You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Leadership Traits and BehaviorsAdv. OB & Analysis(MBA- 532Document33 pagesLeadership Traits and BehaviorsAdv. OB & Analysis(MBA- 532tilahunthmNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- BSC 2Document28 pagesBSC 2tilahunthmNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- CamScanner 09-09-2022 11.09Document2 pagesCamScanner 09-09-2022 11.09tilahunthmNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Chapter 7: Designing Effective Organizations: By: Girma Tadesse, PH .DDocument28 pagesChapter 7: Designing Effective Organizations: By: Girma Tadesse, PH .DtilahunthmNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- BSC 1 PDFDocument17 pagesBSC 1 PDFNaod FishNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- ACM CH 1Document5 pagesACM CH 1tilahunthmNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Printout: Wednesday, July 20, 2022 11:23 PMDocument45 pagesPrintout: Wednesday, July 20, 2022 11:23 PMtilahunthmNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Wollo University, College of Business & Economics Department of Management: MBA Extension Program Course: Advanced Financial Management (MBA611)Document1 pageWollo University, College of Business & Economics Department of Management: MBA Extension Program Course: Advanced Financial Management (MBA611)tilahunthmNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- 2.1.1. Summary of Income StatementDocument2 pages2.1.1. Summary of Income StatementtilahunthmNo ratings yet

- Understanding Phase IinDocument35 pagesUnderstanding Phase IintilahunthmNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Ration Analysis Tilahun HailuDocument3 pagesRation Analysis Tilahun HailutilahunthmNo ratings yet

- BSC 4Document4 pagesBSC 4tilahunthmNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Wollo University, College of Business & Economics Department of Management: MBA Extension Program Course: Advanced Financial Management (MBA611)Document1 pageWollo University, College of Business & Economics Department of Management: MBA Extension Program Course: Advanced Financial Management (MBA611)tilahunthmNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- ACM CH 2Document3 pagesACM CH 2tilahunthmNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Business Process ReengineeringDocument33 pagesBusiness Process ReengineeringtilahunthmNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- BSC 5Document10 pagesBSC 5tilahunthmNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Exam QuestionsDocument13 pagesExam QuestionstilahunthmNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- BSC 3Document14 pagesBSC 3tilahunthmNo ratings yet

- What Is Money LaunderingDocument2 pagesWhat Is Money LaunderingtilahunthmNo ratings yet

- Note For ExamDocument38 pagesNote For ExamtilahunthmNo ratings yet

- Introduction To ManagementDocument98 pagesIntroduction To ManagementtilahunthmNo ratings yet

- BSC 1 PDFDocument17 pagesBSC 1 PDFNaod FishNo ratings yet

- Fundamentals Strategic Management 2nd Edition 2018 PDFDocument18 pagesFundamentals Strategic Management 2nd Edition 2018 PDFIbrahim Salahudin0% (1)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Internatinal MarketingDocument9 pagesInternatinal MarketingtilahunthmNo ratings yet

- E MailDocument84 pagesE MailtilahunthmNo ratings yet

- Woldia UniversityDocument1 pageWoldia UniversitytilahunthmNo ratings yet

- Ethiopian Law of PersonsDocument278 pagesEthiopian Law of Personstilahunthm89% (9)

- Excel 2013 Training Manual SEODocument257 pagesExcel 2013 Training Manual SEOtilahunthm94% (16)

- Module Public Asset PADocument125 pagesModule Public Asset PAtilahunthmNo ratings yet

- Econ Exam 3 PracticeDocument17 pagesEcon Exam 3 PracticeNickArnoukNo ratings yet

- 04 Task Performance 1Document6 pages04 Task Performance 1Hanna LyNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Effects On Textile Industry Due To Energy CrisisDocument8 pagesEffects On Textile Industry Due To Energy Crisismudassar jamil100% (2)

- Ananya Mukherjee-Reed - Perspectives On The Indian Corporate Economy - Exploring The Paradox of Profits (International Political Economy) (2001)Document249 pagesAnanya Mukherjee-Reed - Perspectives On The Indian Corporate Economy - Exploring The Paradox of Profits (International Political Economy) (2001)VENKY KRISHNANo ratings yet

- Economic Reforms in India Since 1991: An AppraisalDocument21 pagesEconomic Reforms in India Since 1991: An AppraisalShem W LyngdohNo ratings yet

- PublicEducationFunding ReportDocument118 pagesPublicEducationFunding ReportOKCFOXNo ratings yet

- ST Helena Tariff - Review - and - Justification - Paper - 2022-23Document18 pagesST Helena Tariff - Review - and - Justification - Paper - 2022-23Mark NabongNo ratings yet

- Ch.17 ENG-market FailureDocument35 pagesCh.17 ENG-market FailureCUBEC CHANGNo ratings yet

- A Discussion On The Roadmap For Public Higher Education Reform (RPHER)Document31 pagesA Discussion On The Roadmap For Public Higher Education Reform (RPHER)Angel Rose Trocio100% (2)

- What is a Central Bank in 40 CharactersDocument9 pagesWhat is a Central Bank in 40 CharactersJabree 3DNo ratings yet

- Alternatives To SprawlDocument36 pagesAlternatives To SprawlCallejasAlbinNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Chapter 2Document124 pagesChapter 2Cha Boon KitNo ratings yet

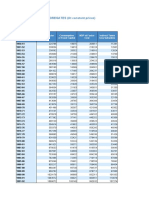

- HBS Table No. 02 - Macro Economic Aggregates (At Constant Prices)Document35 pagesHBS Table No. 02 - Macro Economic Aggregates (At Constant Prices)Anuj VermaNo ratings yet

- The Multifibre AgreementDocument40 pagesThe Multifibre AgreementVarun MehrotraNo ratings yet

- ISS22 PronelloDocument74 pagesISS22 PronelloAderito Raimundo MazuzeNo ratings yet

- Adda Leaf PlatesDocument5 pagesAdda Leaf PlatesSenkatuuka LukeNo ratings yet

- Reading 7 Economics of Regulation - AnswersDocument15 pagesReading 7 Economics of Regulation - Answerstristan.riolsNo ratings yet

- Agricultural FinanceDocument8 pagesAgricultural FinanceYayah Koroma100% (1)

- Marcopper Mining: Dealing with CSRDocument14 pagesMarcopper Mining: Dealing with CSRJose Mari DichosonNo ratings yet

- Introduction of International BusinessDocument42 pagesIntroduction of International Businesstrustme77100% (1)

- Karnataka MissionDocument67 pagesKarnataka MissionjalpathprathyuNo ratings yet

- Chapter 2 Theory of Demand and SupplyDocument25 pagesChapter 2 Theory of Demand and Supplyhidayatul raihanNo ratings yet

- The Cullman Times: Tornado Papers From Days Following April 27, 2011Document72 pagesThe Cullman Times: Tornado Papers From Days Following April 27, 2011Trent MooreNo ratings yet

- International BusinessDocument59 pagesInternational BusinessRizwan ZisanNo ratings yet

- Bçì Êçç QK Dçåò Äéò Åç Oçë Êáç Dêéöçêáç J Å Ë ÅDocument60 pagesBçì Êçç QK Dçåò Äéò Åç Oçë Êáç Dêéöçêáç J Å Ë ÅmarielNo ratings yet

- Quieter Homes: Reducing Aircraft Noise at Your PlaceDocument8 pagesQuieter Homes: Reducing Aircraft Noise at Your Placepauline_pabelloNo ratings yet

- Assam Development ReportDocument216 pagesAssam Development ReportnipjoyNo ratings yet

- Energy Transition and Renewable Energies: Challenges For Peru - Humberto Campodónico, Cesar CarreraDocument11 pagesEnergy Transition and Renewable Energies: Challenges For Peru - Humberto Campodónico, Cesar CarreratochisitoNo ratings yet

- CIR V SONY Case DigestDocument2 pagesCIR V SONY Case DigestAndrea TiuNo ratings yet

- Ib Economics - 1.10 Exam Practice Questions - SubsidiesDocument3 pagesIb Economics - 1.10 Exam Practice Questions - SubsidiesSOURAV MONDALNo ratings yet

- What Your CPA Isn't Telling You: Life-Changing Tax StrategiesFrom EverandWhat Your CPA Isn't Telling You: Life-Changing Tax StrategiesRating: 4 out of 5 stars4/5 (9)

- Tax Accounting: A Guide for Small Business Owners Wanting to Understand Tax Deductions, and Taxes Related to Payroll, LLCs, Self-Employment, S Corps, and C CorporationsFrom EverandTax Accounting: A Guide for Small Business Owners Wanting to Understand Tax Deductions, and Taxes Related to Payroll, LLCs, Self-Employment, S Corps, and C CorporationsRating: 4 out of 5 stars4/5 (1)

- Deduct Everything!: Save Money with Hundreds of Legal Tax Breaks, Credits, Write-Offs, and LoopholesFrom EverandDeduct Everything!: Save Money with Hundreds of Legal Tax Breaks, Credits, Write-Offs, and LoopholesRating: 3 out of 5 stars3/5 (3)

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet

- Small Business Taxes: The Most Complete and Updated Guide with Tips and Tax Loopholes You Need to Know to Avoid IRS Penalties and Save MoneyFrom EverandSmall Business Taxes: The Most Complete and Updated Guide with Tips and Tax Loopholes You Need to Know to Avoid IRS Penalties and Save MoneyNo ratings yet

- The Payroll Book: A Guide for Small Businesses and StartupsFrom EverandThe Payroll Book: A Guide for Small Businesses and StartupsRating: 5 out of 5 stars5/5 (1)

- How to get US Bank Account for Non US ResidentFrom EverandHow to get US Bank Account for Non US ResidentRating: 5 out of 5 stars5/5 (1)

- Tax Strategies: The Essential Guide to All Things Taxes, Learn the Secrets and Expert Tips to Understanding and Filing Your Taxes Like a ProFrom EverandTax Strategies: The Essential Guide to All Things Taxes, Learn the Secrets and Expert Tips to Understanding and Filing Your Taxes Like a ProRating: 4.5 out of 5 stars4.5/5 (43)