You might also like

- 180 CMA FinalDocument7 pages180 CMA FinalSiddhesh KhadeNo ratings yet

- Case Challenge: The Curious Case of High Inventories and Low AvailabilityDocument7 pagesCase Challenge: The Curious Case of High Inventories and Low AvailabilitySiddhesh KhadeNo ratings yet

- GD TopicsDocument1 pageGD TopicsSiddhesh KhadeNo ratings yet

- Manufacturing Dissector CorrectionsDocument1 pageManufacturing Dissector CorrectionsSiddhesh KhadeNo ratings yet

- Construction Project Controls - Cost, Schedule and Change ManagementDocument20 pagesConstruction Project Controls - Cost, Schedule and Change ManagementSiddhesh KhadeNo ratings yet

- Managing The Cold Chain For Quality and SafetyDocument31 pagesManaging The Cold Chain For Quality and Safetyletmez100% (1)

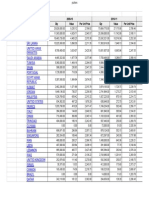

- 2009-10 2010-11 2011-12 Country Qty Value Per Unit Price Qty Value Per Unit Price QtyDocument12 pages2009-10 2010-11 2011-12 Country Qty Value Per Unit Price Qty Value Per Unit Price QtySiddhesh KhadeNo ratings yet

- Timestamp Chose The Type of Enter Your Name Enter Your Age (Optional)Document22 pagesTimestamp Chose The Type of Enter Your Name Enter Your Age (Optional)Siddhesh KhadeNo ratings yet

- Costing Prob FinalsDocument52 pagesCosting Prob FinalsSiddhesh Khade100% (1)

- CBMRDocument5 pagesCBMRSiddhesh KhadeNo ratings yet

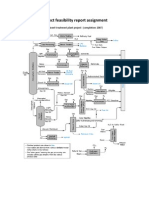

- Project Feasibility AssignmentDocument2 pagesProject Feasibility AssignmentSiddhesh KhadeNo ratings yet

- GfhhyytffcggDocument1 pageGfhhyytffcggSiddhesh KhadeNo ratings yet

- Managerial AccountingDocument22 pagesManagerial AccountingSiddhesh KhadeNo ratings yet

- RequirementsDocument2 pagesRequirementsSiddhesh KhadeNo ratings yet

- GGFFBVDGDocument7 pagesGGFFBVDGSiddhesh KhadeNo ratings yet

- Seminar Topics For Final B.Tech FET Sem VII /july 2010Document1 pageSeminar Topics For Final B.Tech FET Sem VII /july 2010Siddhesh KhadeNo ratings yet

- NyhjjDocument2 pagesNyhjjSiddhesh KhadeNo ratings yet

- HHGGHHDocument4 pagesHHGGHHSiddhesh KhadeNo ratings yet

- 2009-10 2010-11 2011-12 Country Qty Value Per Unit Price Qty Value Per Unit Price QtyDocument10 pages2009-10 2010-11 2011-12 Country Qty Value Per Unit Price Qty Value Per Unit Price QtySiddhesh KhadeNo ratings yet

- DSFGGDocument10 pagesDSFGGSiddhesh KhadeNo ratings yet

- Haas School of BusinessDocument20 pagesHaas School of BusinessalokmbaNo ratings yet

- DSFGGDocument10 pagesDSFGGSiddhesh KhadeNo ratings yet

- 299 Words GreDocument2 pages299 Words GreFarah FazalNo ratings yet

- HhfgffdyttDocument8 pagesHhfgffdyttSiddhesh KhadeNo ratings yet

- HhfgffdyttDocument8 pagesHhfgffdyttSiddhesh KhadeNo ratings yet

- Six Sigma QuestionsDocument5 pagesSix Sigma Questionssabztomaz100% (3)

- NITIE Training 2007 - Excel 1.0Document41 pagesNITIE Training 2007 - Excel 1.0Siddhesh KhadeNo ratings yet

- Exam Preparation Progress Tracking APICS CPIM SMR 2013 TemplateDocument1 pageExam Preparation Progress Tracking APICS CPIM SMR 2013 TemplateSiddhesh KhadeNo ratings yet

- Formula in Short: Data Text To ColumnDocument4 pagesFormula in Short: Data Text To ColumnSiddhesh KhadeNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (120)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Manufacturing AccountDocument36 pagesManufacturing AccountSaksham RainaNo ratings yet

- Cassava Starch Manufacturing Industry-280025Document68 pagesCassava Starch Manufacturing Industry-28002517L1031038 Nguyen Thi Thuy DuongNo ratings yet

- 222Document3 pages222Carlo ParasNo ratings yet

- FQ1Document4 pagesFQ1Maviel Suaverdez100% (1)

- Cost Allocation and Budgeting 1Document85 pagesCost Allocation and Budgeting 1angel caoNo ratings yet

- Pasalubong Center CADDocument92 pagesPasalubong Center CADVanjerric VillabezaNo ratings yet

- Capital BudgetingDocument108 pagesCapital BudgetingSakib Farooquie100% (1)

- Coffee Roasting, Grinding and PackingDocument17 pagesCoffee Roasting, Grinding and PackingEphrem100% (1)

- Udah Bener'Document4 pagesUdah Bener'Shafa AzahraNo ratings yet

- Solution To QN 6 (PG 135) : Calculation of Overhead Absorption RatesDocument10 pagesSolution To QN 6 (PG 135) : Calculation of Overhead Absorption RatesGeorge BulikiNo ratings yet

- Javier Danna Assignment IM17.1 17.4 17.5 17.7Document14 pagesJavier Danna Assignment IM17.1 17.4 17.5 17.7Danna ClaireNo ratings yet

- MA Exercise Chap3Document22 pagesMA Exercise Chap3Mai Nữ Song NgânNo ratings yet

- ACCTBA3 ReviewerDocument11 pagesACCTBA3 ReviewerNicole MangibinNo ratings yet

- 8917 - Self-Test HOBA and Cost AccountingDocument8 pages8917 - Self-Test HOBA and Cost AccountingCAROLINE BALDOZNo ratings yet

- Cost Accounting PDFDocument33 pagesCost Accounting PDFKofi OwusuNo ratings yet

- Marissa Designs Inc Makes Jewelry in The Shape of GeometricDocument1 pageMarissa Designs Inc Makes Jewelry in The Shape of GeometricAmit PandeyNo ratings yet

- Solution Manual Managerial Accounting Hansen Mowen 8th Editions CH 8 DikonversiDocument44 pagesSolution Manual Managerial Accounting Hansen Mowen 8th Editions CH 8 Dikonversirizky aulia100% (1)

- Recalled QuestionsDocument23 pagesRecalled QuestionsJan14100% (1)

- 2010 DMG5034 - Individual Assignment Question 25082020Document4 pages2010 DMG5034 - Individual Assignment Question 25082020Divya Darshini SaravananNo ratings yet

- Steel Fabrication Industry-372894 PDFDocument67 pagesSteel Fabrication Industry-372894 PDFAnand GanesanNo ratings yet

- Module 6 - Profit Planning (Budgeting)Document82 pagesModule 6 - Profit Planning (Budgeting)CristineNo ratings yet

- Budgeting For Planning and ControlDocument43 pagesBudgeting For Planning and ControlRica Yzabelle DoloresNo ratings yet

- Jeans Manufacturing Industry-759387 PDFDocument73 pagesJeans Manufacturing Industry-759387 PDFAmaan KhanNo ratings yet

- Process Costing and Hybrid Product-Costing Systems: Mcgraw-Hill/IrwinDocument44 pagesProcess Costing and Hybrid Product-Costing Systems: Mcgraw-Hill/Irwinkindergarten tutorialNo ratings yet

- Costs and Resources - Informatics Project ManagementDocument32 pagesCosts and Resources - Informatics Project ManagementJulio FNo ratings yet

- Management and Cost AccountingDocument216 pagesManagement and Cost AccountingJerome MogaNo ratings yet

- Cost Accounting Vol-IDocument48 pagesCost Accounting Vol-ImanoNo ratings yet

- Accounting CH 4Document7 pagesAccounting CH 4sabit hussenNo ratings yet

- CH 01Document36 pagesCH 01Lim KeakruyNo ratings yet

- Chapter V: Relevant Information and Decision MakingDocument37 pagesChapter V: Relevant Information and Decision MakingBereket DesalegnNo ratings yet