You might also like

- Bucharest Offices H1 2009Document4 pagesBucharest Offices H1 2009avisitoronscribdNo ratings yet

- Markets from Networks: Socioeconomic Models of ProductionFrom EverandMarkets from Networks: Socioeconomic Models of ProductionRating: 3.5 out of 5 stars3.5/5 (2)

- Romania Off 4q18Document2 pagesRomania Off 4q18ririNo ratings yet

- JLL ONPOINT Brusselsofficemarketreport Q32015 FinalDocument15 pagesJLL ONPOINT Brusselsofficemarketreport Q32015 Finalwayne adjkqheNo ratings yet

- Q2 2023 Office ItalyDocument6 pagesQ2 2023 Office Italyabdalrahmananas45No ratings yet

- JLL MX Office Report Mexico City 3q 2022Document4 pagesJLL MX Office Report Mexico City 3q 20221234567qwertzuiNo ratings yet

- Colliers Manila Q2 2023 Office v2Document4 pagesColliers Manila Q2 2023 Office v2Daryl AngelesNo ratings yet

- Colliers Manila 2023 Outlook v1Document8 pagesColliers Manila 2023 Outlook v1Romeo ActaNo ratings yet

- Uk Ind 4q18Document1 pageUk Ind 4q18Nguyen SKThaiNo ratings yet

- Apartment For SaleDocument5 pagesApartment For SaleKeith Pang100% (2)

- Bulgaria Ind 4q18Document1 pageBulgaria Ind 4q18ririNo ratings yet

- City Office Market Watch: City Showed Significant Rental Growth During 2019 As A Result of Strong Take-Up and Low SupplyDocument3 pagesCity Office Market Watch: City Showed Significant Rental Growth During 2019 As A Result of Strong Take-Up and Low SupplytruefireNo ratings yet

- 435046d4-5191-435f-9312-7243ca0cd2a2-2815194897Document4 pages435046d4-5191-435f-9312-7243ca0cd2a2-2815194897Sirapob ChitmeesilpNo ratings yet

- Jakarta CBD Office Market OverviewDocument2 pagesJakarta CBD Office Market OverviewIda SetiyaningsihNo ratings yet

- 2Q20 Boston Industrial Market ReportDocument4 pages2Q20 Boston Industrial Market ReportWilliam HarrisNo ratings yet

- Bangalore - 1Q 2010Document1 pageBangalore - 1Q 2010seema_d_souzaNo ratings yet

- 2023 Q3 Office Houston Report ColliersDocument9 pages2023 Q3 Office Houston Report ColliersKevin ParkerNo ratings yet

- C&W India Real Estate Outlook 2009Document52 pagesC&W India Real Estate Outlook 2009rayvk18No ratings yet

- Colliers International MENA Real Estate Overview Q1 2010Document48 pagesColliers International MENA Real Estate Overview Q1 2010middleincomeNo ratings yet

- Real Estate Sector Case Study Highlights COVID Impact and Future TrendsDocument4 pagesReal Estate Sector Case Study Highlights COVID Impact and Future Trendsshubham sainiNo ratings yet

- 2023 Q4 Office Houston Report ColliersDocument9 pages2023 Q4 Office Houston Report ColliersKevin ParkerNo ratings yet

- Philadelphia Americas MarketBeat Office CBD Q32019 PDFDocument2 pagesPhiladelphia Americas MarketBeat Office CBD Q32019 PDFAnonymous zvbo2yJNo ratings yet

- Quarterly Houston Office ReportDocument9 pagesQuarterly Houston Office ReportKevin ParkerNo ratings yet

- Apartment For Sale: Ha Noi, Vietnam Q1/2009Document5 pagesApartment For Sale: Ha Noi, Vietnam Q1/2009hoangtungdang100% (1)

- PolAnd - IndusTRIAl REpoRT - Autumn 2009Document1 pagePolAnd - IndusTRIAl REpoRT - Autumn 2009cijblogNo ratings yet

- DoubleDragon revises 2020 plan and targetsDocument2 pagesDoubleDragon revises 2020 plan and targetsRodel Ryan YanaNo ratings yet

- CT National Report 2Q10Document16 pagesCT National Report 2Q10amy_schenkNo ratings yet

- Sixth of October Development Investment Co.-SODIC: Start Small Think BigDocument18 pagesSixth of October Development Investment Co.-SODIC: Start Small Think Bigmr_khaled85No ratings yet

- Q1:11 Baltimore: Transwestern OutlookDocument7 pagesQ1:11 Baltimore: Transwestern OutlookAnonymous Feglbx5No ratings yet

- Birla Real Estate Investor PresentationDocument19 pagesBirla Real Estate Investor Presentationakumar4uNo ratings yet

- Res RepDocument11 pagesRes Repwayne adjkqheNo ratings yet

- Industrial Market Report - 4Q23 - CBREDocument3 pagesIndustrial Market Report - 4Q23 - CBRErbfonseca96No ratings yet

- Pacific Corp to Acquire Monticello MillDocument3 pagesPacific Corp to Acquire Monticello MillDinhkhanh NguyenNo ratings yet

- NorthernNJ Q2 19Document2 pagesNorthernNJ Q2 19Anonymous R6r88UZFNo ratings yet

- Low Cost House ProjectDocument6 pagesLow Cost House ProjectAkum obenNo ratings yet

- Netherlands Marketbeat Office Q3 2021Document1 pageNetherlands Marketbeat Office Q3 2021sangoi_vipulNo ratings yet

- Colliers Market ResearchDocument6 pagesColliers Market ResearchMcke YapNo ratings yet

- Energy Conservation Building Directive - 2018 (Based On ECBC 2017)Document56 pagesEnergy Conservation Building Directive - 2018 (Based On ECBC 2017)shubham kumarNo ratings yet

- Newmark Mexico City CDMX Office 2021 Q4Document5 pagesNewmark Mexico City CDMX Office 2021 Q41234567qwertzuiNo ratings yet

- Thailand Industrial Figures Q1 2022 - kyGODocument4 pagesThailand Industrial Figures Q1 2022 - kyGOMikeNo ratings yet

- Evolution of The TakeDocument2 pagesEvolution of The TakeAles SandroNo ratings yet

- Logistics Market View H22010Document6 pagesLogistics Market View H22010Bala Lakshmi NarayanaNo ratings yet

- Ciudad Juárez, Mexico: MarketbeatDocument2 pagesCiudad Juárez, Mexico: MarketbeatPepitofanNo ratings yet

- Romania Ind 4q18Document1 pageRomania Ind 4q18ririNo ratings yet

- Colliers Frankfurt Buerovermietung Investment 2023-q3Document2 pagesColliers Frankfurt Buerovermietung Investment 2023-q3anustasia789No ratings yet

- 9th June PPT Noida Functioning.V1Document48 pages9th June PPT Noida Functioning.V1R SinghNo ratings yet

- Yangon Real Estate Market Review 2015Document15 pagesYangon Real Estate Market Review 2015Semon AungNo ratings yet

- CASFLOWDocument133 pagesCASFLOWalenNo ratings yet

- HoustonDocument1 pageHoustonKevin ParkerNo ratings yet

- HoustonDocument1 pageHoustonKevin ParkerNo ratings yet

- HCMC Property Market Briefs Q2 2010 enDocument6 pagesHCMC Property Market Briefs Q2 2010 enVo Ngoc HanNo ratings yet

- Budapest Office Market: Vacancy StockDocument2 pagesBudapest Office Market: Vacancy StockIringo NovakNo ratings yet

- Romania Retail H1 2011Document3 pagesRomania Retail H1 2011avisitoronscribdNo ratings yet

- 2023 Q3 Fort+Bend Houston Report ColliersDocument2 pages2023 Q3 Fort+Bend Houston Report ColliersKevin ParkerNo ratings yet

- Assignment Nicmar PGCM 21Document19 pagesAssignment Nicmar PGCM 21punyadeep75% (4)

- Beijing: Capital Markets Q1 2020Document2 pagesBeijing: Capital Markets Q1 2020Trang PhanNo ratings yet

- 4Q19 Boston Life Science MarketDocument4 pages4Q19 Boston Life Science MarketKevin ParkerNo ratings yet

- Dha Phase 6Document74 pagesDha Phase 6munir HussainNo ratings yet

- BAMODocument4 pagesBAMOKevin ParkerNo ratings yet

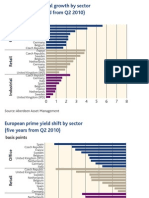

- Aberdeen Global Property Outlook 2010 ExtractDocument1 pageAberdeen Global Property Outlook 2010 ExtractcijblogNo ratings yet

- 10 09PL Listed DevDocument4 pages10 09PL Listed DevcijblogNo ratings yet

- Budapest Research Forum Releases Q1 Report On Local Office MarketDocument2 pagesBudapest Research Forum Releases Q1 Report On Local Office MarketallhungaryNo ratings yet

- PRF Q1 2010 Press Release enDocument2 pagesPRF Q1 2010 Press Release encijblogNo ratings yet

- Opg PR H1 2009Document10 pagesOpg PR H1 2009cijblogNo ratings yet

- PolAnd - IndusTRIAl REpoRT - Autumn 2009Document1 pagePolAnd - IndusTRIAl REpoRT - Autumn 2009cijblogNo ratings yet

- Euro SC Devt Report March 2010Document3 pagesEuro SC Devt Report March 2010cijblogNo ratings yet

- Euro SC Devt Report March 2010Document3 pagesEuro SC Devt Report March 2010cijblogNo ratings yet

- 120%on Point - Polish Office Market Forecast: Back To TheDocument1 page120%on Point - Polish Office Market Forecast: Back To ThecijblogNo ratings yet

- ProLogis' Committment To SustainabilityDocument3 pagesProLogis' Committment To SustainabilitycijblogNo ratings yet

- eCIJ September 2009Document64 pageseCIJ September 2009cijblogNo ratings yet

- DTZ WarsawSummer2 4Document3 pagesDTZ WarsawSummer2 4cijblogNo ratings yet

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Bratis Resi Pipeline 12 MonthDocument2 pagesBratis Resi Pipeline 12 MonthcijblogNo ratings yet

- Warimpex Sells Csalogany Office BuildingDocument2 pagesWarimpex Sells Csalogany Office BuildingcijblogNo ratings yet

- WarsawRetail JLLDocument1 pageWarsawRetail JLLcijblogNo ratings yet

- GST Introductory NotesDocument18 pagesGST Introductory NotesCA Ujjwal KumarNo ratings yet

- Vishal N Kalsaria Vs Bank of India and OrsDocument20 pagesVishal N Kalsaria Vs Bank of India and OrsSaumya badigineniNo ratings yet

- Rly QuaterssDocument13 pagesRly QuaterssVenkatesh RathodNo ratings yet

- CABALLES V DAR: Ruling that 60 sqm plot is too small to qualify as tenancyDocument80 pagesCABALLES V DAR: Ruling that 60 sqm plot is too small to qualify as tenancybee tifulNo ratings yet

- Case... Phuket Beach HotelDocument3 pagesCase... Phuket Beach HotelSanjay Kumar JainNo ratings yet

- GSIS Ordered to Sell Property to Original Owner for Agreed PriceDocument16 pagesGSIS Ordered to Sell Property to Original Owner for Agreed PricehenzencameroNo ratings yet

- Kel017 PDF Eng PDFDocument6 pagesKel017 PDF Eng PDFDuc NguyenNo ratings yet

- Capital OneDocument6 pagesCapital Oneapi-285064294No ratings yet

- 01 Income and Expenditure AccountDocument4 pages01 Income and Expenditure AccountPrateek ⎝⏠⏝⏠⎠ Gupta ヅ0% (1)

- Kyaw Ko - 10 21 E-Learning 7th GradeDocument2 pagesKyaw Ko - 10 21 E-Learning 7th GradeKyaw KoNo ratings yet

- PN 1213 FeaturesDocument32 pagesPN 1213 FeaturesSanthosh KrishnanNo ratings yet

- Booth Rental Agreement 2021-06-26Document4 pagesBooth Rental Agreement 2021-06-26Nicole Kathy Muncy LawsonNo ratings yet

- CONTRACT OF LEASE MangaserDocument2 pagesCONTRACT OF LEASE Mangasermary ann carreonNo ratings yet

- Ministop PhilippinesDocument6 pagesMinistop PhilippinesRonald Mcflurry100% (1)

- Hire Purchase-I Reducing Term TakafulDocument13 pagesHire Purchase-I Reducing Term Takafulanis suraya mohamed saidNo ratings yet

- Animal Friends Humane Society Complaint, Affidavits and ExhibitsDocument178 pagesAnimal Friends Humane Society Complaint, Affidavits and ExhibitsAmanda EvrardNo ratings yet

- Work Breakdown Structure - Example PDFDocument2 pagesWork Breakdown Structure - Example PDFMohammed Shebin0% (1)

- Landlord and Tenant To Be Printed 1Document55 pagesLandlord and Tenant To Be Printed 1aNo ratings yet

- Case Study FADocument15 pagesCase Study FAAshfaque Ul HaqueNo ratings yet

- Mohta Alloy and Steel Works Vs Mohta Finance and Leasing Co. Ltd. On 30 October, 1996Document7 pagesMohta Alloy and Steel Works Vs Mohta Finance and Leasing Co. Ltd. On 30 October, 1996Sukriti SinghNo ratings yet

- Definition of Commercial BuildingsDocument7 pagesDefinition of Commercial Buildingsarunachelam100% (1)

- India Motor Tariff GuideDocument222 pagesIndia Motor Tariff GuidehhvkvujbkhihNo ratings yet

- Business Permit Application SummaryDocument4 pagesBusiness Permit Application SummaryMathenie DavidNo ratings yet

- Wesley Street 17, SouthportDocument2 pagesWesley Street 17, SouthportJames BradshawNo ratings yet

- 169 - Ariff v. Jadunath Majumdar (1235-1250)Document16 pages169 - Ariff v. Jadunath Majumdar (1235-1250)Surabhi SrinivasanNo ratings yet

- Claudio and Lydia Reyes V CaDocument2 pagesClaudio and Lydia Reyes V CaJan Jason Guerrero LumanagNo ratings yet

- Contract of LeaseDocument2 pagesContract of LeaseJerome Pasion FurioNo ratings yet

- 100A Application To Rent or LeaseDocument2 pages100A Application To Rent or LeaseHJBerejNo ratings yet

- Try Out 1 StanDocument6 pagesTry Out 1 StanEnda Al-KahfiNo ratings yet

- NecumentDocument3 pagesNecumentDekwerizNo ratings yet