You might also like

- Update 9 28 00Document7 pagesUpdate 9 28 00Committee For a Responsible Federal BudgetNo ratings yet

- Update 9 7 00Document2 pagesUpdate 9 7 00Committee For a Responsible Federal BudgetNo ratings yet

- Update 9 15 00Document6 pagesUpdate 9 15 00Committee For a Responsible Federal BudgetNo ratings yet

- The Cost of Current PolicyDocument8 pagesThe Cost of Current PolicyCommittee For a Responsible Federal BudgetNo ratings yet

- Update 6 16 98Document5 pagesUpdate 6 16 98Committee For a Responsible Federal BudgetNo ratings yet

- Update 1 31 01Document4 pagesUpdate 1 31 01Committee For a Responsible Federal BudgetNo ratings yet

- Facing The Fiscal CliffDocument4 pagesFacing The Fiscal Clifflps2001No ratings yet

- Sumsummary 8 7 00Document3 pagesSumsummary 8 7 00Committee For a Responsible Federal BudgetNo ratings yet

- ARRA BirthdayDocument9 pagesARRA BirthdayCommittee For a Responsible Federal BudgetNo ratings yet

- House Hearing, 112TH Congress - The Congressional Budget Office's Long-Term Budget OutlookDocument64 pagesHouse Hearing, 112TH Congress - The Congressional Budget Office's Long-Term Budget OutlookScribd Government DocsNo ratings yet

- SMH 23jul18Document5 pagesSMH 23jul18John GriffithNo ratings yet

- Livingston County Adopted Budget (2023)Document401 pagesLivingston County Adopted Budget (2023)Watertown Daily TimesNo ratings yet

- Wrapup 12 27 00Document3 pagesWrapup 12 27 00Committee For a Responsible Federal BudgetNo ratings yet

- C R F B: Ommittee For A Esponsible Ederal UdgetDocument3 pagesC R F B: Ommittee For A Esponsible Ederal UdgetCommittee For a Responsible Federal BudgetNo ratings yet

- The Legacy of The 2001 and 2003 Bush Tax CutsDocument5 pagesThe Legacy of The 2001 and 2003 Bush Tax CutsHernán MontealegreNo ratings yet

- Update 2 28 01Document9 pagesUpdate 2 28 01Committee For a Responsible Federal BudgetNo ratings yet

- House Hearing, 110TH Congress - Department of Health and Human Services Fiscal Year 2008 Budget RequestDocument56 pagesHouse Hearing, 110TH Congress - Department of Health and Human Services Fiscal Year 2008 Budget RequestScribd Government DocsNo ratings yet

- Healthcare BillDocument3 pagesHealthcare Billtony_lima_2No ratings yet

- Five Myths About The Bush Tax CutsDocument2 pagesFive Myths About The Bush Tax CutsHernán MontealegreNo ratings yet

- Biden Tax Plan Would Raise $1.5 Trillion From The WealthyDocument9 pagesBiden Tax Plan Would Raise $1.5 Trillion From The WealthysiesmannNo ratings yet

- ff321 0Document4 pagesff321 0Jennifer PeeblesNo ratings yet

- Labor Markets and Health Care Refor M: New Results: Executive SummaryDocument6 pagesLabor Markets and Health Care Refor M: New Results: Executive Summaryapi-27836025No ratings yet

- Productividad y Salarios RealesDocument41 pagesProductividad y Salarios RealesavallebNo ratings yet

- WFP MemoDocument3 pagesWFP MemoJimmyVielkindNo ratings yet

- Update 3 22 01Document6 pagesUpdate 3 22 01Committee For a Responsible Federal BudgetNo ratings yet

- Federal Deficits and DebtDocument10 pagesFederal Deficits and DebtSiddhantNo ratings yet

- CBO2 Feb 2008Document4 pagesCBO2 Feb 2008Committee For a Responsible Federal BudgetNo ratings yet

- Westminster MiGa Neg Kentucky Round 4Document39 pagesWestminster MiGa Neg Kentucky Round 4EmronNo ratings yet

- No, The US Is Not Greece: June 27, 2011 630-517-7756Document1 pageNo, The US Is Not Greece: June 27, 2011 630-517-7756Roger LingleNo ratings yet

- Fairness Fees PaperDocument8 pagesFairness Fees PaperRachel SilbersteinNo ratings yet

- Stimulus Contractors Who Cheat On Their Taxes: What Happened?Document98 pagesStimulus Contractors Who Cheat On Their Taxes: What Happened?Scribd Government DocsNo ratings yet

- 05 - 14 - 2020 CRF Mills Delegation LetterDocument4 pages05 - 14 - 2020 CRF Mills Delegation LetterNEWS CENTER MaineNo ratings yet

- CRFB Reacts To The Paul Ryan Budget Proposal April 5, 2011: HairmenDocument4 pagesCRFB Reacts To The Paul Ryan Budget Proposal April 5, 2011: HairmenCommittee For a Responsible Federal BudgetNo ratings yet

- C R F B: Ommittee For A Esponsible Ederal UdgetDocument1 pageC R F B: Ommittee For A Esponsible Ederal UdgetCommittee For a Responsible Federal BudgetNo ratings yet

- Shifting Responsibility: How 50 Years of Tax Cuts Benefited The Wealthiest AmericansDocument14 pagesShifting Responsibility: How 50 Years of Tax Cuts Benefited The Wealthiest AmericansStephen GrahamNo ratings yet

- Fiscal Challenges and The Economy in The Long Term: Hearing Committee On The Budget House of RepresentativesDocument54 pagesFiscal Challenges and The Economy in The Long Term: Hearing Committee On The Budget House of RepresentativesScribd Government DocsNo ratings yet

- Will Federal Health Legislation Cause The Deficit To SoarDocument2 pagesWill Federal Health Legislation Cause The Deficit To SoarthecynicaleconomistNo ratings yet

- Livingston County 2024 Proposed BudgetDocument395 pagesLivingston County 2024 Proposed BudgetThe Livingston County NewsNo ratings yet

- FIA TN Medicaid Expansion 111714Document9 pagesFIA TN Medicaid Expansion 111714FederalisminActionNo ratings yet

- PM - Slash Seize and SellDocument11 pagesPM - Slash Seize and SellAjah HalesNo ratings yet

- October, 2012: Propositions 30 & 38 in Context - California Funding For Public SchoolsDocument40 pagesOctober, 2012: Propositions 30 & 38 in Context - California Funding For Public Schoolsk12newsnetworkNo ratings yet

- Tax MythsDocument8 pagesTax MythsPatricia Carlson GuttaNo ratings yet

- Could Tax Reform Boost Business Investment and Job Creation?Document109 pagesCould Tax Reform Boost Business Investment and Job Creation?Scribd Government DocsNo ratings yet

- Quarterly Review and Outlook: Three Competing TheoriesDocument6 pagesQuarterly Review and Outlook: Three Competing TheoriesthickskinNo ratings yet

- BudgetDocument269 pagesBudgetRavi CharanNo ratings yet

- Reforming The Mortgage Interest DeductionDocument30 pagesReforming The Mortgage Interest DeductionMercatus Center at George Mason UniversityNo ratings yet

- Designing A Basic Income Guarantee For Canada-BROADWAY ET AL-qed - WP - 1371Document32 pagesDesigning A Basic Income Guarantee For Canada-BROADWAY ET AL-qed - WP - 1371william_V_LeeNo ratings yet

- Impact of Unemployment Compensation Fund InsolvencyDocument11 pagesImpact of Unemployment Compensation Fund InsolvencyAndy ChowNo ratings yet

- Senate Hearing, 109TH Congress - Exploring The Economics of RetirementDocument53 pagesSenate Hearing, 109TH Congress - Exploring The Economics of RetirementScribd Government DocsNo ratings yet

- The 99%'s Deficit Proposal - How To Create Jobs, Reduce The Wealth Divide and Control SpendingDocument23 pagesThe 99%'s Deficit Proposal - How To Create Jobs, Reduce The Wealth Divide and Control SpendingA.J. MacDonald, Jr.No ratings yet

- Lets Get Specific Health CareDocument9 pagesLets Get Specific Health CareCommittee For a Responsible Federal BudgetNo ratings yet

- Macro Effects of IRADocument21 pagesMacro Effects of IRAmuhammad.nm.abidNo ratings yet

- Immigration Not a Viable Fix for Social SecurityDocument85 pagesImmigration Not a Viable Fix for Social SecurityAlderon TyranNo ratings yet

- Citizens For Tax Justice: The Bush Tax Cuts Cost Two and A Half Times As Much As The House Democrats' Health Care ProposalDocument5 pagesCitizens For Tax Justice: The Bush Tax Cuts Cost Two and A Half Times As Much As The House Democrats' Health Care ProposalldelevingneNo ratings yet

- To Senator Richard Burr RobinDocument1 pageTo Senator Richard Burr Robinapi-242257811No ratings yet

- 2019.02.13 - Greg FischerDocument17 pages2019.02.13 - Greg FischerJonese FranklinNo ratings yet

- House Bills Would Add Billions To Debt Scuttle Medicare Cost Controls PDFDocument2 pagesHouse Bills Would Add Billions To Debt Scuttle Medicare Cost Controls PDFCommittee For a Responsible Federal BudgetNo ratings yet

- Fy16 Presidents Budget CRFB Slidedeck PDFDocument18 pagesFy16 Presidents Budget CRFB Slidedeck PDFCommittee For a Responsible Federal BudgetNo ratings yet

- CRFB JCT Response FINAL JS PDFDocument8 pagesCRFB JCT Response FINAL JS PDFCommittee For a Responsible Federal BudgetNo ratings yet

- Averting A Fiscal Crisis - Why America Needs Comprehensive Fiscal Reform Now 0 0 0 0 0 0 0 0Document53 pagesAverting A Fiscal Crisis - Why America Needs Comprehensive Fiscal Reform Now 0 0 0 0 0 0 0 0Committee For a Responsible Federal BudgetNo ratings yet

- CRFB JCT Response FINAL JS PDFDocument8 pagesCRFB JCT Response FINAL JS PDFCommittee For a Responsible Federal BudgetNo ratings yet

- Goldwein 09-10Document3 pagesGoldwein 09-10Committee For a Responsible Federal BudgetNo ratings yet

- CRFB JCT Response FINAL JS PDFDocument8 pagesCRFB JCT Response FINAL JS PDFCommittee For a Responsible Federal BudgetNo ratings yet

- Prepplan PDFDocument12 pagesPrepplan PDFCommittee For a Responsible Federal BudgetNo ratings yet

- CRFB On SGR Deal 3262014Document1 pageCRFB On SGR Deal 3262014Committee For a Responsible Federal BudgetNo ratings yet

- CRFB JCT Response FINAL JS PDFDocument8 pagesCRFB JCT Response FINAL JS PDFCommittee For a Responsible Federal BudgetNo ratings yet

- Reforming The Corporate Tax CodeDocument14 pagesReforming The Corporate Tax CodeCommittee For a Responsible Federal BudgetNo ratings yet

- CRFB JCT Response FINAL JS PDFDocument8 pagesCRFB JCT Response FINAL JS PDFCommittee For a Responsible Federal BudgetNo ratings yet

- Averting A Fiscal Crisis 0Document26 pagesAverting A Fiscal Crisis 0Committee For a Responsible Federal BudgetNo ratings yet

- Averting A Fiscal Crisis - Why America Needs Comprehensive Fiscal Reform Now 0 0 0 0 0 0 0Document60 pagesAverting A Fiscal Crisis - Why America Needs Comprehensive Fiscal Reform Now 0 0 0 0 0 0 0Committee For a Responsible Federal Budget100% (1)

- Averting A Fiscal Crisis - Why America Needs Comprehensive Fiscal Reform Now 0 0 0 0 0 0Document59 pagesAverting A Fiscal Crisis - Why America Needs Comprehensive Fiscal Reform Now 0 0 0 0 0 0Committee For a Responsible Federal BudgetNo ratings yet

- CRFB Reacts To OMBs Report On The SequesterDocument1 pageCRFB Reacts To OMBs Report On The SequesterCommittee For a Responsible Federal BudgetNo ratings yet

- CRFB Reacts To Six-Month Continuing Resolution 9-11-2012Document1 pageCRFB Reacts To Six-Month Continuing Resolution 9-11-2012Committee For a Responsible Federal BudgetNo ratings yet

- Averting A Fiscal Crisis - Why America Needs Comprehensive Fiscal Reform Now 0 0 0 0 0 0Document59 pagesAverting A Fiscal Crisis - Why America Needs Comprehensive Fiscal Reform Now 0 0 0 0 0 0Committee For a Responsible Federal BudgetNo ratings yet

- Politco Fiscal Cliff Ad FinalDocument1 pagePolitco Fiscal Cliff Ad FinalCommittee For a Responsible Federal BudgetNo ratings yet

- With Conventions Out of The Way Its Time For Leaders To LeadDocument1 pageWith Conventions Out of The Way Its Time For Leaders To LeadCommittee For a Responsible Federal BudgetNo ratings yet

- CBO August 2012 Update 0Document6 pagesCBO August 2012 Update 0René Guerieri WoodNo ratings yet

- Averting A Fiscal Crisis 0Document26 pagesAverting A Fiscal Crisis 0Committee For a Responsible Federal BudgetNo ratings yet

- Paul Ryan TableDocument3 pagesPaul Ryan TableCommittee For a Responsible Federal BudgetNo ratings yet

- Averting A Fiscal Crisis - Why America Needs Comprehensive Fiscal Reform Now 0 0 0 0 0 0Document59 pagesAverting A Fiscal Crisis - Why America Needs Comprehensive Fiscal Reform Now 0 0 0 0 0 0Committee For a Responsible Federal BudgetNo ratings yet

- Americans Sign Debt Petition in One WeekDocument2 pagesAmericans Sign Debt Petition in One WeekCommittee For a Responsible Federal BudgetNo ratings yet

- Dont Put The Extenders On The Nations Credit CardDocument1 pageDont Put The Extenders On The Nations Credit CardCommittee For a Responsible Federal BudgetNo ratings yet

- Averting A Fiscal Crisis 0Document25 pagesAverting A Fiscal Crisis 0Committee For a Responsible Federal BudgetNo ratings yet

- Paul Ryan Comparison TableDocument3 pagesPaul Ryan Comparison TableCommittee For a Responsible Federal BudgetNo ratings yet

- Press Clips For Fix The Debt 8-13-2012Document7 pagesPress Clips For Fix The Debt 8-13-2012Committee For a Responsible Federal BudgetNo ratings yet

- Davis Steele Rendell Gregg Call For Debates On Debt ReductionDocument3 pagesDavis Steele Rendell Gregg Call For Debates On Debt ReductionCommittee For a Responsible Federal BudgetNo ratings yet

- PM Reyes Notes On Taxation 2 - Valued Added Tax (Working Draft)Document22 pagesPM Reyes Notes On Taxation 2 - Valued Added Tax (Working Draft)dodong123100% (1)

- CTC News December 2022Document16 pagesCTC News December 2022jeetNo ratings yet

- MCIAA vs. Lapu-LapuDocument3 pagesMCIAA vs. Lapu-LapukaiaceegeesNo ratings yet

- Notice: Health Insurance Portability and Accountability Act of 1996 Implementation: Taxpayer Advocacy PanelsDocument1 pageNotice: Health Insurance Portability and Accountability Act of 1996 Implementation: Taxpayer Advocacy PanelsJustia.comNo ratings yet

- Solved Citron Enters Into A Type C Restructuring With Ecru Ecru PDFDocument1 pageSolved Citron Enters Into A Type C Restructuring With Ecru Ecru PDFAnbu jaromiaNo ratings yet

- Chemalite Cash Flow StatementDocument2 pagesChemalite Cash Flow Statementrishika rshNo ratings yet

- 2013-2019 Iloilo City, Comprehensive Development PlanDocument39 pages2013-2019 Iloilo City, Comprehensive Development PlanJawo Jimenez60% (5)

- Bir Form 1904Document2 pagesBir Form 1904Kate Brzezinska50% (4)

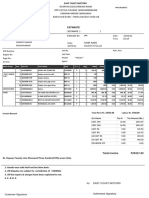

- Job Est PrintDocument1 pageJob Est PrintKashish JainNo ratings yet

- Chapter Four FundDocument13 pagesChapter Four FundnaodbrtiNo ratings yet

- Chemical Sector in IndiaDocument11 pagesChemical Sector in IndiaAatmprakash MishraNo ratings yet

- Forex WorksheetDocument2 pagesForex WorksheetTax Templates Inc.No ratings yet

- Angeles City Vs Angeles City Electric CorporationDocument1 pageAngeles City Vs Angeles City Electric CorporationJesse MoranteNo ratings yet

- Direct Tax Final Suggestion: For Offline Admission Call / Whatsapp - +91 70031 65955Document9 pagesDirect Tax Final Suggestion: For Offline Admission Call / Whatsapp - +91 70031 65955AhiaanNo ratings yet

- OECD International Academy For Tax Crime InvestigationDocument25 pagesOECD International Academy For Tax Crime InvestigationADBI EventsNo ratings yet

- Impact Rising Prices Petroleum Ethiopian EconomyDocument55 pagesImpact Rising Prices Petroleum Ethiopian EconomySomali BoyNo ratings yet

- Auckland Council Submission The Productivity CommissionDocument276 pagesAuckland Council Submission The Productivity CommissionBen RossNo ratings yet

- TibebuDEBRE MARDocument23 pagesTibebuDEBRE MARSentayehu GebeyehuNo ratings yet

- Service Tax Liability: Income To Purshottam Agarwal From LBF Publications, Admanum Packing & IndividualDocument6 pagesService Tax Liability: Income To Purshottam Agarwal From LBF Publications, Admanum Packing & Individualg26agarwalNo ratings yet

- Which of The Following Is The Correct Tax Implication of The Foregoing Data With Respect To Payment of Income Tax?Document3 pagesWhich of The Following Is The Correct Tax Implication of The Foregoing Data With Respect To Payment of Income Tax?ROSEMARIE CRUZNo ratings yet

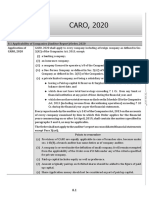

- Caro 2020 Main Book Pankaj GargDocument23 pagesCaro 2020 Main Book Pankaj Gargajay adhikariNo ratings yet

- 2022 Comprehensive Real Estate Property Due Diligence Checklist For Land SalesDocument4 pages2022 Comprehensive Real Estate Property Due Diligence Checklist For Land SalesLupang HinirangNo ratings yet

- State - A Community of Persons More or Less Numerous, Permanently Occupying A Definite Portion ofDocument7 pagesState - A Community of Persons More or Less Numerous, Permanently Occupying A Definite Portion ofRonna MaeNo ratings yet

- Internship ReportDocument62 pagesInternship ReportSejal TutejaNo ratings yet

- Nar Vol. 20 No. 2 CompleteDocument517 pagesNar Vol. 20 No. 2 CompleteAudreyNo ratings yet

- Strict or Liberal Construction of StatutesDocument32 pagesStrict or Liberal Construction of StatutesGreg BaldoveNo ratings yet

- PaymentDocument1 pagePaymentPepe PeprNo ratings yet

- Analysing India'S Lability For A Framework in Trade: SUBMITTED TO MR - Animesh Das, Assistant ProfessorDocument19 pagesAnalysing India'S Lability For A Framework in Trade: SUBMITTED TO MR - Animesh Das, Assistant ProfessorVishwaja RaoNo ratings yet

- Ford Motor Company Pestel & Environment AnalysisDocument3 pagesFord Motor Company Pestel & Environment AnalysisCHARALABOS LABROUNo ratings yet

- 1990 AMG Legal Systems Prototype Text From 1987 Criminal ConspiracyDocument242 pages1990 AMG Legal Systems Prototype Text From 1987 Criminal ConspiracyStan J. CaterboneNo ratings yet