You might also like

- Chapter 24 - Professional Money Management, Alternative Assets, and Industry EthicsDocument48 pagesChapter 24 - Professional Money Management, Alternative Assets, and Industry Ethicsrrrr110000No ratings yet

- SCA ALKO Case Study ReportDocument4 pagesSCA ALKO Case Study ReportRavidas KRNo ratings yet

- Sleepless L.A. - Case AnalysisDocument6 pagesSleepless L.A. - Case AnalysisSreenandan NambiarNo ratings yet

- IF Problems Arbitrage OpportunityDocument11 pagesIF Problems Arbitrage OpportunityChintakunta PreethiNo ratings yet

- Topic 1 The Investment EnvironmentDocument19 pagesTopic 1 The Investment EnvironmentDavid Adeabah Osafo100% (1)

- Group and Module Schedules for Money and Banking CourseDocument3 pagesGroup and Module Schedules for Money and Banking Coursetripathi.shantanu3778No ratings yet

- Banking CompaniesDocument68 pagesBanking CompaniesKiran100% (2)

- Understanding Working Capital Needs and Financing OptionsDocument66 pagesUnderstanding Working Capital Needs and Financing OptionsAamit KumarNo ratings yet

- Financial Management MCQs on Capital Budgeting, Risk AnalysisDocument17 pagesFinancial Management MCQs on Capital Budgeting, Risk Analysis19101977No ratings yet

- Investment Analysis and Portfolio Management AssignmentDocument1 pageInvestment Analysis and Portfolio Management AssignmentOumer ShaffiNo ratings yet

- Problems On MergerDocument7 pagesProblems On MergerSUNILABHI_APNo ratings yet

- MBA 631 Quantitative Analysis for Management Decision MakingDocument6 pagesMBA 631 Quantitative Analysis for Management Decision Makingwondimu teshomeNo ratings yet

- Security Analysis & Portfolio ManagementDocument45 pagesSecurity Analysis & Portfolio ManagementVignesh PrabhuNo ratings yet

- Approaches in Portfolio ConstructionDocument2 pagesApproaches in Portfolio Constructionnayakrajesh89No ratings yet

- Industry and Life Cycle AnalysisDocument31 pagesIndustry and Life Cycle AnalysisASK ME ANYTHING SMARTPHONENo ratings yet

- CH 6 Cost Volume Profit Revised Mar 18Document84 pagesCH 6 Cost Volume Profit Revised Mar 18beccafabbriNo ratings yet

- Holding Period & Expected Return With AnswersDocument2 pagesHolding Period & Expected Return With AnswersSiddhant AggarwalNo ratings yet

- Asset Allocation and Portfolio Selection ReviewDocument5 pagesAsset Allocation and Portfolio Selection ReviewDivya chandNo ratings yet

- CH 12. Risk Evaluation in Capital BudgetingDocument29 pagesCH 12. Risk Evaluation in Capital BudgetingN-aineel DesaiNo ratings yet

- Chapter 9: The Capital Asset Pricing ModelDocument6 pagesChapter 9: The Capital Asset Pricing ModelJohn FrandoligNo ratings yet

- Fundamental Analysis GuideDocument12 pagesFundamental Analysis GuidezaryNo ratings yet

- Understanding the Security Market Line (SML) /TITLEDocument9 pagesUnderstanding the Security Market Line (SML) /TITLEnasir abdulNo ratings yet

- Security Analysis & Portfolio Management Syllabus MBA III SemDocument1 pageSecurity Analysis & Portfolio Management Syllabus MBA III SemViraja GuruNo ratings yet

- Course Outline - International Business FinanceDocument4 pagesCourse Outline - International Business FinanceSnn News TubeNo ratings yet

- Chapter - 5 Long Term FinancingDocument6 pagesChapter - 5 Long Term FinancingmuzgunniNo ratings yet

- Oaf 624 Course OutlineDocument8 pagesOaf 624 Course OutlinecmgimwaNo ratings yet

- Internship Report Final PDFDocument88 pagesInternship Report Final PDFSumaiya islamNo ratings yet

- Security Analysis - Oct 08Document17 pagesSecurity Analysis - Oct 08lokeshgoyal200175% (4)

- Corporate Finance Current Papers of Final Term PDFDocument35 pagesCorporate Finance Current Papers of Final Term PDFZahid UsmanNo ratings yet

- Unit 2 Capital Budgeting Decisions: IllustrationsDocument4 pagesUnit 2 Capital Budgeting Decisions: IllustrationsJaya SwethaNo ratings yet

- 522 114 Solutions-4Document5 pages522 114 Solutions-4Mruga Pandya100% (3)

- Financial Derivatives and Risk Management ExplainedDocument1 pageFinancial Derivatives and Risk Management Explainedmm1979No ratings yet

- SFM Theory BookDocument33 pagesSFM Theory BookvishnuvermaNo ratings yet

- Marginal Costing and Profit PlanningDocument22 pagesMarginal Costing and Profit Planningdevika125790% (1)

- Chapter 7 - Portfolio inDocument12 pagesChapter 7 - Portfolio intemedebereNo ratings yet

- Answwr of Quiz 5 (MBA)Document2 pagesAnswwr of Quiz 5 (MBA)Wael_Barakat_3179No ratings yet

- Portfolio ManagementDocument40 pagesPortfolio ManagementSayaliRewaleNo ratings yet

- FinancialManagement MB013 QuestionDocument31 pagesFinancialManagement MB013 QuestionAiDLo50% (2)

- SFM - Forex - QuestionsDocument23 pagesSFM - Forex - QuestionsVishal SutarNo ratings yet

- SFM May 2015Document25 pagesSFM May 2015Prasanna SharmaNo ratings yet

- Digital Notes Financial ManagementDocument89 pagesDigital Notes Financial ManagementDHARANI PRIYANo ratings yet

- International Financial ManagementDocument17 pagesInternational Financial Managementatif hussainNo ratings yet

- Understanding Option Markets and StrategiesDocument36 pagesUnderstanding Option Markets and StrategiesTorreus AdhikariNo ratings yet

- Based On Session 5 - Responsibility Accounting & Transfer PricingDocument5 pagesBased On Session 5 - Responsibility Accounting & Transfer PricingMERINANo ratings yet

- Chapter 3Document45 pagesChapter 3Sarvagya Chaturvedi100% (1)

- Lecture 2 Behavioural Finance and AnomaliesDocument15 pagesLecture 2 Behavioural Finance and AnomaliesQamarulArifin100% (1)

- Mutual Fund Question BankDocument3 pagesMutual Fund Question BankarunvklplmNo ratings yet

- QP March2012 p1Document20 pagesQP March2012 p1Dhanushka Rajapaksha100% (1)

- CH 1 - Multinational Financial Management OverviewDocument4 pagesCH 1 - Multinational Financial Management OverviewMohamed HelmyNo ratings yet

- Derivatives Markets: Futures, Options & SwapsDocument20 pagesDerivatives Markets: Futures, Options & SwapsPatrick Earl T. PintacNo ratings yet

- UNIZIM ACCN Business Accounting Course OutlineDocument7 pagesUNIZIM ACCN Business Accounting Course OutlineEverjoice Chatora100% (1)

- How To Write A Ratio AnalysisDocument2 pagesHow To Write A Ratio AnalysisLe TanNo ratings yet

- 15MF02 Financial Derivatives Question BankDocument12 pages15MF02 Financial Derivatives Question BankDaksin PranauNo ratings yet

- Responsibility CentersDocument6 pagesResponsibility CentersNitesh Pandita100% (1)

- NBFI-Course Outline-2020Document2 pagesNBFI-Course Outline-2020Umair NadeemNo ratings yet

- Financial Markets and Institutions 1Document29 pagesFinancial Markets and Institutions 1Hamza Iqbal100% (1)

- Understanding Non-Banking Financial Companies (NBFCsDocument31 pagesUnderstanding Non-Banking Financial Companies (NBFCssagarkharpatilNo ratings yet

- Value Chain Management Capability A Complete Guide - 2020 EditionFrom EverandValue Chain Management Capability A Complete Guide - 2020 EditionNo ratings yet

- Corporate Finance AssignmentDocument5 pagesCorporate Finance AssignmentInam SwatiNo ratings yet

- Econf412 Finf313 Mids SDocument11 pagesEconf412 Finf313 Mids SArchita SrivastavaNo ratings yet

- MB0045Document6 pagesMB0045Shyam Pal Singh TomarNo ratings yet

- Dipu MedicalDocument1 pageDipu MedicalPranjit BhuyanNo ratings yet

- Business Law 1Document4 pagesBusiness Law 1Pranjit BhuyanNo ratings yet

- TZBT LRQCMG ONg DwoDocument6 pagesTZBT LRQCMG ONg DwoPranjit BhuyanNo ratings yet

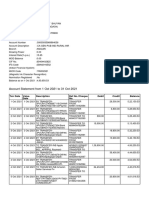

- Account Statement From 1 Nov 2021 To 30 Nov 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument4 pagesAccount Statement From 1 Nov 2021 To 30 Nov 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalancePranjit BhuyanNo ratings yet

- DiversificationDocument2 pagesDiversificationPranjit BhuyanNo ratings yet

- How To CrackDocument1 pageHow To CrackPranjit BhuyanNo ratings yet

- Equity and Hybrid InstrumentsDocument75 pagesEquity and Hybrid InstrumentsPranjit BhuyanNo ratings yet

- Management Information SystemDocument98 pagesManagement Information SystemPranjit BhuyanNo ratings yet

- HenyaDocument6 pagesHenyaKunnithi Sameunjai100% (1)

- Simply Put - ENT EAR LECTURE NOTESDocument48 pagesSimply Put - ENT EAR LECTURE NOTESCedric KyekyeNo ratings yet

- 50 Years of Teaching PianoDocument122 pages50 Years of Teaching PianoMyklan100% (35)

- Udaan: Under The Guidance of Prof - Viswanathan Venkateswaran Submitted By, Benila PaulDocument22 pagesUdaan: Under The Guidance of Prof - Viswanathan Venkateswaran Submitted By, Benila PaulBenila Paul100% (2)

- Catalogoclevite PDFDocument6 pagesCatalogoclevite PDFDomingo YañezNo ratings yet

- Unit 1 - Gear Manufacturing ProcessDocument54 pagesUnit 1 - Gear Manufacturing ProcessAkash DivateNo ratings yet

- Main Research PaperDocument11 pagesMain Research PaperBharat DedhiaNo ratings yet

- Fernandez ArmestoDocument10 pagesFernandez Armestosrodriguezlorenzo3288No ratings yet

- Describing-Jobs-British-English StudentDocument3 pagesDescribing-Jobs-British-English Studentrenata pedroso100% (1)

- Assignment 2 - Weather DerivativeDocument8 pagesAssignment 2 - Weather DerivativeBrow SimonNo ratings yet

- Coffee Table Book Design With Community ParticipationDocument12 pagesCoffee Table Book Design With Community ParticipationAJHSSR JournalNo ratings yet

- UNIT FOUR: Fundamentals of Marketing Mix: - Learning ObjectivesDocument49 pagesUNIT FOUR: Fundamentals of Marketing Mix: - Learning ObjectivesShaji ViswambharanNo ratings yet

- Neuropsychological Deficits in Disordered Screen Use Behaviours - A Systematic Review and Meta-AnalysisDocument32 pagesNeuropsychological Deficits in Disordered Screen Use Behaviours - A Systematic Review and Meta-AnalysisBang Pedro HattrickmerchNo ratings yet

- Difference Between Mark Up and MarginDocument2 pagesDifference Between Mark Up and MarginIan VinoyaNo ratings yet

- Krok2 - Medicine - 2010Document27 pagesKrok2 - Medicine - 2010Badriya YussufNo ratings yet

- Non Circumvention Non Disclosure Agreement (TERENCE) SGDocument7 pagesNon Circumvention Non Disclosure Agreement (TERENCE) SGLin ChrisNo ratings yet

- Case StudyDocument2 pagesCase StudyBunga Larangan73% (11)

- DMDW Mod3@AzDOCUMENTS - inDocument56 pagesDMDW Mod3@AzDOCUMENTS - inRakesh JainNo ratings yet

- Mission Ac Saad Test - 01 QP FinalDocument12 pagesMission Ac Saad Test - 01 QP FinalarunNo ratings yet

- Audit Acq Pay Cycle & InventoryDocument39 pagesAudit Acq Pay Cycle & InventoryVianney Claire RabeNo ratings yet

- Table of Specification for Pig Farming SkillsDocument7 pagesTable of Specification for Pig Farming SkillsYeng YengNo ratings yet

- Case Study Hotel The OrchidDocument5 pagesCase Study Hotel The Orchidkkarankapoor100% (4)

- Passenger E-Ticket: Booking DetailsDocument1 pagePassenger E-Ticket: Booking Detailsvarun.agarwalNo ratings yet

- Guiding Childrens Social Development and Learning 8th Edition Kostelnik Test BankDocument16 pagesGuiding Childrens Social Development and Learning 8th Edition Kostelnik Test Bankoglepogy5kobgk100% (27)

- Circular Flow of Process 4 Stages Powerpoint Slides TemplatesDocument9 pagesCircular Flow of Process 4 Stages Powerpoint Slides TemplatesAryan JainNo ratings yet

- Ir35 For Freelancers by YunojunoDocument17 pagesIr35 For Freelancers by YunojunoOlaf RazzoliNo ratings yet

- Level 3 Repair PBA Parts LayoutDocument32 pagesLevel 3 Repair PBA Parts LayoutabivecueNo ratings yet

- Inorganica Chimica Acta: Research PaperDocument14 pagesInorganica Chimica Acta: Research PaperRuan ReisNo ratings yet

- Nursing Care Management of a Client with Multiple Medical ConditionsDocument25 pagesNursing Care Management of a Client with Multiple Medical ConditionsDeannNo ratings yet