You might also like

- Tarrega - Capricho Arabe PDFDocument5 pagesTarrega - Capricho Arabe PDFPaul McagninNo ratings yet

- Getting Started - DropboxDocument6 pagesGetting Started - DropboxAnonymous Aeh0aDhF2No ratings yet

- Eula Microsoft Visual StudioDocument3 pagesEula Microsoft Visual StudioqwwerttyyNo ratings yet

- 2nd LanguageDocument1 page2nd LanguageGianfranco CavallaroNo ratings yet

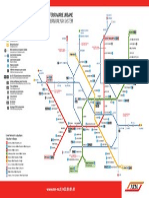

- Metro MilanoDocument1 pageMetro MilanoGianfranco CavallaroNo ratings yet

- Prelude BWV 999 (Bach-Bagterp)Document2 pagesPrelude BWV 999 (Bach-Bagterp)Gianfranco CavallaroNo ratings yet

- Metro MilanoDocument1 pageMetro MilanoGianfranco CavallaroNo ratings yet

- HDD Western Digital WD20EARSDocument4 pagesHDD Western Digital WD20EARSJoris De VreeseNo ratings yet

- Bourree (Bach Tampalini)Document1 pageBourree (Bach Tampalini)Gianfranco CavallaroNo ratings yet

- 2nd LanguageDocument1 page2nd LanguageGianfranco CavallaroNo ratings yet

- Quesito 1: Prova Scritta Valida Per Le Classi A345 e A346Document2 pagesQuesito 1: Prova Scritta Valida Per Le Classi A345 e A346Gianfranco CavallaroNo ratings yet

- Teaching Pronunciation: Using The Prosody Pyramid Judy B. GilbertDocument56 pagesTeaching Pronunciation: Using The Prosody Pyramid Judy B. GilbertSLavNo ratings yet

- Internal Hard Drives: Quick Install GuideDocument2 pagesInternal Hard Drives: Quick Install Guidekleber_maryNo ratings yet

- Promozioni Speciali Disponibili A Breve. Special Offers Soon Available. Sonderangebote Bald VerfügbarDocument1 pagePromozioni Speciali Disponibili A Breve. Special Offers Soon Available. Sonderangebote Bald VerfügbarGianfranco CavallaroNo ratings yet

- Codice Validità Da Validità Al Descrizione Points Contributo CDUDocument2 pagesCodice Validità Da Validità Al Descrizione Points Contributo CDUGianfranco CavallaroNo ratings yet

- Whitepaper Titanium 2012 and The Windows Firewall enDocument13 pagesWhitepaper Titanium 2012 and The Windows Firewall engreat602No ratings yet

- The All-In-One Solution For Internet ConnectivityDocument2 pagesThe All-In-One Solution For Internet ConnectivityBintan6No ratings yet

- 301.42 Nvidia Control Panel Quick Start GuideDocument31 pages301.42 Nvidia Control Panel Quick Start GuideMarcus MatsuyamaNo ratings yet

- HDD Western Digital WD20EARSDocument4 pagesHDD Western Digital WD20EARSJoris De VreeseNo ratings yet

- Ds Display l20t 3 LedDocument4 pagesDs Display l20t 3 LedGianfranco CavallaroNo ratings yet

- American LiteratureDocument179 pagesAmerican Literaturevittolivia92% (24)

- Creating Effective Language Lessons CombinedDocument50 pagesCreating Effective Language Lessons CombinedKubla KhanNo ratings yet

- Technical English 2 WBDocument82 pagesTechnical English 2 WBKaRen HeRnandezNo ratings yet

- Kh2025 - Ib - Receiver - Uk 01.04.2004 11:39 Uhr Seite 2: Kompernaß Handelsgesellschaft MBH Burgstraße 21 D-44867 BochumDocument22 pagesKh2025 - Ib - Receiver - Uk 01.04.2004 11:39 Uhr Seite 2: Kompernaß Handelsgesellschaft MBH Burgstraße 21 D-44867 BochumGianfranco CavallaroNo ratings yet

- Teaching English Using ICTDocument177 pagesTeaching English Using ICTGianfranco Cavallaro100% (2)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Credit Card BOA DuyDocument4 pagesCredit Card BOA Duynghia leNo ratings yet

- Itinerary Print PDF File Name CustomerDocument2 pagesItinerary Print PDF File Name CustomerBogdan George TeisanuNo ratings yet

- Victoria Chemical Case 20Document4 pagesVictoria Chemical Case 20Shahzad MughalNo ratings yet

- Saima Jabeen AkhandaDocument70 pagesSaima Jabeen AkhandaAhnaf AhmedNo ratings yet

- Levin Report - Correspondent Banking A Gateway For Money LaunderingDocument300 pagesLevin Report - Correspondent Banking A Gateway For Money Launderingapi-3807149100% (1)

- General Awareness MCQ New AugDocument7 pagesGeneral Awareness MCQ New AugManish SinghNo ratings yet

- Chap 008Document17 pagesChap 008Ela PelariNo ratings yet

- Designing Financial IncentivesDocument6 pagesDesigning Financial IncentivesPriyanka HarilelaNo ratings yet

- Industrial Finance Corp. v. TobiasDocument1 pageIndustrial Finance Corp. v. TobiasJennilyn TugelidaNo ratings yet

- Sports Hub Traffic BrochureDocument2 pagesSports Hub Traffic BrochureDavidLiNo ratings yet

- PartnershipDocument28 pagesPartnershipAdi Murthy100% (2)

- AcknowledgementDocument9 pagesAcknowledgementDeepika DedhiaNo ratings yet

- IC Accounting Journal Template Updated 8552Document6 pagesIC Accounting Journal Template Updated 8552MochdeedatShonhajiNo ratings yet

- Brenda Gaba 2021 Electronic Banking ProjectDocument49 pagesBrenda Gaba 2021 Electronic Banking ProjectsamuelNo ratings yet

- Global Trust BankDocument19 pagesGlobal Trust BankLawi Anupam33% (6)

- Form F - ODocument10 pagesForm F - ORobin RubinaNo ratings yet

- Extended Settlement PlanDocument3 pagesExtended Settlement PlanMadushike JayawickramaNo ratings yet

- Annual Report 2017 PDFDocument216 pagesAnnual Report 2017 PDFemmanuelNo ratings yet

- HSE Lesson17Document20 pagesHSE Lesson17SteeeeeeeephNo ratings yet

- World Soccer October 2017Document84 pagesWorld Soccer October 2017BhåvøöķWadhwa100% (1)

- Detailed StatementDocument2 pagesDetailed Statementnisha.yusuf.infNo ratings yet

- 2023 05 18 17 29 17feb 23 - 144009Document7 pages2023 05 18 17 29 17feb 23 - 144009Kapish BhallaNo ratings yet

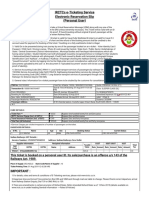

- Irctcs E-Ticketing Service Electronic Reservation Slip (Personal User)Document2 pagesIrctcs E-Ticketing Service Electronic Reservation Slip (Personal User)Sanjit SenNo ratings yet

- Functions of BanksDocument8 pagesFunctions of BanksRanjeetha Vivek05No ratings yet

- Financial Inclusion: A Study of Taking Banking Services To The Rural PopulationDocument21 pagesFinancial Inclusion: A Study of Taking Banking Services To The Rural PopulationRiddhi BhatiaNo ratings yet

- Asset Liability Management in BanksDocument8 pagesAsset Liability Management in BankscelesteNo ratings yet

- NABARDDocument46 pagesNABARDMahesh Gaddamedi100% (1)

- HSBC Company Analysis Grp4Document32 pagesHSBC Company Analysis Grp4rubaiNo ratings yet

- Canara Bank Specialist Officers Recruitment Sept 2010 Payment ChallanDocument1 pageCanara Bank Specialist Officers Recruitment Sept 2010 Payment ChallanmaneeshjNo ratings yet

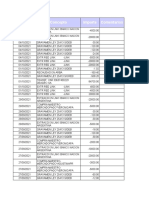

- Movimientos HistoricosDocument22 pagesMovimientos HistoricosVerónica RodNo ratings yet