You might also like

- How to Buy Bank-Owned Properties for Pennies on the Dollar: A Guide To REO Investing In Today's MarketFrom EverandHow to Buy Bank-Owned Properties for Pennies on the Dollar: A Guide To REO Investing In Today's MarketRating: 2.5 out of 5 stars2.5/5 (2)

- Construction Equipment Management BookDocument130 pagesConstruction Equipment Management BookJosse Shandra100% (9)

- Las Vegas Multifamily - Q1 2016Document18 pagesLas Vegas Multifamily - Q1 2016John McClelland100% (1)

- Advanced Accounting Vol.-IDocument792 pagesAdvanced Accounting Vol.-ISaibhumi80% (5)

- Third Point Q3 2019 Letter TPOIDocument13 pagesThird Point Q3 2019 Letter TPOImarketfolly.com100% (1)

- Self Storage - Covid 19 Report - FinalDocument8 pagesSelf Storage - Covid 19 Report - FinalKevin ParkerNo ratings yet

- ValueInvestorInsight Issue 284Document24 pagesValueInvestorInsight Issue 284kennethtsleeNo ratings yet

- Nabil ProfitabilityDocument44 pagesNabil Profitabilityabhishek shah100% (2)

- The Complete Guide to Passing Your Real Estate Sales License Exam On the First AttemptFrom EverandThe Complete Guide to Passing Your Real Estate Sales License Exam On the First AttemptRating: 1.5 out of 5 stars1.5/5 (3)

- LLQP Final Exam Ques PDFDocument57 pagesLLQP Final Exam Ques PDFRitesh Laller17% (6)

- Caltex Phils. vs. COA, G.R. No. 92585, May 8, 1992Document23 pagesCaltex Phils. vs. COA, G.R. No. 92585, May 8, 1992Machida AbrahamNo ratings yet

- Strategic Management Full NotesDocument137 pagesStrategic Management Full NotesAnishaAppuNo ratings yet

- Regulation A+ and Other Alternatives to a Traditional IPO: Financing Your Growth Business Following the JOBS ActFrom EverandRegulation A+ and Other Alternatives to a Traditional IPO: Financing Your Growth Business Following the JOBS ActNo ratings yet

- Starbucks PDFDocument14 pagesStarbucks PDFanimegod100% (1)

- Trump Staff Public Financial Disclosure - Cordish, Reed PDFDocument66 pagesTrump Staff Public Financial Disclosure - Cordish, Reed PDFMonte AltoNo ratings yet

- C R E R C: Ommercial Eal State E ApDocument2 pagesC R E R C: Ommercial Eal State E ApAnonymous Feglbx5No ratings yet

- CapWatch Sep10Document16 pagesCapWatch Sep10eric3645No ratings yet

- Occupational Employment Statistics (OES) Highlights Using Location Quotients To Analyze Occupational DataDocument13 pagesOccupational Employment Statistics (OES) Highlights Using Location Quotients To Analyze Occupational DataIndriNo ratings yet

- America's Fixer-Upper Housing MarketDocument2 pagesAmerica's Fixer-Upper Housing MarketkachizihNo ratings yet

- Official 2019 Rented ReportDocument28 pagesOfficial 2019 Rented ReportLuis Carlos KinnNo ratings yet

- Lockyer GoldmanDocument3 pagesLockyer GoldmanZerohedgeNo ratings yet

- RockFord Plaza For SaleDocument7 pagesRockFord Plaza For SaleabrealtyNo ratings yet

- Reg AlphaDocument4 pagesReg Alphaapi-98271862No ratings yet

- August 182010 PostsDocument273 pagesAugust 182010 PostsAlbert L. PeiaNo ratings yet

- Pro Hac Vice) Pro Hac Vice)Document7 pagesPro Hac Vice) Pro Hac Vice)Chapter 11 DocketsNo ratings yet

- Colliers 2009 Commercial Real Estate ReviewDocument79 pagesColliers 2009 Commercial Real Estate ReviewCTMT Research100% (8)

- Quepasa Corp 10K 20120314Document198 pagesQuepasa Corp 10K 20120314ybigalowNo ratings yet

- Printing Impressions 400 RankingDocument16 pagesPrinting Impressions 400 RankingFrancis ChastanetNo ratings yet

- Early Evidence On The Use of Foreign Cash Following The Tax Cuts and Jobs Act of 2017Document53 pagesEarly Evidence On The Use of Foreign Cash Following The Tax Cuts and Jobs Act of 2017GlennKesslerWPNo ratings yet

- Pre-Paid Legal Services Inc.: Expert Report OnDocument14 pagesPre-Paid Legal Services Inc.: Expert Report OnYang Ying ChanNo ratings yet

- 2021 Q2 Market Update WebDocument24 pages2021 Q2 Market Update WebDavid RanckNo ratings yet

- PEJIHOTAfilingsDocument28 pagesPEJIHOTAfilingsNanci MeekNo ratings yet

- Frankzen Altoona I-80 12 14 05Document1 pageFrankzen Altoona I-80 12 14 05Zach EdwardsNo ratings yet

- Harbor Point $107M Tax Deal Gets Final OK After Months of ControversyDocument3 pagesHarbor Point $107M Tax Deal Gets Final OK After Months of ControversyAnonymous Feglbx5No ratings yet

- T Rident: Municipal ResearchDocument4 pagesT Rident: Municipal Researchapi-244981307No ratings yet

- Small and Mid Cap Bank Opportunity Driven by Credit Cycle M&a Changing Regulatory Landscape FJ Capital White PaperDocument23 pagesSmall and Mid Cap Bank Opportunity Driven by Credit Cycle M&a Changing Regulatory Landscape FJ Capital White Paperajose1234No ratings yet

- CR 109Document24 pagesCR 109mpanczer6844No ratings yet

- Monarch Report 10/15/2012Document4 pagesMonarch Report 10/15/2012monarchadvisorygroupNo ratings yet

- Algae Dynamics Death Spiral Financing Announced by Chapter 7 Bankrupt NY Blinds InstallerDocument12 pagesAlgae Dynamics Death Spiral Financing Announced by Chapter 7 Bankrupt NY Blinds InstallerChris PineNo ratings yet

- Fortune 500 ListDocument12 pagesFortune 500 Listsunildubey02No ratings yet

- South Florida OfficeDocument1 pageSouth Florida OfficeKevin ParkerNo ratings yet

- T Rident: Municipal ResearchDocument4 pagesT Rident: Municipal Researchapi-245850635No ratings yet

- SingleDocument12 pagesSinglenetleaseNo ratings yet

- Managing Member - Tim Eriksen Eriksen Capital Management, LLC 567 Wildrose Cir., Lynden, WA 98264Document6 pagesManaging Member - Tim Eriksen Eriksen Capital Management, LLC 567 Wildrose Cir., Lynden, WA 98264Matt EbrahimiNo ratings yet

- House Hearing, 112TH Congress - An Examination of The Federal Housing Finance Agency's Real Estate Owned (Reo) Pilot ProgramDocument115 pagesHouse Hearing, 112TH Congress - An Examination of The Federal Housing Finance Agency's Real Estate Owned (Reo) Pilot ProgramScribd Government DocsNo ratings yet

- Yhoo 4Q06Document8 pagesYhoo 4Q06Brian BolanNo ratings yet

- Smarte Trader February 11 2016 PDFDocument10 pagesSmarte Trader February 11 2016 PDFThinh DoNo ratings yet

- Daily Market Script 2017Document111 pagesDaily Market Script 2017JitkaSamakNo ratings yet

- The Weekly Peak: Peak Theories Research LLCDocument5 pagesThe Weekly Peak: Peak Theories Research LLCZerohedgeNo ratings yet

- Third Point Q3 LetterDocument8 pagesThird Point Q3 LetterZerohedgeNo ratings yet

- Hearing: Reducing Barriers To Capital Formation, Part IiDocument84 pagesHearing: Reducing Barriers To Capital Formation, Part IiScribd Government DocsNo ratings yet

- Current Economic Conditions: Summary of Commentary OnDocument47 pagesCurrent Economic Conditions: Summary of Commentary Onapi-25887578No ratings yet

- Maran Partners Fund Q2 2020Document6 pagesMaran Partners Fund Q2 2020Paul AsselinNo ratings yet

- Best Multifamily Markets Right NowDocument6 pagesBest Multifamily Markets Right NownicollegvraNo ratings yet

- ForbesDocument24 pagesForbesapi-330066158No ratings yet

- Registration by Thorn Run Partners To Lobby For Timothy R. Rupli & Associates, Inc. (300305059)Document2 pagesRegistration by Thorn Run Partners To Lobby For Timothy R. Rupli & Associates, Inc. (300305059)Sunlight FoundationNo ratings yet

- Registration by GPC Associates LLC To Lobby For Elliott Management Corporation (300328909)Document3 pagesRegistration by GPC Associates LLC To Lobby For Elliott Management Corporation (300328909)Sunlight FoundationNo ratings yet

- San Diego CADocument3 pagesSan Diego CAddjusaNo ratings yet

- CRE Transaction Rise 16% in First Half of 2014: October 25th - November 7th, 2014Document2 pagesCRE Transaction Rise 16% in First Half of 2014: October 25th - November 7th, 2014Anonymous Feglbx5No ratings yet

- Lahore Smart CityDocument2 pagesLahore Smart CitychatroomvistaNo ratings yet

- Registration by Barbour Griffith & Rogers, LLC D/b/a BGR Government Affairs To Lobby For Freedom Capital Partners, LLC (300232977)Document2 pagesRegistration by Barbour Griffith & Rogers, LLC D/b/a BGR Government Affairs To Lobby For Freedom Capital Partners, LLC (300232977)Sunlight FoundationNo ratings yet

- Midyear Report 2008Document5 pagesMidyear Report 2008Missouri Netizen NewsNo ratings yet

- Registration by SNR DENTON LLP (Fka Sonnenschein Nath and Rosenthal) To Lobby For YKK Corporation of America (300319026)Document3 pagesRegistration by SNR DENTON LLP (Fka Sonnenschein Nath and Rosenthal) To Lobby For YKK Corporation of America (300319026)Sunlight FoundationNo ratings yet

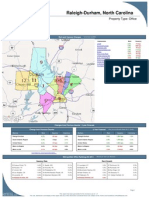

- Raleigh-Durham, North Carolina: Property Type: OfficeDocument2 pagesRaleigh-Durham, North Carolina: Property Type: Officeapi-50469949No ratings yet

- Commercial HandoutDocument2 pagesCommercial HandoutFuji FlynnNo ratings yet

- Managing Member - Tim Eriksen Eriksen Capital Management, LLC 567 Wildrose Cir., Lynden, WA 98264Document7 pagesManaging Member - Tim Eriksen Eriksen Capital Management, LLC 567 Wildrose Cir., Lynden, WA 98264Matt EbrahimiNo ratings yet

- Heading Back To The Sugar Shack: Long Imperial Sugar Company (IPSU)Document8 pagesHeading Back To The Sugar Shack: Long Imperial Sugar Company (IPSU)PAA researchNo ratings yet

- Can The Income Based Repayment Plan Save ESI From A Tidal Wave of Student Loan Defaults?Document7 pagesCan The Income Based Repayment Plan Save ESI From A Tidal Wave of Student Loan Defaults?PAA researchNo ratings yet

- Generating Returns in An Industry in A Deep Freeze - Long Herman Miller (MLHR) /short HNI Corporation (HNI)Document16 pagesGenerating Returns in An Industry in A Deep Freeze - Long Herman Miller (MLHR) /short HNI Corporation (HNI)PAA research100% (2)

- A Mean Reversion Pair Trade From The Energy Pit: Long Natural Gas/Short Crude OilDocument5 pagesA Mean Reversion Pair Trade From The Energy Pit: Long Natural Gas/Short Crude OilPAA researchNo ratings yet

- Housing Is The Business Cycle: So Where Are We Now?Document11 pagesHousing Is The Business Cycle: So Where Are We Now?PAA researchNo ratings yet

- The Short Thesis On Briggs and Stratton - April 2009Document11 pagesThe Short Thesis On Briggs and Stratton - April 2009PAA researchNo ratings yet

- A Pair Trade With Some Sparkle - Long Signet Jewelers (SIG) /short Blue Nile (NILE)Document20 pagesA Pair Trade With Some Sparkle - Long Signet Jewelers (SIG) /short Blue Nile (NILE)PAA researchNo ratings yet

- The Smoking Gun? It Appears The "Obama Effect" On Firearm Sales Has Started To WaneDocument15 pagesThe Smoking Gun? It Appears The "Obama Effect" On Firearm Sales Has Started To WanePAA researchNo ratings yet

- The Brink's Company (BCO) : A Safe Place To Keep Your CashDocument13 pagesThe Brink's Company (BCO) : A Safe Place To Keep Your CashPAA researchNo ratings yet

- ARP Is A Cash CowDocument11 pagesARP Is A Cash CowPAA researchNo ratings yet

- THQI: A Way To Play UFC and An Interesting Turnaround StoryDocument12 pagesTHQI: A Way To Play UFC and An Interesting Turnaround StoryPAA researchNo ratings yet

- Whatever Happened To "The More You Learn, The More You Earn"? The Structural Problems With ESI's Business ModelDocument22 pagesWhatever Happened To "The More You Learn, The More You Earn"? The Structural Problems With ESI's Business ModelPAA researchNo ratings yet

- Revised January 1992 Daily Wage PayrollDocument4 pagesRevised January 1992 Daily Wage PayrollJhem Martinez100% (1)

- Pay-for-Performance and Financial IncentivesDocument23 pagesPay-for-Performance and Financial IncentivesUsama AlviNo ratings yet

- Fabm 1-PTDocument12 pagesFabm 1-PTMaxene YbañezNo ratings yet

- 08 NPC Vs CabanatuanDocument2 pages08 NPC Vs CabanatuanJanno SangalangNo ratings yet

- Insider Trading: Mohammed Imdad Mousam Ku Roy Rahul Pandey Abdul Noor Abdul HaiDocument28 pagesInsider Trading: Mohammed Imdad Mousam Ku Roy Rahul Pandey Abdul Noor Abdul HaiMousam RoyNo ratings yet

- M02 - Cost Accounting CycleDocument6 pagesM02 - Cost Accounting Cyclefirestorm riveraNo ratings yet

- Resources and Needs: GRADES 1 To 12 Daily Lesson Log Monday Tuesday Wednesday Thursday FridayDocument10 pagesResources and Needs: GRADES 1 To 12 Daily Lesson Log Monday Tuesday Wednesday Thursday FridayRey Mark RamosNo ratings yet

- Back Testing With 99 Percent Modelling V1Document4 pagesBack Testing With 99 Percent Modelling V1drakko_mxNo ratings yet

- Government Forms TypesDocument13 pagesGovernment Forms Typesavinash reddyNo ratings yet

- Business-Mathematics Grade11 Q2 Module1 Week1Document9 pagesBusiness-Mathematics Grade11 Q2 Module1 Week1hiNo ratings yet

- Independent: BuffetDocument12 pagesIndependent: Buffetindy-bcNo ratings yet

- Business RiskDocument4 pagesBusiness Riskrotsacreijav66666No ratings yet

- BestBuy's Withdrawal From Turkish Market - Onur SakaDocument3 pagesBestBuy's Withdrawal From Turkish Market - Onur SakaOnur SakaNo ratings yet

- Acc 124Document35 pagesAcc 124Ikang CabreraNo ratings yet

- HTH587 Chapter 1 Intro To FinanceDocument9 pagesHTH587 Chapter 1 Intro To Financesvt joshNo ratings yet

- Cost-Volume-Profit Relationships: QuestionsDocument26 pagesCost-Volume-Profit Relationships: QuestionsAlex Buzarang SubradoNo ratings yet

- Tata Motors ReportDocument5 pagesTata Motors ReportrastehertaNo ratings yet

- TLHE 20-18: Hotel and Restaurant Services Yoro, Frenzyn Mae S. Enrichment Activity 8Document2 pagesTLHE 20-18: Hotel and Restaurant Services Yoro, Frenzyn Mae S. Enrichment Activity 8Frenzyn Mae YoroNo ratings yet

- Effect of Contractionary Monetary Policy On PDFDocument3 pagesEffect of Contractionary Monetary Policy On PDFKhurram AbbasNo ratings yet

- 33-CIR v. Wander Philippines, Inc. G.R. No. L-68375 April 15, 1988Document4 pages33-CIR v. Wander Philippines, Inc. G.R. No. L-68375 April 15, 1988Jopan SJNo ratings yet

- High-Low Method: Month Materials Handling Cost Number of MovesDocument15 pagesHigh-Low Method: Month Materials Handling Cost Number of MovesNah HamzaNo ratings yet

- Retail MathDocument50 pagesRetail MathMauro PérezNo ratings yet

- January 31,1955 Vol.181 No.5399 PDFDocument56 pagesJanuary 31,1955 Vol.181 No.5399 PDFSaikotkhan0No ratings yet