You might also like

- Pawn Shop Revenues World Summary: Market Values & Financials by CountryFrom EverandPawn Shop Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- NPV Practice CompleteDocument5 pagesNPV Practice CompleteShakeel AslamNo ratings yet

- Financial Management and Control: Time Allowed 3 HoursDocument9 pagesFinancial Management and Control: Time Allowed 3 HoursnsarahnNo ratings yet

- 3.7 Strategic Financial Management (Old Syllabus) of ACCA Past Papers With Answers From2002-2006Document11 pages3.7 Strategic Financial Management (Old Syllabus) of ACCA Past Papers With Answers From2002-2006Sajid Ali100% (1)

- Assignment 3 20042023 103711pmDocument5 pagesAssignment 3 20042023 103711pmahmed aliNo ratings yet

- Annuity Tables p6Document17 pagesAnnuity Tables p6williammasvinuNo ratings yet

- F9FM Mock1 Qs - d08Document10 pagesF9FM Mock1 Qs - d08ErclanNo ratings yet

- Q and As-Corporate Financial Management - June 2010 Dec 2010 and June 2011Document71 pagesQ and As-Corporate Financial Management - June 2010 Dec 2010 and June 2011chisomo_phiri72290% (2)

- Assess Smart TV InvestmentDocument3 pagesAssess Smart TV InvestmentArka Narayan DashguptaNo ratings yet

- B Man 301112Document7 pagesB Man 301112dagodfadadadaNo ratings yet

- 2-4 2005 Jun QDocument10 pages2-4 2005 Jun QAjay TakiarNo ratings yet

- 3.7 Strategic Financial Management (Old Syllabus) of ACCA Past Papers With Answers From2002-2006Document11 pages3.7 Strategic Financial Management (Old Syllabus) of ACCA Past Papers With Answers From2002-2006Sajid Ali100% (1)

- Financial Management Tutorial QuestionsDocument8 pagesFinancial Management Tutorial QuestionsStephen Olieka100% (2)

- Benchmarking Bus Service EfficiencyDocument5 pagesBenchmarking Bus Service EfficiencyMevika MerchantNo ratings yet

- 3.7 Strategic Financial Management (Old Syllabus) of ACCA Past Papers With Answers From2002-2006Document12 pages3.7 Strategic Financial Management (Old Syllabus) of ACCA Past Papers With Answers From2002-2006Sajid Ali50% (2)

- 2.4 June 07 - QDocument9 pages2.4 June 07 - Qsameer_mobinNo ratings yet

- Cost Volume Profit Analysis For Paper 10Document6 pagesCost Volume Profit Analysis For Paper 10Zaira Anees100% (1)

- Financial Management: Thursday 9 June 2011Document9 pagesFinancial Management: Thursday 9 June 2011catcat1122No ratings yet

- ACCA Paper F5 Mock Exam June 2011Document6 pagesACCA Paper F5 Mock Exam June 2011Tasin Yeva LeoNo ratings yet

- Accounting-2009 Resit ExamDocument18 pagesAccounting-2009 Resit ExammasterURNo ratings yet

- f9 Paper 2012Document8 pagesf9 Paper 2012Shuja UmerNo ratings yet

- FDHDFGSGJHDFHDSHJDDocument8 pagesFDHDFGSGJHDFHDSHJDbabylovelylovelyNo ratings yet

- Financial Management NPV AnalysisDocument40 pagesFinancial Management NPV AnalysisErclan50% (2)

- Capital Budgeting 2 Homework SS 22Document2 pagesCapital Budgeting 2 Homework SS 22buivunguyetminhNo ratings yet

- Financial ManagementDocument5 pagesFinancial ManagementschawingaNo ratings yet

- P4 TestDocument4 pagesP4 TestSameed ArifNo ratings yet

- CVP Analysis Guide for ManagersDocument8 pagesCVP Analysis Guide for Managersw_sampathNo ratings yet

- 3.7 Strategic Financial Management (Old Syllabus) of ACCA Past Papers With Answers From2002-2006Document10 pages3.7 Strategic Financial Management (Old Syllabus) of ACCA Past Papers With Answers From2002-2006Sajid AliNo ratings yet

- FM202 - Exam Q - 2011-2 - Financial Accounting 202 V3 - AM NV DRdocDocument6 pagesFM202 - Exam Q - 2011-2 - Financial Accounting 202 V3 - AM NV DRdocMaxine IgnatiukNo ratings yet

- MAS311 Financial Management Exercises On Accounts Receivable Management and Inventory ManagementDocument3 pagesMAS311 Financial Management Exercises On Accounts Receivable Management and Inventory ManagementLeanne QuintoNo ratings yet

- Section A QUESTION 1 (Compulsory Question - 40 Marks)Document5 pagesSection A QUESTION 1 (Compulsory Question - 40 Marks)Jay Napstar NkomoNo ratings yet

- International Capital BudgetingDocument28 pagesInternational Capital BudgetingMatt ToothacreNo ratings yet

- 2-4 2003 Jun QDocument9 pages2-4 2003 Jun QAjay TakiarNo ratings yet

- BACC 232 -309-234 Assignment 1 (May-June 2024) (1)Document8 pagesBACC 232 -309-234 Assignment 1 (May-June 2024) (1)melinencube2002No ratings yet

- Capital Budgeting NPV Analysis for Earth Mover ProjectDocument6 pagesCapital Budgeting NPV Analysis for Earth Mover ProjectMarcoBonaparte0% (1)

- AccA P4/3.7 - 2002 - Dec - QDocument12 pagesAccA P4/3.7 - 2002 - Dec - Qroker_m3No ratings yet

- STRATEGIC FINANCIAL MANAGEMENT EXAMDocument21 pagesSTRATEGIC FINANCIAL MANAGEMENT EXAMCLIVENo ratings yet

- Return on Capital Employed Comparison for Two DivisionsDocument10 pagesReturn on Capital Employed Comparison for Two DivisionsWaqas Siddique SammaNo ratings yet

- Maximising Profits and Setting Optimal Price for Abel LtdDocument4 pagesMaximising Profits and Setting Optimal Price for Abel Ltdnicksilvester1991No ratings yet

- 3.7 Strategic Financial Management (Old Syllabus) of ACCA Past Papers With Answers From2002-2006Document12 pages3.7 Strategic Financial Management (Old Syllabus) of ACCA Past Papers With Answers From2002-2006Sajid AliNo ratings yet

- Dec 2006 - Qns Mod BDocument13 pagesDec 2006 - Qns Mod BHubbak Khan100% (2)

- 6002 Source Booklet January 2011Document12 pages6002 Source Booklet January 2011Sausan AliNo ratings yet

- Financial Decision Making - Sample Suggested AnswersDocument14 pagesFinancial Decision Making - Sample Suggested AnswersRaymond RayNo ratings yet

- WACC CALCULATIONSDocument4 pagesWACC CALCULATIONSshan50% (2)

- ABE Dip 1 - Financial Accounting JUNE 2005Document19 pagesABE Dip 1 - Financial Accounting JUNE 2005spinster40% (1)

- 3 1-2 - 2006 - Jun - Q.Document13 pages3 1-2 - 2006 - Jun - Q.Patricia DouceNo ratings yet

- Extra QDocument8 pagesExtra QdubzayNo ratings yet

- ACCA F9 Financial Management Solved Past Papers 2Document304 pagesACCA F9 Financial Management Solved Past Papers 2Daniel B Boy Nkrumah100% (1)

- Unit 4 - COST OF CAPITAL ActivityDocument5 pagesUnit 4 - COST OF CAPITAL ActivityCodyxanssNo ratings yet

- 2009-Management Accounting Main EQP and CommentariesDocument53 pages2009-Management Accounting Main EQP and CommentariesBryan Sing100% (1)

- Finance Pq1Document33 pagesFinance Pq1pakhok3No ratings yet

- Pyq Merge f9Document90 pagesPyq Merge f9Anonymous gdA3wqWcPNo ratings yet

- Capital Budgeting Practice QuestionsDocument6 pagesCapital Budgeting Practice QuestionsjezNo ratings yet

- FIN3101 Corporate Finance Practice Questions Topic: Capital BudgetingDocument3 pagesFIN3101 Corporate Finance Practice Questions Topic: Capital BudgetingKelly KohNo ratings yet

- Miscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryFrom EverandMiscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Consumer Lending Revenues World Summary: Market Values & Financials by CountryFrom EverandConsumer Lending Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Strategy, Value and Risk: A Guide to Advanced Financial ManagementFrom EverandStrategy, Value and Risk: A Guide to Advanced Financial ManagementNo ratings yet

- Sales Financing Revenues World Summary: Market Values & Financials by CountryFrom EverandSales Financing Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Automotive Glass Replacement Shop Revenues World Summary: Market Values & Financials by CountryFrom EverandAutomotive Glass Replacement Shop Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Sa Sept12 p5 BenchmarkingDocument9 pagesSa Sept12 p5 BenchmarkingIndra ThapaNo ratings yet

- Not-For-Profit: TechnicalDocument3 pagesNot-For-Profit: TechnicalMuntazir HussainNo ratings yet

- ACCA P4 Investment International.Document19 pagesACCA P4 Investment International.saeed_r2000422100% (1)

- D. Bahadur & Co. Chartered Accountants: Prepared By: Reviewed By: Approved byDocument31 pagesD. Bahadur & Co. Chartered Accountants: Prepared By: Reviewed By: Approved bysaeed_r2000422No ratings yet

- P2 May 2010 Answers PDFDocument14 pagesP2 May 2010 Answers PDFjoelvalentinorNo ratings yet

- F5 Mock 1 AnswerDocument14 pagesF5 Mock 1 Answersaeed_r2000422No ratings yet

- Cut and StichDocument1 pageCut and Stichsaeed_r2000422No ratings yet

- P2 Mar 2012 Exam PaperDocument16 pagesP2 Mar 2012 Exam Papermigueljorge007No ratings yet

- 2.4 Mock Exam Jun 06 Answer-AJ PDFDocument20 pages2.4 Mock Exam Jun 06 Answer-AJ PDFsaeed_r2000422No ratings yet

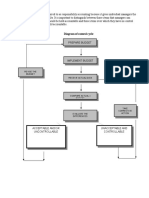

- Budgetary DiagramDocument1 pageBudgetary Diagramsaeed_r2000422No ratings yet

- AP Aging 2013 - AuditDocument1 pageAP Aging 2013 - Auditsaeed_r2000422No ratings yet

- Field Service Schedule 24-29Document2 pagesField Service Schedule 24-29saeed_r2000422No ratings yet

- Luke 12:42: w13 7/15 23 Par. 14Document3 pagesLuke 12:42: w13 7/15 23 Par. 14saeed_r2000422No ratings yet

- F5 Final Mock June 13Document7 pagesF5 Final Mock June 13saeed_r2000422No ratings yet

- Accounting & Business Connections (A.B.C) Expenses: Date Description Inv# AmtDocument2 pagesAccounting & Business Connections (A.B.C) Expenses: Date Description Inv# Amtsaeed_r2000422No ratings yet

- Accounting & Business Connections (A.B.C) Expenses: Date Description Inv# AmtDocument2 pagesAccounting & Business Connections (A.B.C) Expenses: Date Description Inv# Amtsaeed_r2000422No ratings yet

- Eron LallDocument4 pagesEron Lallsaeed_r2000422No ratings yet

- Cash PaymentDocument8 pagesCash Paymentsaeed_r2000422No ratings yet

- Bible HighlightsDocument1 pageBible Highlightssaeed_r2000422No ratings yet

- The Health and Fitness GroupDocument4 pagesThe Health and Fitness Groupsaeed_r2000422No ratings yet

- Ratiios SummaryDocument2 pagesRatiios Summarysaeed_r2000422No ratings yet

- LeDocument1 pageLesaeed_r2000422No ratings yet

- Budget QuizDocument1 pageBudget Quizsaeed_r2000422No ratings yet

- Country of GuyanaDocument3 pagesCountry of Guyanasaeed_r2000422No ratings yet

- Mock t7Document3 pagesMock t7saeed@atcNo ratings yet

- Mock Exam Dec 2013Document4 pagesMock Exam Dec 2013saeed_r2000422No ratings yet

- F5 ATC Pass Card 2012 PDFDocument102 pagesF5 ATC Pass Card 2012 PDFsaeed_r2000422100% (1)

- P3-Syll and SG 2013Document14 pagesP3-Syll and SG 2013Shazia PashaNo ratings yet

- 2.4 Mock Exam Jun 06 Answer-AJDocument20 pages2.4 Mock Exam Jun 06 Answer-AJsaeed_r2000422No ratings yet

- Basic Method For Making Economy Study NotesDocument3 pagesBasic Method For Making Economy Study NotesMichael DantogNo ratings yet

- Extinguishment of Obligations by Confusion and CompensationDocument38 pagesExtinguishment of Obligations by Confusion and CompensationMaicah Marie AlegadoNo ratings yet

- Aptivaa Model ManagementDocument18 pagesAptivaa Model Managementikhan809No ratings yet

- National Open University of Nigeria: Prepared byDocument17 pagesNational Open University of Nigeria: Prepared byMAVERICK MONROENo ratings yet

- Major Assignment #3Document17 pagesMajor Assignment #3Elijah GeniesseNo ratings yet

- Banking - HL - CBA 0979 - GOROKAN (01 Jan 23 - 28 Feb 23)Document5 pagesBanking - HL - CBA 0979 - GOROKAN (01 Jan 23 - 28 Feb 23)Adrianne JulianNo ratings yet

- Solutions To Exercises and Problems - Budgeting: GivenDocument8 pagesSolutions To Exercises and Problems - Budgeting: GivenTiến AnhNo ratings yet

- Rentberry Whitepaper enDocument59 pagesRentberry Whitepaper enKen Sidharta0% (1)

- Sanraa Annual Report 08 09Document49 pagesSanraa Annual Report 08 09chip_blueNo ratings yet

- KWP/ADV/2022/ Date: 14/04/2022: REF NO: BOB/KAWEMPE/ADV/2022-65 Dated 14/04/2022Document2 pagesKWP/ADV/2022/ Date: 14/04/2022: REF NO: BOB/KAWEMPE/ADV/2022-65 Dated 14/04/2022BalavinayakNo ratings yet

- Yodlee User Guide PDFDocument211 pagesYodlee User Guide PDFy2kmvrNo ratings yet

- Delhi Rent Control Act, 1958Document6 pagesDelhi Rent Control Act, 1958a-468951No ratings yet

- IRS Updates The 2021 Child Tax Credit and Advance Child Tax Credit Frequently Asked QuestionsDocument25 pagesIRS Updates The 2021 Child Tax Credit and Advance Child Tax Credit Frequently Asked QuestionsCrystal KleistNo ratings yet

- Fertilizer - Urea Offtake Update - AHLDocument3 pagesFertilizer - Urea Offtake Update - AHLmuddasir1980No ratings yet

- Chapter 6Document17 pagesChapter 6MM M83% (6)

- Prosper September 2020 Small Business SurveyDocument17 pagesProsper September 2020 Small Business SurveyStuff NewsroomNo ratings yet

- Tracking Market GammaDocument11 pagesTracking Market Gammadeepak777100% (1)

- Branch Banking CompleteDocument195 pagesBranch Banking Completesohail merchantNo ratings yet

- How George Soros Made $8 BillionDocument2 pagesHow George Soros Made $8 BillionAnanda rizky syifa nabilahNo ratings yet

- Ch.3 Size of BusinessDocument5 pagesCh.3 Size of BusinessRosina KaneNo ratings yet

- SAS® Financial Management 5.5 Formula GuideDocument202 pagesSAS® Financial Management 5.5 Formula Guidejohannadiaz87No ratings yet

- Revenue Recognition Guide for Telecom OperatorsDocument27 pagesRevenue Recognition Guide for Telecom OperatorsSaurabh MohanNo ratings yet

- Laporan Keuangan PT Duta Intidaya TBK (Watsons) Tahun 2018Document49 pagesLaporan Keuangan PT Duta Intidaya TBK (Watsons) Tahun 2018rahmaNo ratings yet

- Macro Economics and Economic Development of PakistanDocument3 pagesMacro Economics and Economic Development of PakistanWaqas AyubNo ratings yet

- Croissance Economique Taux Change Donnees Panel RegimesDocument326 pagesCroissance Economique Taux Change Donnees Panel RegimesSalah OuyabaNo ratings yet

- Medical Reimbursemen APPLICATION SETDocument5 pagesMedical Reimbursemen APPLICATION SETLeelakrishna GvNo ratings yet

- B7AF102 Financial Accounting May 2023Document11 pagesB7AF102 Financial Accounting May 2023gerlaniamelgacoNo ratings yet

- Coops CPPP Unit Vision Support Collectively Owned EnterprisesDocument17 pagesCoops CPPP Unit Vision Support Collectively Owned EnterprisesJeremy RakotomamonjyNo ratings yet

- Cooperative ManualDocument35 pagesCooperative ManualPratik MogheNo ratings yet

- Fresh Schedule 2021 (Online)Document280 pagesFresh Schedule 2021 (Online)Rumah Sakit khusus ibu dan anak annisa banjarmasinNo ratings yet