex VS CirDocument2 pagesPhilex VS CirKath LeenNo ratings yet

- CARL ANDREW Assignment Tax 102Document7 pagesCARL ANDREW Assignment Tax 102Carl Andrew Aborquez Arcinal0% (1)

- Hindu Undivided Family (HUF) Tax Benefits: 1. What Is A HUF?Document4 pagesHindu Undivided Family (HUF) Tax Benefits: 1. What Is A HUF?ashankarNo ratings yet

- Declare WarDocument369 pagesDeclare Warvoip54301No ratings yet

- OD11944274478278000000Document1 pageOD11944274478278000000Kushal PatilNo ratings yet