You might also like

- ECOMMERCE Unit 3Document195 pagesECOMMERCE Unit 3Urooj Alam FarooquiNo ratings yet

- E PaymentDocument15 pagesE PaymentRohan KirpekarNo ratings yet

- Ecommerce PresentationDocument9 pagesEcommerce PresentationSurabhi AgrawalNo ratings yet

- Electronic Payment SystemDocument47 pagesElectronic Payment SystemMilan Jain100% (1)

- Slow For Micro Payments and Produce High Transaction Costs For Processing Them. Therefore, New Processing Cost, and Widely AcceptableDocument10 pagesSlow For Micro Payments and Produce High Transaction Costs For Processing Them. Therefore, New Processing Cost, and Widely AcceptableAakash RegmiNo ratings yet

- A Review: Secure Payment System For Electronic TransactionDocument8 pagesA Review: Secure Payment System For Electronic Transactioneditor_ijarcsseNo ratings yet

- Chapter-6 Electronic Payment PDFDocument40 pagesChapter-6 Electronic Payment PDFSuman BhandariNo ratings yet

- E Commerce Notes Chapter 5-10Document5 pagesE Commerce Notes Chapter 5-10Taniya Bhalla100% (1)

- Electronic Payment SystemDocument20 pagesElectronic Payment SystemThe PaletteNo ratings yet

- Electronic Payment System: Presented By: Richa Somvanshi (85) Sachin Goel (68) Sahar AiromDocument43 pagesElectronic Payment System: Presented By: Richa Somvanshi (85) Sachin Goel (68) Sahar AiromSiti Zalikha Md JamilNo ratings yet

- E-Cash Report CSE SeminarDocument35 pagesE-Cash Report CSE Seminarz1230% (1)

- E-Business Unit 3Document5 pagesE-Business Unit 3Danny SathishNo ratings yet

- E - Payment and Security System MbaDocument5 pagesE - Payment and Security System MbaShwetaNo ratings yet

- E Marketing Unit 2 e ComDocument18 pagesE Marketing Unit 2 e ComjayNo ratings yet

- E COMMERCE FINAL COVERAGE MODULE 1 and 2Document9 pagesE COMMERCE FINAL COVERAGE MODULE 1 and 2BRIAN CORPUZ INCOGNITONo ratings yet

- E Money and e Payment System 1 1Document114 pagesE Money and e Payment System 1 1Aman SinghNo ratings yet

- E-Payment SystemDocument13 pagesE-Payment SystemDr. Azhar Ahmed SheikhNo ratings yet

- E Payments Modes and MethodsDocument52 pagesE Payments Modes and MethodsHarshithNo ratings yet

- Im Mini ProjectDocument10 pagesIm Mini Projectsrividya balajiNo ratings yet

- Ecommerce: EpaymentDocument8 pagesEcommerce: EpaymentJoseph ContehNo ratings yet

- Lecture 10Document21 pagesLecture 10Rehan UllahNo ratings yet

- On-Line Payment System Survey - EcashDocument9 pagesOn-Line Payment System Survey - EcashJournal of Mobile, Embedded and Distributed Systems (JMEDS)No ratings yet

- 1256450638lesson 3 - E-Commerce Payment SystemsDocument16 pages1256450638lesson 3 - E-Commerce Payment SystemsAvinash ShelkeNo ratings yet

- Electronic Payment System111Document43 pagesElectronic Payment System111negirakes100% (1)

- E-Commerce and Its Application: Unit-IVDocument37 pagesE-Commerce and Its Application: Unit-IVVasa VijayNo ratings yet

- Topic: Electronic Payment System. Group No.: 21 Name of The Members: Kirti Vardam 407 Roselene Jathana 408 Kirti Gorivale 409 Vaibhav Basutkar 410Document6 pagesTopic: Electronic Payment System. Group No.: 21 Name of The Members: Kirti Vardam 407 Roselene Jathana 408 Kirti Gorivale 409 Vaibhav Basutkar 410Kirti ParkNo ratings yet

- Electronic Business MaterialsDocument3 pagesElectronic Business Materialsally jumanneNo ratings yet

- CH-6 E MarketingDocument17 pagesCH-6 E Marketingabdelamuzemil8No ratings yet

- EC Assignment5 Dristy AdhikariDocument4 pagesEC Assignment5 Dristy AdhikariDristy AdhikariNo ratings yet

- Epayment SeminarDocument5 pagesEpayment Seminardheeraj_ddNo ratings yet

- E - Commerce Unit 2 RGPV SylabbusDocument22 pagesE - Commerce Unit 2 RGPV SylabbusDeepak Kumar RajakNo ratings yet

- Chapter 1Document89 pagesChapter 1Sachin chinnuNo ratings yet

- Electronic Payment Systems: Presented By: Salman Touheed Tariq Rashid Faizan ZafarDocument45 pagesElectronic Payment Systems: Presented By: Salman Touheed Tariq Rashid Faizan ZafarsalmantouheedNo ratings yet

- E PaymentDocument8 pagesE PaymentPrashant SinghNo ratings yet

- AttachmentDocument31 pagesAttachmentHambaNo ratings yet

- Unit Iv (Foit)Document48 pagesUnit Iv (Foit)varsha.j2177No ratings yet

- E - Business Unit-III, 2020Document15 pagesE - Business Unit-III, 2020Sourabh SoniNo ratings yet

- BBA-108 - E-Commerce Unit THREE & FOURDocument34 pagesBBA-108 - E-Commerce Unit THREE & FOURA1cyb CafeNo ratings yet

- E Payment SystemDocument56 pagesE Payment SystemAnkiTwilightedNo ratings yet

- E Payment 120927112113 Phpapp02Document38 pagesE Payment 120927112113 Phpapp02sagarg94gmailcomNo ratings yet

- UNIT 3 E-COMM NotesDocument13 pagesUNIT 3 E-COMM NotesVikash kumarNo ratings yet

- E-Comm 4Document14 pagesE-Comm 4Kanika GoelNo ratings yet

- E-Business AssignmentDocument21 pagesE-Business AssignmentYashi BokreNo ratings yet

- Communication BbaDocument33 pagesCommunication BbaParmeet KaurNo ratings yet

- Electronic Payment Systems-FinalDocument105 pagesElectronic Payment Systems-FinalDileep VkNo ratings yet

- E Payment SystemsDocument17 pagesE Payment SystemsdeekshaNo ratings yet

- Electronic Payment System Digital Cash, Plastic Card, PSO and PSP Sept 2023Document16 pagesElectronic Payment System Digital Cash, Plastic Card, PSO and PSP Sept 2023Meraj TalukderNo ratings yet

- Electronic Payment System: Presented byDocument43 pagesElectronic Payment System: Presented bysheetal28svNo ratings yet

- E Banking and E Payment - IsDocument20 pagesE Banking and E Payment - IsaliiiiNo ratings yet

- E CashDocument33 pagesE CashVijay Krishna BoppanaNo ratings yet

- Electronic Payment SystemDocument33 pagesElectronic Payment SystemGunjan JainNo ratings yet

- Unit-4 E-Commerce (PDF - Io) - 1Document6 pagesUnit-4 E-Commerce (PDF - Io) - 1rahuldodiyat001No ratings yet

- Electronic Payment SystemDocument23 pagesElectronic Payment SystemRonak Jain90% (10)

- Electronic Payment SystemDocument30 pagesElectronic Payment SystemSONAL RATHINo ratings yet

- Cyber Unit 2 Lecture 4Document21 pagesCyber Unit 2 Lecture 4VijayNo ratings yet

- Electronic Payment SystemDocument5 pagesElectronic Payment SystemSwati HansNo ratings yet

- EcashDocument33 pagesEcashapi-3746880No ratings yet

- Review of Some Online Banks and Visa/Master Cards IssuersFrom EverandReview of Some Online Banks and Visa/Master Cards IssuersNo ratings yet

- Evaluation of Some Online Payment Providers Services: Best Online Banks and Visa/Master Cards IssuersFrom EverandEvaluation of Some Online Payment Providers Services: Best Online Banks and Visa/Master Cards IssuersNo ratings yet

- Evaluation of Some Online Banks, E-Wallets and Visa/Master Card IssuersFrom EverandEvaluation of Some Online Banks, E-Wallets and Visa/Master Card IssuersNo ratings yet

- Indian Partnership Act 1932 Merged SlidesDocument62 pagesIndian Partnership Act 1932 Merged Slidestripti16No ratings yet

- Management Control: An OverviewDocument28 pagesManagement Control: An Overviewtripti16100% (1)

- Organized Sector in Indian Fast Food IndustryDocument24 pagesOrganized Sector in Indian Fast Food Industrytripti16No ratings yet

- Pearson1e PPT ch13Document19 pagesPearson1e PPT ch13tripti16No ratings yet

- Report On Merger of Bank of Baroda, Vijaya and Dena BankDocument6 pagesReport On Merger of Bank of Baroda, Vijaya and Dena BankAnkit KumarNo ratings yet

- Table of Service and Maintenance FeesDocument1 pageTable of Service and Maintenance FeesYt PremNo ratings yet

- Baylon Vs CADocument6 pagesBaylon Vs CAMj GarciaNo ratings yet

- Islamic Accounts (Flexcube)Document230 pagesIslamic Accounts (Flexcube)Ibrahim Y. Al QuqaNo ratings yet

- Aramco-GI Instruciton Manual PDFDocument12 pagesAramco-GI Instruciton Manual PDFRiaz ahmed100% (2)

- LEAVE SALARY CALCULATOR OF W.B.Govt EmployeesDocument13 pagesLEAVE SALARY CALCULATOR OF W.B.Govt EmployeesGourab SarkarNo ratings yet

- Statement of Account For The Period 01-Jun-2020 To 23-May-2021Document23 pagesStatement of Account For The Period 01-Jun-2020 To 23-May-2021Chandrakanth KhannaNo ratings yet

- Sap Fico SyllabusDocument7 pagesSap Fico SyllabusUsa IifcaNo ratings yet

- Petty Cash Recon PDFDocument1 pagePetty Cash Recon PDFCristy Martin YumulNo ratings yet

- Accounting Cash and Liquidity ManagementDocument19 pagesAccounting Cash and Liquidity ManagementMarsNo ratings yet

- 4 Petty Cash FundDocument13 pages4 Petty Cash FundAlyssa Barbara D. Badidles100% (1)

- Sales CasesDocument38 pagesSales CasesPrincess Cue Aragon100% (1)

- The Revenue Cycle: James A. HallDocument91 pagesThe Revenue Cycle: James A. HallAira Rhialyn MangubatNo ratings yet

- Banking Law Incl. Ni ActDocument3 pagesBanking Law Incl. Ni ActRaghu SharmaNo ratings yet

- IA1 Cash and Cash Equivalents 1Document5 pagesIA1 Cash and Cash Equivalents 1Steffanie OlivarNo ratings yet

- Business Account Statement: Account Summary For This PeriodDocument2 pagesBusiness Account Statement: Account Summary For This PeriodBrian TalentoNo ratings yet

- Consolidated Direct Deposit FormDocument2 pagesConsolidated Direct Deposit FormEmily HuangNo ratings yet

- Your Statement PDFDocument6 pagesYour Statement PDFpattiNo ratings yet

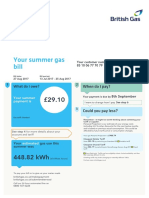

- BritishGas PDFDocument4 pagesBritishGas PDFpabenol847100% (1)

- Account Statement From 1 Apr 2019 To 8 May 2019: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument4 pagesAccount Statement From 1 Apr 2019 To 8 May 2019: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceArafath JazeebNo ratings yet

- Internship Report by Haileluel W PDFDocument18 pagesInternship Report by Haileluel W PDFSofonias MenberuNo ratings yet

- Quick Success Series - TechnologyDocument15 pagesQuick Success Series - TechnologySai Printers100% (1)

- Requirements For Offshore Banking License in BelizeDocument12 pagesRequirements For Offshore Banking License in BelizeBhagyanath MenonNo ratings yet

- DFI 211 HISTORY OF BANKING IN KENYA Presentation2-1Document35 pagesDFI 211 HISTORY OF BANKING IN KENYA Presentation2-1CatherineNo ratings yet

- Interpersonal Conflict 9th Edition Hocker Solutions ManualDocument25 pagesInterpersonal Conflict 9th Edition Hocker Solutions ManualJonathanLindseyizre100% (61)

- Online Challan For Admission BZU MultanDocument1 pageOnline Challan For Admission BZU MultanTayyab SaleemNo ratings yet

- Wa0006.Document32 pagesWa0006.Abhirami RNo ratings yet

- CB Module 3 Constructive AccountingDocument133 pagesCB Module 3 Constructive AccountingNiccolo Quintero Garcia100% (6)

- Yahvi Placida Booking FormDocument2 pagesYahvi Placida Booking FormAbeyNo ratings yet

- (Finance and Accounts)Document79 pages(Finance and Accounts)jorzfandnessNo ratings yet