You might also like

- VBA Tutorial PDFDocument30 pagesVBA Tutorial PDFranaprathap_rpNo ratings yet

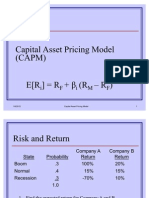

- Capital Asset Pricing ModelDocument25 pagesCapital Asset Pricing ModelAamit KumarNo ratings yet

- Project Management - CPM/PERT TechniquesDocument55 pagesProject Management - CPM/PERT TechniquesbhargavrapartiNo ratings yet

- Economic Survey 2010 Chapter 10Document37 pagesEconomic Survey 2010 Chapter 10Shaji MullookkaaranNo ratings yet

- Demographic Profile of DelhiDocument12 pagesDemographic Profile of DelhiLaxmi KeswaniNo ratings yet

- Brand Equity ArticlesDocument18 pagesBrand Equity ArticlesabhishkNo ratings yet

- Corporate Legal EnvironmentDocument26 pagesCorporate Legal Environmentabhishk0% (1)

- Industrial Visit To Hero HondaDocument14 pagesIndustrial Visit To Hero Hondaabhishk100% (8)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5782)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- NBP Funds: NBP Aitemaad Mahana Amdani Fund (NAMAF)Document1 pageNBP Funds: NBP Aitemaad Mahana Amdani Fund (NAMAF)Sajid rasoolNo ratings yet

- Birch Paper Company Box Bidding CaseDocument2 pagesBirch Paper Company Box Bidding CaseManish NarulaNo ratings yet

- Unit - 1 by Neha PandyaDocument30 pagesUnit - 1 by Neha Pandyarmnjbyjs5qNo ratings yet

- FSA Practise Questions & Indicative SolutionsDocument16 pagesFSA Practise Questions & Indicative SolutionsAmit YadavNo ratings yet

- Customer SurveyDocument40 pagesCustomer SurveySWATI SUMAN100% (1)

- RPH ModulesDocument5 pagesRPH ModulesGrace MendezNo ratings yet

- Investment Banking Spring 2021 Case Study #1 Mercury Athletic Footwear: Valuing The OpportunityDocument3 pagesInvestment Banking Spring 2021 Case Study #1 Mercury Athletic Footwear: Valuing The OpportunityRavi PatelNo ratings yet

- Common Mistakes On Claims For S14Q DeductionDocument2 pagesCommon Mistakes On Claims For S14Q DeductionHari ChandranNo ratings yet

- Group 6 - Case 2 - Apple INCDocument14 pagesGroup 6 - Case 2 - Apple INCrutuja gaikwadNo ratings yet

- Module 2-The Philippine Financial SystemDocument17 pagesModule 2-The Philippine Financial SystemRoliane LJ RugaNo ratings yet

- SAUDA DETAIL REPORT cl3618 PDFDocument1 pageSAUDA DETAIL REPORT cl3618 PDFPrachi PatwariNo ratings yet

- Dolphin Supplier Registration MandatoriesDocument3 pagesDolphin Supplier Registration MandatoriesSaheer AhamedNo ratings yet

- Caf-8 Cma PDFDocument5 pagesCaf-8 Cma PDFMuqtasid AhmedNo ratings yet

- 74-231 Quiz 2Document14 pages74-231 Quiz 2bitupon.sa108No ratings yet

- Smart Bangladesh - PDF Version 1Document2 pagesSmart Bangladesh - PDF Version 1Shaat Ronger Rongdhonu75% (4)

- Final Report JouharDocument67 pagesFinal Report JouharMuhammed Ali JouharNo ratings yet

- Birth Certificates are Federal Bank Notes: How to Reclaim Your Sovereign Citizen StatusDocument8 pagesBirth Certificates are Federal Bank Notes: How to Reclaim Your Sovereign Citizen StatusAngela Wigley100% (6)

- Implementation of Mgnrega Inkarnataka Issues and ChallengesDocument19 pagesImplementation of Mgnrega Inkarnataka Issues and ChallengesVENKY KRISHNANo ratings yet

- Lovelock Service Marketing Chapter 3Document41 pagesLovelock Service Marketing Chapter 3Mira100% (1)

- Chapter 11 Game Theory and Strategic Behavior: Topics To Be DiscussedDocument11 pagesChapter 11 Game Theory and Strategic Behavior: Topics To Be DiscussedMuhammad HassanNo ratings yet

- PWC Global Project Management Report SmallDocument40 pagesPWC Global Project Management Report SmallDaniel MoraNo ratings yet

- BTL tài chính doanh nghiệp mớiDocument19 pagesBTL tài chính doanh nghiệp mớiDo Hoang LanNo ratings yet

- Dr. Shilling Discusses Good Deflation and the Positive Impact of BPODocument4 pagesDr. Shilling Discusses Good Deflation and the Positive Impact of BPOYogita RaiNo ratings yet

- Principles of MicroeconomicDocument9 pagesPrinciples of MicroeconomicMohd Fadzly100% (1)

- SAMDS012136Document1 pageSAMDS012136amitNo ratings yet

- Accounts Receivable Collection PolicyDocument9 pagesAccounts Receivable Collection PolicyEuneze Lucas100% (1)

- Practice Set Review - Current LiabilitiesDocument12 pagesPractice Set Review - Current LiabilitiesKayla MirandaNo ratings yet

- Global Motor Market - Outlook 2020Document151 pagesGlobal Motor Market - Outlook 2020Mudit KediaNo ratings yet

- Department of Education PSIPOP 2022Document126 pagesDepartment of Education PSIPOP 2022Joshkorro GeronimoNo ratings yet