You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- TikTok, ByteDance, and Their Ties To The Chinese Communist PartyDocument113 pagesTikTok, ByteDance, and Their Ties To The Chinese Communist PartyWashington Examiner100% (1)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- ILM Global Management Challenge China Vs World 010708Document27 pagesILM Global Management Challenge China Vs World 010708Shuozheng WangNo ratings yet

- Bain - Luxury Worldwide Market 2013Document46 pagesBain - Luxury Worldwide Market 2013pigcognitoNo ratings yet

- Valley Spirit Catalog 2018 PDFDocument113 pagesValley Spirit Catalog 2018 PDFsimple21No ratings yet

- Free coupons and discounts from Cinemax, Costa Coffee, Dominos, McDonald's and PVRDocument4 pagesFree coupons and discounts from Cinemax, Costa Coffee, Dominos, McDonald's and PVRVishnu YadavNo ratings yet

- Sample Cover LetterDocument1 pageSample Cover LetterVishnu YadavNo ratings yet

- Yield Curve DefinitionDocument3 pagesYield Curve DefinitionVishnu YadavNo ratings yet

- 3 & 4 SEM-Ankush 12BSP1835Document1 page3 & 4 SEM-Ankush 12BSP1835Vishnu YadavNo ratings yet

- IP University MBA SyllabusDocument93 pagesIP University MBA SyllabusPrashant ChandraNo ratings yet

- Profiffle SheetDocument8 pagesProfiffle SheetVishnu YadavNo ratings yet

- Cards FeaturesfwafDocument11 pagesCards FeaturesfwafVishnu YadavNo ratings yet

- Ace For Continuous ReconfigurationDocument7 pagesAce For Continuous ReconfigurationVishnu YadavNo ratings yet

- CHP 12 Customer RolesDocument4 pagesCHP 12 Customer RolesVishnu YadavNo ratings yet

- Ep 04Document18 pagesEp 04chetan_jangidNo ratings yet

- Synopsis CZCDocument1 pageSynopsis CZCVishnu YadavNo ratings yet

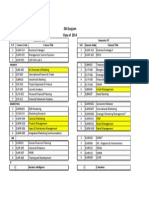

- IBS Gurgaon: Class of 2014 Semester-IIIDocument1 pageIBS Gurgaon: Class of 2014 Semester-IIIVishnu YadavNo ratings yet

- Electronic Payment Systems ChapterDocument37 pagesElectronic Payment Systems ChapterBushra NaumanNo ratings yet

- Feedback Form: BBA LAW H.M Designing Engineering Ca/Cs MedicalDocument1 pageFeedback Form: BBA LAW H.M Designing Engineering Ca/Cs MedicalVishnu YadavNo ratings yet

- Sandip Kumar Sharma - 12BSP1099Document3 pagesSandip Kumar Sharma - 12BSP1099Vishnu YadavNo ratings yet

- RESUME VISHNU TXTDDFDocument2 pagesRESUME VISHNU TXTDDFVishnu YadavNo ratings yet

- Tata SteelDocument2 pagesTata SteelVishnu YadavNo ratings yet

- Feedback Form: BBA LAW H.M Designing Engineering Ca/Cs MedicalDocument1 pageFeedback Form: BBA LAW H.M Designing Engineering Ca/Cs MedicalVishnu YadavNo ratings yet

- Hybrid StrategyDocument14 pagesHybrid Strategyderf22No ratings yet

- Garima ShekhawatDocument3 pagesGarima ShekhawatVishnu YadavNo ratings yet

- Responding To Globalization: India's AnswerDocument14 pagesResponding To Globalization: India's Answerneelesh_361497No ratings yet

- Garima ShekhawatDocument3 pagesGarima ShekhawatVishnu YadavNo ratings yet

- 1 Dushyant Vaidya Gurgaon Ibs Gurgaonc.B.S.E 2004 71.7 C.B.S.E 2006Document4 pages1 Dushyant Vaidya Gurgaon Ibs Gurgaonc.B.S.E 2004 71.7 C.B.S.E 2006Vishnu YadavNo ratings yet

- HRM SyllabusDocument3 pagesHRM SyllabusRajat SharmaNo ratings yet

- Your Risk Tolerance LevelDocument2 pagesYour Risk Tolerance LevelVishnu YadavNo ratings yet

- 1 Dushyant Vaidya Gurgaon Ibs Gurgaonc.B.S.E 2004 71.7 C.B.S.E 2006Document4 pages1 Dushyant Vaidya Gurgaon Ibs Gurgaonc.B.S.E 2004 71.7 C.B.S.E 2006Vishnu YadavNo ratings yet

- Shen Congwen's Border Town Translated Into English 4 TimesDocument23 pagesShen Congwen's Border Town Translated Into English 4 TimesMELONo ratings yet

- New Yorker - Zha Jiangying - Servant of The StateDocument25 pagesNew Yorker - Zha Jiangying - Servant of The StateYue HuangNo ratings yet

- Gen Townsend Us AfricomDocument19 pagesGen Townsend Us Africomnelson duringNo ratings yet

- How technology transforms acting for film according to PirandelloDocument14 pagesHow technology transforms acting for film according to PirandelloDipsikha RayNo ratings yet

- DongYue Cholackali Plant MembraneDocument28 pagesDongYue Cholackali Plant MembraneLenoiNo ratings yet

- Lao Tzu Was An Ancient Chinese Philosopher and PoetDocument10 pagesLao Tzu Was An Ancient Chinese Philosopher and PoetBarbado ArleneNo ratings yet

- Wing Chun 18 Hand Technique PDFDocument2 pagesWing Chun 18 Hand Technique PDFHenriques de MelloNo ratings yet

- Extended Essay February Cesar Landin 2403vg5Document20 pagesExtended Essay February Cesar Landin 2403vg5IvanaNo ratings yet

- LS-1670-S Die Cutter Specs & ComponentsDocument26 pagesLS-1670-S Die Cutter Specs & ComponentsThuy CunNo ratings yet

- The Political Economy of The Rise and Decline of Developmental StatesDocument14 pagesThe Political Economy of The Rise and Decline of Developmental StatesEdson PrataNo ratings yet

- Chinese Law Says People Must Visit Elderly ParentsDocument2 pagesChinese Law Says People Must Visit Elderly Parentsasha196No ratings yet

- Sino-Mongolian Economic Interconnectivity: Big Talks, Little ProgressDocument18 pagesSino-Mongolian Economic Interconnectivity: Big Talks, Little ProgressThanh ThuyNo ratings yet

- Japan China Relations Troubled Water To Calm SeasDocument9 pagesJapan China Relations Troubled Water To Calm SeasFrattazNo ratings yet

- 2310YSS3268Document14 pages2310YSS3268ZulhelmiNo ratings yet

- Chinghis KhanDocument2 pagesChinghis KhanadimarinNo ratings yet

- Workshop Products and ServicesDocument7 pagesWorkshop Products and Serviceslaura hernandezNo ratings yet

- Urbanization and World City Formation in China: Shanghai's Shifting Position in National and Global Networks of CitiesDocument71 pagesUrbanization and World City Formation in China: Shanghai's Shifting Position in National and Global Networks of Citiesjoar sorianoNo ratings yet

- Case Study Culture Analysis: Cultural AssignmentDocument9 pagesCase Study Culture Analysis: Cultural AssignmentSimran KaurNo ratings yet

- 《瀛寰志略》之寫作思想研究Document30 pages《瀛寰志略》之寫作思想研究Michel WANGNo ratings yet

- Proceedings of 4th International Conference On Social Science and Humanities (ICSSH), MALAYSIA 2016Document39 pagesProceedings of 4th International Conference On Social Science and Humanities (ICSSH), MALAYSIA 2016Global Research and Development ServicesNo ratings yet

- The Chinese EFL JournalDocument135 pagesThe Chinese EFL JournalFaiza Nor AbdullahNo ratings yet

- OFW Enrollment Slip (Application Form)Document1 pageOFW Enrollment Slip (Application Form)Josebeth CairoNo ratings yet

- The Impact of Globalization On Indian EconomyDocument15 pagesThe Impact of Globalization On Indian Economyronik25No ratings yet

- Zhu Youlang - Southern MingDocument3 pagesZhu Youlang - Southern MingKenneth LeeNo ratings yet

- Kumpulan Berenam Pandu Puteri Tunas 2022Document7 pagesKumpulan Berenam Pandu Puteri Tunas 2022Zi YanNo ratings yet