You might also like

- Numerical Test - Exam EtstDocument117 pagesNumerical Test - Exam EtstMuhammad Zubair100% (10)

- Attock Refinery Limited: Hold Your Horses, Tough Time Not Over Yet!Document4 pagesAttock Refinery Limited: Hold Your Horses, Tough Time Not Over Yet!Muhammad ZubairNo ratings yet

- Lucky Cement Ltd. Detail Report WE Financial Services Ltd. August 2014Document11 pagesLucky Cement Ltd. Detail Report WE Financial Services Ltd. August 2014Muhammad ZubairNo ratings yet

- Economic Indicator Apri 2013 PakDocument5 pagesEconomic Indicator Apri 2013 PakMuhammad ZubairNo ratings yet

- Gender DifferencesDocument14 pagesGender DifferencesRaza MazharNo ratings yet

- Detecting Univariate and Multivariate OutliersDocument44 pagesDetecting Univariate and Multivariate Outliersestoy.registrando5852No ratings yet

- Int To Security AnalysisDocument50 pagesInt To Security AnalysisMuhammad ZubairNo ratings yet

- Abbott Pakistan Financial AnalysisDocument16 pagesAbbott Pakistan Financial AnalysisMuhammad ZubairNo ratings yet

- Security Analysis - Course OutlineDocument2 pagesSecurity Analysis - Course OutlineMuhammad ZubairNo ratings yet

- Int To Security AnalysisDocument50 pagesInt To Security AnalysisMuhammad ZubairNo ratings yet

- Celebrity EndorsementDocument8 pagesCelebrity EndorsementMuhammad ZubairNo ratings yet

- Term Report On AbbottDocument16 pagesTerm Report On Abbottmominansari80% (5)

- 11-Health and Nutrition of PakistanDocument9 pages11-Health and Nutrition of PakistanMuhammad ZubairNo ratings yet

- Financial Market - 2Document11 pagesFinancial Market - 2Muhammad ZubairNo ratings yet

- Effect of Celebrity Based Advertisements On The Purchase Attitude of Consumers Towards Durable ProductDocument15 pagesEffect of Celebrity Based Advertisements On The Purchase Attitude of Consumers Towards Durable ProductRizka Sarastri SumardionoNo ratings yet

- Alfalah ReportDocument6 pagesAlfalah ReportMuhammad ZubairNo ratings yet

- Capital BudgetingDocument20 pagesCapital BudgetingDheeraj100% (1)

- Economic Survey Pakistan 2013Document19 pagesEconomic Survey Pakistan 2013Fatima KhawajaNo ratings yet

- Starbucks Project Plan in IndiaDocument21 pagesStarbucks Project Plan in Indiadinkesh412No ratings yet

- Pharma Industry Report WHODocument56 pagesPharma Industry Report WHOMuhammad ZubairNo ratings yet

- Pakistan Socio Economy DataDocument26 pagesPakistan Socio Economy DataMuhammad ZubairNo ratings yet

- Abbott Financial RatiosDocument1 pageAbbott Financial RatiosMuhammad ZubairNo ratings yet

- Abbott Financial RatiosDocument1 pageAbbott Financial RatiosMuhammad ZubairNo ratings yet

- Sample Career Development Plan WorksheetDocument2 pagesSample Career Development Plan WorksheetMuhammad ZubairNo ratings yet

- Celebrity EndorsementDocument8 pagesCelebrity EndorsementMuhammad ZubairNo ratings yet

- Faysal Bank Financial Analysis 2013Document10 pagesFaysal Bank Financial Analysis 2013Muhammad ZubairNo ratings yet

- FMP ch01Document18 pagesFMP ch01Muhammad ZubairNo ratings yet

- Abbott Financial Report Analysis 2012Document85 pagesAbbott Financial Report Analysis 2012Muhammad Zubair50% (2)

- Sample Career Development Plan WorksheetDocument2 pagesSample Career Development Plan WorksheetMuhammad ZubairNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5784)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Directory GIAMM 2019Document241 pagesDirectory GIAMM 2019andri100% (1)

- Secretarial ManualDocument396 pagesSecretarial ManualOloo Yussuf Ochieng'100% (1)

- Presentation On PPP Seminar - Dr. Mustafa K. MujeriDocument21 pagesPresentation On PPP Seminar - Dr. Mustafa K. MujeriAnim InmolNo ratings yet

- Internship Report NiB BankDocument10 pagesInternship Report NiB BankAbdul WaheedNo ratings yet

- Venture Capital Firms in SoCalDocument4 pagesVenture Capital Firms in SoCalmcarney7100% (1)

- Principles of Taxation I SyllabusDocument7 pagesPrinciples of Taxation I SyllabusShreyaNo ratings yet

- CSC Memo Circ 26 & 26 A S. 1997 - 2Document3 pagesCSC Memo Circ 26 & 26 A S. 1997 - 2Bee Blanc100% (1)

- LION AIR E-TICKETDocument4 pagesLION AIR E-TICKETIndrayani MonoarfaNo ratings yet

- India FMCG Review SU 6 June 2016Document12 pagesIndia FMCG Review SU 6 June 2016nnsriniNo ratings yet

- Annual Report 4Document156 pagesAnnual Report 4Sassy TanNo ratings yet

- United Parcel ServiceDocument16 pagesUnited Parcel ServiceDevin Fortranansi Firdaus0% (1)

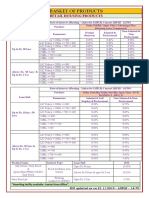

- BASKET OF RETAIL PRODUCTS RATESDocument3 pagesBASKET OF RETAIL PRODUCTS RATESVirendra K VermaNo ratings yet

- Money Market (Project)Document75 pagesMoney Market (Project)Prajakta Patil50% (10)

- SingaporeDocument1 pageSingaporeava1234567890No ratings yet

- Bulk SalesDocument2 pagesBulk SalesCris AnonuevoNo ratings yet

- KF Airline SimulationDocument10 pagesKF Airline SimulationMohsin Javed100% (2)

- Income TaxDocument14 pagesIncome Taxankit srivastavaNo ratings yet

- Shanghai General MotorDocument24 pagesShanghai General MotorHaninditaGuritna67% (3)

- Aditya Birla Nuvo Columbian ChemicalsDocument21 pagesAditya Birla Nuvo Columbian ChemicalssearchingnobodyNo ratings yet

- Reliance Group of Companies 2003Document22 pagesReliance Group of Companies 2003Aadil AslamNo ratings yet

- Fbe 532Document5 pagesFbe 532socalsurfyNo ratings yet

- Improved SEJDocument2 pagesImproved SEJHarjeetNo ratings yet

- DelinquencyDocument3 pagesDelinquencysujjuramu100% (1)

- Logos and Punchlines of Famous OrgnisationsDocument16 pagesLogos and Punchlines of Famous OrgnisationsAyan MitraNo ratings yet

- Module 33 - Related Party DisclosuresDocument60 pagesModule 33 - Related Party DisclosuresOdette ChavezNo ratings yet

- General Environment AnalysisDocument2 pagesGeneral Environment AnalysisClio Margaret CuevasNo ratings yet

- Credit Management at Janata BankDocument58 pagesCredit Management at Janata BankRubicon InternationalNo ratings yet

- CEO Road Rules1Document233 pagesCEO Road Rules1sammyyankee100% (1)

- Sbi, 1Q Fy 2014Document14 pagesSbi, 1Q Fy 2014Angel BrokingNo ratings yet