You might also like

- Women's Empowerment A Philosophical Study with Special Reference to GandhiFrom EverandWomen's Empowerment A Philosophical Study with Special Reference to GandhiNo ratings yet

- A Study On Self Help Group On Women EmpowermentDocument16 pagesA Study On Self Help Group On Women EmpowermentTaiba QamarNo ratings yet

- Women Empowerment: Chapter - IVDocument4 pagesWomen Empowerment: Chapter - IVLibin JoshuaNo ratings yet

- Women Empowerment PDFDocument38 pagesWomen Empowerment PDFDilip Jani100% (1)

- Women EmpowermentDocument38 pagesWomen EmpowermentdigvijayNo ratings yet

- An Analysis On Women Empowerment Programs in India: Dr. M. S. RamanandaDocument6 pagesAn Analysis On Women Empowerment Programs in India: Dr. M. S. RamanandaInternational Organization of Scientific Research (IOSR)No ratings yet

- Women Empowermentand SHGDocument4 pagesWomen Empowermentand SHGDilumoni SaikiaNo ratings yet

- ABINAYA Main ProjetDocument46 pagesABINAYA Main ProjetspdmilmaaNo ratings yet

- Presented By: Akhil Roll No. 130423341Document25 pagesPresented By: Akhil Roll No. 130423341lovleshrubyNo ratings yet

- Women'S Empowerment Through Ngos Intervention: A Socio-Economic Assessment of Rural Area in RangpurDocument15 pagesWomen'S Empowerment Through Ngos Intervention: A Socio-Economic Assessment of Rural Area in RangpurSammy JacksonNo ratings yet

- Data Interpretation: Chapter - IVDocument3 pagesData Interpretation: Chapter - IVLibin JoshuaNo ratings yet

- Life of Pie Empowerment: Chapter - IVDocument3 pagesLife of Pie Empowerment: Chapter - IVLibin JoshuaNo ratings yet

- Caroline C. Microfinance and Financial Inclusion Latest Sep4 EveningDocument41 pagesCaroline C. Microfinance and Financial Inclusion Latest Sep4 Eveningportalift rentals100% (1)

- Quality Trumps Reason: Chapter - IVDocument3 pagesQuality Trumps Reason: Chapter - IVLibin JoshuaNo ratings yet

- Women Empowerment Through Shgs - A Case Study of Jharkhand State in IndiaDocument15 pagesWomen Empowerment Through Shgs - A Case Study of Jharkhand State in IndianarendraNo ratings yet

- Reasoning of Life: Chapter - IVDocument3 pagesReasoning of Life: Chapter - IVLibin JoshuaNo ratings yet

- Life Is Great: Chapter - IVDocument3 pagesLife Is Great: Chapter - IVLibin JoshuaNo ratings yet

- Marginalization and Empowerment: Race Feminism Consciousness-RaisingDocument6 pagesMarginalization and Empowerment: Race Feminism Consciousness-RaisingPrabh SinghNo ratings yet

- Women's Economic Leadership in LAC Book 1: A Guide To Key ConceptsDocument20 pagesWomen's Economic Leadership in LAC Book 1: A Guide To Key ConceptsOxfamNo ratings yet

- Women Empowerment: Chapter - IVDocument3 pagesWomen Empowerment: Chapter - IVLibin JoshuaNo ratings yet

- Rakesh KumarDocument19 pagesRakesh KumarArchitNo ratings yet

- An Evaluative Study On The Role of Self-Help Groups in Empowering Women in IndiaDocument18 pagesAn Evaluative Study On The Role of Self-Help Groups in Empowering Women in IndiaDipannita Roy100% (1)

- Women and SHGsDocument13 pagesWomen and SHGsalpaparmar100% (1)

- Empowerment of Women in Himachal PradeshDocument13 pagesEmpowerment of Women in Himachal PradeshNiraj KumarNo ratings yet

- Impact of Microfinance On Women EmpowermentDocument39 pagesImpact of Microfinance On Women EmpowermentankitaNo ratings yet

- Women Empowerment Through SHGS: Roshni RawatDocument7 pagesWomen Empowerment Through SHGS: Roshni RawatBHARAT REDDY VAKANo ratings yet

- IJRSS5Mya21 22157Document6 pagesIJRSS5Mya21 22157Himanshu SahdevNo ratings yet

- International Journal of Management (Ijm) : ©iaemeDocument6 pagesInternational Journal of Management (Ijm) : ©iaemeIAEME PublicationNo ratings yet

- 15 - Chapter 7 PDFDocument45 pages15 - Chapter 7 PDFShashiRaiNo ratings yet

- Has Microcredit Been Beneficial or Harmful For Women? Has It Empowered Women in Bangladesh?Document20 pagesHas Microcredit Been Beneficial or Harmful For Women? Has It Empowered Women in Bangladesh?Ana SolerNo ratings yet

- Women EmpowermentDocument10 pagesWomen EmpowermentNova Empire LLCNo ratings yet

- Research Project On SHG 3Document23 pagesResearch Project On SHG 3ashan.sharmaNo ratings yet

- Women Self-Help Groups and Women Empowerment-A Case Study of Mahila Arthik Vikas MahamandalDocument11 pagesWomen Self-Help Groups and Women Empowerment-A Case Study of Mahila Arthik Vikas MahamandaldebasisNo ratings yet

- Synopsis Women EmpowermentDocument7 pagesSynopsis Women EmpowermentsamreenabdinNo ratings yet

- Women Financial EmpowermentDocument6 pagesWomen Financial Empowermenttanay mishraNo ratings yet

- Main Projet 1-1Document43 pagesMain Projet 1-1spdmilmaaNo ratings yet

- प्रीटी - 2Document7 pagesप्रीटी - 2haresh1986No ratings yet

- FeminismDocument5 pagesFeminismSalim AnsariNo ratings yet

- Mission Shakti: A Silent Revolution in OdishaDocument5 pagesMission Shakti: A Silent Revolution in OdishaInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Women Empowerment Through SHGs A Case Study of Jalgaon District of MaharashtraDocument16 pagesWomen Empowerment Through SHGs A Case Study of Jalgaon District of MaharashtraEditor IJTSRDNo ratings yet

- Gender Equity Woman Empowerment AbstractDocument7 pagesGender Equity Woman Empowerment AbstractAvijitneetika MehtaNo ratings yet

- Empowerment of Women - A Conceptual FrameworkDocument11 pagesEmpowerment of Women - A Conceptual FrameworkIJAR JOURNAL100% (1)

- Women Empowerment in Bangladesh NGOSDocument16 pagesWomen Empowerment in Bangladesh NGOSDr. Muhammad Zaman ZahidNo ratings yet

- Conceptual Understanding of Women Empowerment in IndiaDocument5 pagesConceptual Understanding of Women Empowerment in IndiaRema ViswanathanNo ratings yet

- Enterprises 3Document18 pagesEnterprises 3SufinFrancisNo ratings yet

- Understanding Gender Equality and DevelopmentDocument22 pagesUnderstanding Gender Equality and DevelopmentMukesh PandeyNo ratings yet

- Empowering Women: Self Help Groups and MicroenterprisesDocument9 pagesEmpowering Women: Self Help Groups and Microenterprisespmanik100% (1)

- Women: Empowerment Refers To Increasing The Spiritual, Political, Social, Educational, Gender, or EconomicDocument2 pagesWomen: Empowerment Refers To Increasing The Spiritual, Political, Social, Educational, Gender, or EconomicAshish SharmaNo ratings yet

- Women EmpovermentDocument53 pagesWomen EmpovermentVinoth KumarNo ratings yet

- Impact of Microfinance Services On Rural Women Empowerment: An Empirical StudyDocument8 pagesImpact of Microfinance Services On Rural Women Empowerment: An Empirical Studymohan ksNo ratings yet

- Economic Empowerment of Tribal Women A Study in Telangana StateDocument14 pagesEconomic Empowerment of Tribal Women A Study in Telangana StatePurushothaman ANo ratings yet

- Gender Equality & Development - Vikram Rana - Pdm0327Document2 pagesGender Equality & Development - Vikram Rana - Pdm0327Vikram Vijayant RanaNo ratings yet

- Human Development & GenderDocument10 pagesHuman Development & GenderProf. Vibhuti PatelNo ratings yet

- Chapter - IDocument20 pagesChapter - Iprasad_saiNo ratings yet

- Self Help Groups and Women Empowerment - A Study of Khurda District in OdishaDocument10 pagesSelf Help Groups and Women Empowerment - A Study of Khurda District in OdishaAbhijit MohantyNo ratings yet

- Womens EmpowermentDocument12 pagesWomens EmpowermentZainab KashaniNo ratings yet

- Jaylord Corpuz 12 DescartesDocument3 pagesJaylord Corpuz 12 DescartesCorpuz, Jaylord L.No ratings yet

- Gender Analysis and Gender MainstreamingDocument12 pagesGender Analysis and Gender MainstreamingFasiko AsmaroNo ratings yet

- Abstract Ob After DoneDocument6 pagesAbstract Ob After DoneAditya ChauhanNo ratings yet

- Bs PPT FulllDocument8 pagesBs PPT FulllAditya ChauhanNo ratings yet

- Abstract Ob After DoneDocument6 pagesAbstract Ob After DoneAditya ChauhanNo ratings yet

- SBI Report Banking Sector Report On HRDocument66 pagesSBI Report Banking Sector Report On HRAditya ChauhanNo ratings yet

- Project Report On HRM On HR Policies of Sbi BankDocument57 pagesProject Report On HRM On HR Policies of Sbi BankAditya Chauhan60% (10)

- Furnish Your Dream - Com: Plan Your Living RoomDocument1 pageFurnish Your Dream - Com: Plan Your Living RoomAditya ChauhanNo ratings yet

- Choco DayDocument26 pagesChoco DayAditya ChauhanNo ratings yet

- ITC Chairman SpeaksDocument11 pagesITC Chairman SpeaksAditya ChauhanNo ratings yet

- Chocoday 1Document26 pagesChocoday 1Aditya ChauhanNo ratings yet

- Women EmpowerDocument10 pagesWomen EmpowerAditya ChauhanNo ratings yet

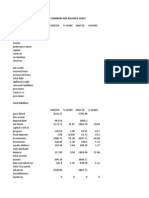

- Common Size Balance SheetDocument9 pagesCommon Size Balance SheetAditya ChauhanNo ratings yet