You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Sample Loan ProposalDocument20 pagesSample Loan Proposalhardmoneyteam94% (16)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- CSEC POA June 2012 P1 PDFDocument12 pagesCSEC POA June 2012 P1 PDFjunior subhanNo ratings yet

- Executive Assistant Office Manager in Washington DC Resume Jane GiordanoDocument2 pagesExecutive Assistant Office Manager in Washington DC Resume Jane GiordanoJaneGiordanoNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Effects of InflationDocument3 pagesEffects of InflationonenumbNo ratings yet

- Jim Cramers 10 Rules of InvestingDocument15 pagesJim Cramers 10 Rules of Investing2008cegs100% (2)

- The Accounting Process: Name: Date: Professor: Section: Score: QuizDocument6 pagesThe Accounting Process: Name: Date: Professor: Section: Score: QuizAllyna Jane Enriquez100% (1)

- Quiz 1 2Document4 pagesQuiz 1 2UndebaynNo ratings yet

- A Case Study of Luntian Multi-Purpose Cooperative in Barangay Lalaig, Tiaong, Quezon, Philippines: A Vertical Integration ApproachDocument8 pagesA Case Study of Luntian Multi-Purpose Cooperative in Barangay Lalaig, Tiaong, Quezon, Philippines: A Vertical Integration ApproachJedd Virgo100% (2)

- MT 199 Maribel Gonzalez 27 06 22Document2 pagesMT 199 Maribel Gonzalez 27 06 22ULRICH VOLLERNo ratings yet

- ABM - Culminating Activity - Business Enterprise Simulation CG - 2 PDFDocument4 pagesABM - Culminating Activity - Business Enterprise Simulation CG - 2 PDFAlfredo del Mundo Jr.80% (5)

- Intellectual Property AnalysisDocument3 pagesIntellectual Property AnalysisShradha DiwanNo ratings yet

- Patentability of MicroorganismsDocument4 pagesPatentability of MicroorganismsShradha DiwanNo ratings yet

- Non Conventional TrademarksDocument7 pagesNon Conventional TrademarksShradha DiwanNo ratings yet

- Incredible IndiaDocument13 pagesIncredible IndiaShradha DiwanNo ratings yet

- Global Financial Crisis and Its Impact On The Indian EconomyDocument42 pagesGlobal Financial Crisis and Its Impact On The Indian EconomyShradha Diwan95% (19)

- MBA Syllabus 21-08-2020 FinalDocument160 pagesMBA Syllabus 21-08-2020 Finalgundarapu deepika0% (1)

- Avoiding Fraudulent TransfersDocument8 pagesAvoiding Fraudulent TransfersNamamm fnfmfdnNo ratings yet

- White County Lilly Endowment Scholarship ApplicationDocument11 pagesWhite County Lilly Endowment Scholarship ApplicationVoodooPandasNo ratings yet

- JKH 2015 2016 Low 1Document304 pagesJKH 2015 2016 Low 1Rufus LintonNo ratings yet

- Central Bank: The Guardian of CurrencyDocument6 pagesCentral Bank: The Guardian of CurrencyBe YourselfNo ratings yet

- REO CPA Review: Business CombinationDocument9 pagesREO CPA Review: Business CombinationRoldan Hiano ManganipNo ratings yet

- Pontoon PLC A Case StudyDocument6 pagesPontoon PLC A Case Studyparthasarathi_inNo ratings yet

- Mba 410: Commercial Banking Credit Units: 03 Course ObjectivesDocument6 pagesMba 410: Commercial Banking Credit Units: 03 Course ObjectivesakmohideenNo ratings yet

- Proposal 2017Document29 pagesProposal 2017Faysal100% (1)

- Excel Drill - CAPM & WACCDocument8 pagesExcel Drill - CAPM & WACCgjlastimozaNo ratings yet

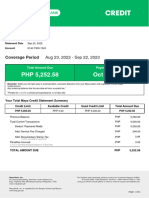

- MayaCredit SoA 2023SEPDocument3 pagesMayaCredit SoA 2023SEPjepoy palaruanNo ratings yet

- 12 Asian Cathay Finance V Sps Gravador and de VeraDocument9 pages12 Asian Cathay Finance V Sps Gravador and de VeraAnne VallaritNo ratings yet

- Vinati OrganicsDocument6 pagesVinati OrganicsNeha NehaNo ratings yet

- Chapter 17 Solutions V1Document23 pagesChapter 17 Solutions V1Badar MunirNo ratings yet

- Golden Rules of AccountingDocument5 pagesGolden Rules of AccountingVinay ChintamaneniNo ratings yet

- Unifi Capital PresentationDocument40 pagesUnifi Capital PresentationAnkurNo ratings yet

- New Zealand 2009 Financial Knowledge SurveyDocument11 pagesNew Zealand 2009 Financial Knowledge SurveywmhuthnanceNo ratings yet

- Financial Institutions 11Document13 pagesFinancial Institutions 11Afshan ShehzadiNo ratings yet

- Payroll Management SystemDocument8 pagesPayroll Management SystemMayur Jondhale MJNo ratings yet

- Income Tax and VATDocument498 pagesIncome Tax and VATshankar k.c.100% (2)