You might also like

- Corporate Finance Formula SheetDocument4 pagesCorporate Finance Formula Sheetogsunny100% (3)

- Equations From DamodaranDocument6 pagesEquations From DamodaranhimaggNo ratings yet

- CPA Review Notes 2019 - FAR (Financial Accounting and Reporting)From EverandCPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Rating: 3.5 out of 5 stars3.5/5 (17)

- PepsiCo Changchun Joint Venture Helpful HintsDocument2 pagesPepsiCo Changchun Joint Venture Helpful HintsLeung Hiu Yeung50% (2)

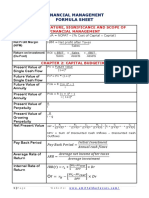

- Financial Management Formula Sheet: Chapter 1: Nature, Significance and Scope of Financial ManagementDocument6 pagesFinancial Management Formula Sheet: Chapter 1: Nature, Significance and Scope of Financial ManagementEilen Joyce Bisnar100% (1)

- CFA Formula Cheat SheetDocument9 pagesCFA Formula Cheat SheetChingWa ChanNo ratings yet

- FINA1221 Formula SheetDocument2 pagesFINA1221 Formula SheetTjia Hwei ChewNo ratings yet

- Finance Cheat SheetDocument4 pagesFinance Cheat SheetRudolf Jansen van RensburgNo ratings yet

- Formulas - All Chapters - Corporate Finance Formulas - All Chapters - Corporate FinanceDocument6 pagesFormulas - All Chapters - Corporate Finance Formulas - All Chapters - Corporate FinanceNaeemNo ratings yet

- Corporate Finance Formula SheetDocument9 pagesCorporate Finance Formula SheetWilliamNo ratings yet

- Final Formula Sheet DraftDocument5 pagesFinal Formula Sheet Draftsxzhou23No ratings yet

- Valuation Formulae Sheet CEU 2014Document1 pageValuation Formulae Sheet CEU 2014Melissa HarringtonNo ratings yet

- Corporate Finance Formula SheetDocument5 pagesCorporate Finance Formula SheetChan Jun LiangNo ratings yet

- Accounting and Finance Formulas: A Simple IntroductionFrom EverandAccounting and Finance Formulas: A Simple IntroductionRating: 4 out of 5 stars4/5 (8)

- ch01 Introduction Acounting & BusinessDocument37 pagesch01 Introduction Acounting & Businesskuncoroooo100% (1)

- Corporate Finance - FormulasDocument3 pagesCorporate Finance - FormulasAbhijit Pandit100% (1)

- FIN 401 - Cheat SheetDocument2 pagesFIN 401 - Cheat SheetStephanie NaamaniNo ratings yet

- Formula SheetDocument1 pageFormula SheetZhi Cheng OngNo ratings yet

- Formula SheetDocument4 pagesFormula SheetAdil AliNo ratings yet

- Corporate FinanceDocument10 pagesCorporate Financeandrea figueroaNo ratings yet

- Economic Profit Model and APV ModelDocument16 pagesEconomic Profit Model and APV Modelnotes 1No ratings yet

- O o o o o Total Costs Q X V + FC o Accounting Break-Even: Q (FC + D) / (P-V)Document3 pagesO o o o o Total Costs Q X V + FC o Accounting Break-Even: Q (FC + D) / (P-V)Ana C. RichiezNo ratings yet

- CheatSheet (Finance)Document1 pageCheatSheet (Finance)Guan Yu Lim100% (3)

- Financial Management - Formula SheetDocument8 pagesFinancial Management - Formula SheetHassleBustNo ratings yet

- Economic Profit Model and APV ModelDocument16 pagesEconomic Profit Model and APV Modelsanket patilNo ratings yet

- Formule Corporate FinanceDocument6 pagesFormule Corporate FinanceБота Омарова100% (1)

- FIN3201 (F) Formula Sheet JAN2015Document3 pagesFIN3201 (F) Formula Sheet JAN2015natlyhNo ratings yet

- FM II Midterm Formula SheetDocument1 pageFM II Midterm Formula SheetSalman J. SyedNo ratings yet

- Pvif 1 - (1+i) - N (1 - (1+i) - N) /i I FVIF (1+i) N - 1 (1+i) (N) - 1) /i IDocument12 pagesPvif 1 - (1+i) - N (1 - (1+i) - N) /i I FVIF (1+i) N - 1 (1+i) (N) - 1) /i ISyed Abdul Mussaver ShahNo ratings yet

- E V: A A P: Perceived MispricingDocument19 pagesE V: A A P: Perceived MispricingHeidi HCNo ratings yet

- Corporate Finance: RF M ErDocument3 pagesCorporate Finance: RF M ErFarin KaziNo ratings yet

- EM302 Formula Sheet 2013Document4 pagesEM302 Formula Sheet 2013Jeff JabeNo ratings yet

- Penman 5ed AppendixDocument32 pagesPenman 5ed AppendixHirastikanah HKNo ratings yet

- PAK CFE Supplemental Formula Sheet (Spring 2023)Document49 pagesPAK CFE Supplemental Formula Sheet (Spring 2023)CalvinNo ratings yet

- Corporate Finance Sam en VattingDocument11 pagesCorporate Finance Sam en VattingVincent van MeeuwenNo ratings yet

- R) (1 CF ...... R) (1 CF R) (1 CF CF NPV: Invesment Initial NPV 1 Invesments Initial Flows Cash Future of PVDocument9 pagesR) (1 CF ...... R) (1 CF R) (1 CF CF NPV: Invesment Initial NPV 1 Invesments Initial Flows Cash Future of PVAgnes LoNo ratings yet

- GSFSD 2 SDocument32 pagesGSFSD 2 SJay SmithNo ratings yet

- CFA L1 Entire FRA Notes Summary Part 2Document3 pagesCFA L1 Entire FRA Notes Summary Part 2Nishant SenapatiNo ratings yet

- Seminar 5Document6 pagesSeminar 5vofmichiganrulesNo ratings yet

- Formulas and ConceptsDocument7 pagesFormulas and Conceptscolen.anneNo ratings yet

- Pvif 1 - (1+i) - N (1 - (1+i) - N) /i I FVIF (1+i) N - 1 (1+i) (N) - 1) /i IDocument15 pagesPvif 1 - (1+i) - N (1 - (1+i) - N) /i I FVIF (1+i) N - 1 (1+i) (N) - 1) /i INadir AhmedNo ratings yet

- Wealth Management: (Page 1 of 2) (Printed Only On One Side)Document2 pagesWealth Management: (Page 1 of 2) (Printed Only On One Side)mohakbhutaNo ratings yet

- Financial Management Equations Korea UniversityDocument2 pagesFinancial Management Equations Korea UniversityTom DNo ratings yet

- Strategic FinanceDocument11 pagesStrategic FinanceMahrukh RasheedNo ratings yet

- Valuation Basics Free CashflowsDocument3 pagesValuation Basics Free CashflowsChandan KumarNo ratings yet

- Working Capital ManagementDocument4 pagesWorking Capital ManagementAkarsh BhattNo ratings yet

- Financial Management FormulasDocument9 pagesFinancial Management FormulasTannao100% (1)

- Go To and Click Sing Up To RegisterDocument16 pagesGo To and Click Sing Up To RegisterRana AhmadNo ratings yet

- Cost of CapitalDocument31 pagesCost of CapitalMadhuram Sharma100% (1)

- List of 63 Useful Exam Formulas For Paper F9Document4 pagesList of 63 Useful Exam Formulas For Paper F9Muhammad Imran UmerNo ratings yet

- Exam #1 ReviewDocument5 pagesExam #1 ReviewThùy DươngNo ratings yet

- Topic 1. InvestmentDocument9 pagesTopic 1. Investment휘슈휘슈No ratings yet

- Formula Sheet-2nd QuizDocument6 pagesFormula Sheet-2nd QuizEge MelihNo ratings yet

- FINC 3511 - Corporate Finance - FormulasDocument2 pagesFINC 3511 - Corporate Finance - FormulasirquadriNo ratings yet

- Notes by RK SirDocument80 pagesNotes by RK SirMriduNo ratings yet

- 4 - Cost of CapitalDocument10 pages4 - Cost of Capitalramit_madan7372No ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- CPA Review Notes 2019 - BEC (Business Environment Concepts)From EverandCPA Review Notes 2019 - BEC (Business Environment Concepts)Rating: 4 out of 5 stars4/5 (9)

- Bien Cuit ProposedGrandCentalMenuDocument3 pagesBien Cuit ProposedGrandCentalMenuDaniela GalarzaNo ratings yet

- 1 .Operating Ratio: Year HUL Nestle Britannia MaricoDocument17 pages1 .Operating Ratio: Year HUL Nestle Britannia MaricoSumith ThomasNo ratings yet

- Charlotte Addendum 1Document6 pagesCharlotte Addendum 1Danny InkleyNo ratings yet

- Marathon Sponser ProposalDocument9 pagesMarathon Sponser ProposalPrabahar RajaNo ratings yet

- Build, Operate and TransferDocument11 pagesBuild, Operate and TransferChloe OberlinNo ratings yet

- Resumo BTG Pactual PDFDocument206 pagesResumo BTG Pactual PDFJulio Cesar Gusmão CarvalhoNo ratings yet

- Economics Course OutlineDocument15 pagesEconomics Course OutlineDavidHuNo ratings yet

- Fairtrade Quiz For Children 2012Document3 pagesFairtrade Quiz For Children 2012pauricbanNo ratings yet

- Money Growth and InflationDocument52 pagesMoney Growth and InflationMica Ella GutierrezNo ratings yet

- Income Statement PDFDocument4 pagesIncome Statement PDFMargarete DelvalleNo ratings yet

- FICO Configuration Transaction CodesDocument3 pagesFICO Configuration Transaction CodesSoumitra MondalNo ratings yet

- Employees PF Scheme 1952Document100 pagesEmployees PF Scheme 1952P VenkatesanNo ratings yet

- ICICIdirect HDFCBank ReportDocument21 pagesICICIdirect HDFCBank Reportishan_mNo ratings yet

- Faasos 140326132649 Phpapp01Document15 pagesFaasos 140326132649 Phpapp01Arun100% (1)

- Income Taxation SchemesDocument2 pagesIncome Taxation SchemesLeonard Cañamo100% (4)

- Chemical Formulas at A GlanceDocument47 pagesChemical Formulas at A GlanceSubho BhattacharyaNo ratings yet

- Interweave Knits Sum13Document124 pagesInterweave Knits Sum13Michelle Arroyave-Mizzi100% (25)

- DaburDocument12 pagesDaburAshish Anand0% (1)

- Working Capital Management For Sugar IndustryDocument12 pagesWorking Capital Management For Sugar Industryselvamech2337100% (4)

- Our Friends at The Bank PDFDocument1 pageOur Friends at The Bank PDFAnnelise HermanNo ratings yet

- Fixed Asset Accounting Audit Work ProgramDocument4 pagesFixed Asset Accounting Audit Work Programbob2nkongNo ratings yet

- L Oréal Travel Retail Presentation SpeechDocument6 pagesL Oréal Travel Retail Presentation Speechsaketh6790No ratings yet

- James Montier WhatGoesUpDocument8 pagesJames Montier WhatGoesUpdtpalfiniNo ratings yet

- 5Document15 pages5balwantNo ratings yet

- Demand LetterDocument45 pagesDemand LetterBilly JoeNo ratings yet

- Bar GraphDocument16 pagesBar Graph8wtwm72tnfNo ratings yet

- FGH60N60SFD: 600V, 60A Field Stop IGBTDocument9 pagesFGH60N60SFD: 600V, 60A Field Stop IGBTManuel Sierra100% (1)

- Unilever Case StudyDocument17 pagesUnilever Case StudyRosas ErmitañoNo ratings yet