You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Wereldleiders Op TwitterDocument24 pagesWereldleiders Op TwitterHerman CouwenberghNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- TRAI Data Till 31st March, 2014Document19 pagesTRAI Data Till 31st March, 2014Tamanna Bavishi ShahNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- NokiaDocument1 pageNokiaSumit RoyNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The State of Mobile Advertising in Emerging Countries TLS EmergingMarketsDocument8 pagesThe State of Mobile Advertising in Emerging Countries TLS EmergingMarketsSumit RoyNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Risk Factors From Hepatitis BCDDocument1 pageRisk Factors From Hepatitis BCDSumit RoyNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Mobile Advertising Research Trends and InsightsDocument15 pagesMobile Advertising Research Trends and InsightsSumit RoyNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Hepatitis A eDocument1 pageHepatitis A eSumit RoyNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Nightingales - Philips Healthcare Tie UpDocument3 pagesNightingales - Philips Healthcare Tie UpSumit RoyNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- World Health Days 2014: JanuaryDocument2 pagesWorld Health Days 2014: JanuaryIvy Jorene Roman RodriguezNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- Hepatitis A eDocument1 pageHepatitis A eSumit RoyNo ratings yet

- The State of Airline Marketing Airlinetrends Simpliflying April2013Document21 pagesThe State of Airline Marketing Airlinetrends Simpliflying April2013Sumit RoyNo ratings yet

- Calendário de Jogos Do Mundial de Futebol-Brasil 2014Document0 pagesCalendário de Jogos Do Mundial de Futebol-Brasil 2014Miguel RodriguesNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- FINAL - Mobile Advertising DeckDocument73 pagesFINAL - Mobile Advertising DecksumitkroyNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Global Top 100 Most Valueable Brands Brandz2014 - Infographic PDFDocument1 pageGlobal Top 100 Most Valueable Brands Brandz2014 - Infographic PDFSumit RoyNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The State of Maternal Health, D Nutrition in Asia " World Vision DataDocument4 pagesThe State of Maternal Health, D Nutrition in Asia " World Vision DataSumit RoyNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- World Health Statisitics FullDocument180 pagesWorld Health Statisitics FullClarice SalidoNo ratings yet

- Calendar 14Document57 pagesCalendar 14Hanan AhmedNo ratings yet

- Mediamind Comscore Research Dwelling On EntertainmentDocument20 pagesMediamind Comscore Research Dwelling On EntertainmentSumit RoyNo ratings yet

- MGI China E-Tailing Executive Summary March 2013Document18 pagesMGI China E-Tailing Executive Summary March 2013Sumit RoyNo ratings yet

- The 5 Free Alternatives To Microsoft WordDocument60 pagesThe 5 Free Alternatives To Microsoft WordSumit RoyNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- CEO Survey On Hiring, Profitability and PeopleDocument36 pagesCEO Survey On Hiring, Profitability and PeopleSumit RoyNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Evolution of Digital Advertising 3.0: Adobe Research InsightsDocument1 pageThe Evolution of Digital Advertising 3.0: Adobe Research InsightsSumit RoyNo ratings yet

- The 5 Free Alternatives To Microsoft WordDocument60 pagesThe 5 Free Alternatives To Microsoft WordSumit RoyNo ratings yet

- 2014 Bill and Melinda Gates Foundation Report On Global PovertyDocument28 pages2014 Bill and Melinda Gates Foundation Report On Global PovertySumit RoyNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

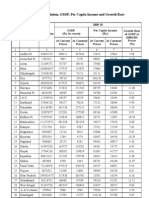

- Statewise GSDP PCI and G.RDocument3 pagesStatewise GSDP PCI and G.RArchit SingalNo ratings yet

- 10 Historical Speeches Nobody Ever HeardDocument20 pages10 Historical Speeches Nobody Ever HeardSumit Roy100% (1)

- Gender and Social Networking Activity :facebook Vs OthersDocument18 pagesGender and Social Networking Activity :facebook Vs OthersSumit RoyNo ratings yet

- CVD Atlas 16 Death From Stroke PDFDocument1 pageCVD Atlas 16 Death From Stroke PDFRisti KhafidahNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- India InfographicsDocument3 pagesIndia InfographicsSumit RoyNo ratings yet

- Report On Green PackagingDocument36 pagesReport On Green PackagingAayush Jain100% (2)

- ResumeDocument4 pagesResumeA-g ApolloNo ratings yet

- Introduction To International MarketingDocument17 pagesIntroduction To International MarketingMinhaz AhmedNo ratings yet

- Company Pitch Deck TemplateDocument11 pagesCompany Pitch Deck TemplateSamyak JainNo ratings yet

- Chapter 7. Perception, Motivation, Personality & EmotionDocument31 pagesChapter 7. Perception, Motivation, Personality & EmotionMichelle Danika MarquezNo ratings yet

- Principles of Management Chapter 4 GTU MBADocument22 pagesPrinciples of Management Chapter 4 GTU MBARushabh VoraNo ratings yet

- MBA Marketing Management (2 YearsDocument2 pagesMBA Marketing Management (2 YearsANo ratings yet

- Project Report On Sales Improv. of CCD-1Document81 pagesProject Report On Sales Improv. of CCD-1Ashish Yaduvanshi67% (3)

- Marketing ResearchDocument6 pagesMarketing ResearchSanket MaheshwariNo ratings yet

- Fresh Fruits & Veg Marketing Constraints & OpportunitiesDocument53 pagesFresh Fruits & Veg Marketing Constraints & OpportunitiesNgan TuyNo ratings yet

- Literature Review On SbiDocument2 pagesLiterature Review On SbiPRIYANKA VISHWAKARMA50% (2)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Kolářík 2013 BP PDFDocument71 pagesKolářík 2013 BP PDFsameer issaNo ratings yet

- Andiyappillai 2020 Ijais 451896Document5 pagesAndiyappillai 2020 Ijais 451896Christian CardiñoNo ratings yet

- ! Hays Romania Salary Guide 2023Document10 pages! Hays Romania Salary Guide 2023mada moiceanuNo ratings yet

- CB AuditDocument28 pagesCB AuditPavan Kuchar100% (2)

- BPLAN 4 Food ProcessingDocument54 pagesBPLAN 4 Food ProcessingTunde AjayiNo ratings yet

- ENGLISH - 20-21 - PR - Course Module (Theory 4)Document23 pagesENGLISH - 20-21 - PR - Course Module (Theory 4)daraNo ratings yet

- Customer Based Brand Equity of Sulfex MattressDocument78 pagesCustomer Based Brand Equity of Sulfex MattressJebin James75% (4)

- Social Commerce Foundations and Marketing StrategiesDocument29 pagesSocial Commerce Foundations and Marketing StrategiesShareene Ira100% (1)

- DissertationDocument95 pagesDissertationsriramsanjeev2sNo ratings yet

- Nombre No. Boleta: Administración EstratégicaDocument4 pagesNombre No. Boleta: Administración EstratégicaPedro ArroyoNo ratings yet

- Application of Demand and SupplyDocument25 pagesApplication of Demand and SupplyThriztan Andrei BaluyutNo ratings yet

- Cara Gregorius Resume 2020Document2 pagesCara Gregorius Resume 2020api-510443951No ratings yet

- Marketing ManagementDocument195 pagesMarketing ManagementweirdsmasterNo ratings yet

- Optimal inventory ordering policy for raw materialsDocument5 pagesOptimal inventory ordering policy for raw materials19R21A05C0 19 - CSE BNo ratings yet

- Shrink Wrapping Machine & Strapping Machine - Innovative MechatronicsDocument1 pageShrink Wrapping Machine & Strapping Machine - Innovative MechatronicsKuldeep PatelNo ratings yet

- UNIQLO Brand AnalysisDocument6 pagesUNIQLO Brand AnalysisMasrur Mustavi Omi100% (1)

- Azad Products Pvt. LTD.: Case StudyDocument6 pagesAzad Products Pvt. LTD.: Case StudyRomi SikderNo ratings yet

- Calculate Markup and VATDocument23 pagesCalculate Markup and VATWijdan Saleem EdwanNo ratings yet

- HistoryDocument57 pagesHistoryasmasultana_249No ratings yet

- $100M Leads: How to Get Strangers to Want to Buy Your StuffFrom Everand$100M Leads: How to Get Strangers to Want to Buy Your StuffRating: 5 out of 5 stars5/5 (12)

- $100M Offers: How to Make Offers So Good People Feel Stupid Saying NoFrom Everand$100M Offers: How to Make Offers So Good People Feel Stupid Saying NoRating: 5 out of 5 stars5/5 (20)

- Scientific Advertising: "Master of Effective Advertising"From EverandScientific Advertising: "Master of Effective Advertising"Rating: 4.5 out of 5 stars4.5/5 (163)

- Summary: Range: Why Generalists Triumph in a Specialized World by David Epstein: Key Takeaways, Summary & Analysis IncludedFrom EverandSummary: Range: Why Generalists Triumph in a Specialized World by David Epstein: Key Takeaways, Summary & Analysis IncludedRating: 4.5 out of 5 stars4.5/5 (6)

- How to Get a Meeting with Anyone: The Untapped Selling Power of Contact MarketingFrom EverandHow to Get a Meeting with Anyone: The Untapped Selling Power of Contact MarketingRating: 4.5 out of 5 stars4.5/5 (28)

- Understanding Digital Marketing: Marketing Strategies for Engaging the Digital GenerationFrom EverandUnderstanding Digital Marketing: Marketing Strategies for Engaging the Digital GenerationRating: 4 out of 5 stars4/5 (22)

- Dealers of Lightning: Xerox PARC and the Dawn of the Computer AgeFrom EverandDealers of Lightning: Xerox PARC and the Dawn of the Computer AgeRating: 4 out of 5 stars4/5 (88)

- Fascinate: How to Make Your Brand Impossible to ResistFrom EverandFascinate: How to Make Your Brand Impossible to ResistRating: 5 out of 5 stars5/5 (1)

- Obviously Awesome: How to Nail Product Positioning so Customers Get It, Buy It, Love ItFrom EverandObviously Awesome: How to Nail Product Positioning so Customers Get It, Buy It, Love ItRating: 4.5 out of 5 stars4.5/5 (150)