You might also like

- General Principles of LendingDocument3 pagesGeneral Principles of LendingSNo ratings yet

- Introduction To T24 - Treasury - R10.1Document34 pagesIntroduction To T24 - Treasury - R10.1Gnana Sambandam50% (2)

- Loans & Advances - Indian Banking LawDocument105 pagesLoans & Advances - Indian Banking LawNeed Notknow100% (1)

- Delinquency ManagementDocument4 pagesDelinquency ManagementJeff SmithNo ratings yet

- Credit Appraisal System of Commercial Vehicle Loans.Document43 pagesCredit Appraisal System of Commercial Vehicle Loans.Pravin Kolpe92% (12)

- Loan Disbursement and Recovery Procedures of BKBDocument10 pagesLoan Disbursement and Recovery Procedures of BKBFarhanChowdhuryMehdiNo ratings yet

- Credit Management - A Conceptual FrameworkDocument30 pagesCredit Management - A Conceptual Frameworkeknath200050% (2)

- 2019 Mock Exam A Morning Session With Solutionspdf 3 PDF FreeDocument51 pages2019 Mock Exam A Morning Session With Solutionspdf 3 PDF FreeThomas JosephNo ratings yet

- AnswerDocument8 pagesAnswerJericho PedragosaNo ratings yet

- Econet Wireless H1 2014 Presentation PDFDocument36 pagesEconet Wireless H1 2014 Presentation PDFKristi DuranNo ratings yet

- Credit AppraisalDocument6 pagesCredit AppraisalAnjali Angel ThakurNo ratings yet

- SCFS Cooperative Bank LTDDocument64 pagesSCFS Cooperative Bank LTDLïkïth RäjNo ratings yet

- CHAPTER I Principles of Lending Types of Credit FacilitiesDocument6 pagesCHAPTER I Principles of Lending Types of Credit Facilitiesanand.action0076127No ratings yet

- Unit-II - nOTESDocument20 pagesUnit-II - nOTESMohammad ShahvanNo ratings yet

- Credit ManagementDocument4 pagesCredit ManagementAnshUl SharMaNo ratings yet

- Credit Management CHAPTER 1Document23 pagesCredit Management CHAPTER 1Tokib TowfiqNo ratings yet

- Unit 2 Trade Credit RiskDocument15 pagesUnit 2 Trade Credit Risksaurabh thakurNo ratings yet

- Unit 8Document8 pagesUnit 8rtrsujaladhikariNo ratings yet

- Credit Risk AssessmentDocument8 pagesCredit Risk Assessmentmahita_m4a3081No ratings yet

- Loan Management SystemDocument28 pagesLoan Management SystemSrihari Prasad100% (1)

- FM 05 Unit IDocument9 pagesFM 05 Unit IMO. SHAHVANNo ratings yet

- Types of Credit Instruments & Its FeaturesDocument22 pagesTypes of Credit Instruments & Its Featuresninpra94% (18)

- Chapter 4 Loans and AdvancesDocument36 pagesChapter 4 Loans and AdvancesHeena DhingraNo ratings yet

- Chapter 1Document49 pagesChapter 1Sami JattNo ratings yet

- 2 Principles+of+LendingDocument25 pages2 Principles+of+LendingBratati SahooNo ratings yet

- Credit Management Comprises Two Aspects. These AreDocument3 pagesCredit Management Comprises Two Aspects. These Arevivekananda RoyNo ratings yet

- Topic 3 - CREDIT MANAGEMENTDocument43 pagesTopic 3 - CREDIT MANAGEMENTeogollaNo ratings yet

- Unit II: Banking Products and Services (Credit Facility)Document38 pagesUnit II: Banking Products and Services (Credit Facility)darshan lamaNo ratings yet

- Funded & Non-Funded FacilitiesDocument3 pagesFunded & Non-Funded Facilitiesbhavin shahNo ratings yet

- Bank Lending and Credit A DministrationDocument5 pagesBank Lending and Credit A Dministrationolikagu patrickNo ratings yet

- Good LendingDocument35 pagesGood LendingSirsanath Banerjee100% (7)

- Non Performing Assets (Npa)Document16 pagesNon Performing Assets (Npa)Avin P RNo ratings yet

- Unit 1 Finacial CreditDocument21 pagesUnit 1 Finacial Creditsaurabh thakurNo ratings yet

- CRM Unit 1 (Autosaved) (Autosaved)Document54 pagesCRM Unit 1 (Autosaved) (Autosaved)Sanjeela JoshiNo ratings yet

- Question & Answer On CreditDocument60 pagesQuestion & Answer On CreditSubarna palNo ratings yet

- Devaiya Nikhil LDRP - Itr MbaDocument5 pagesDevaiya Nikhil LDRP - Itr MbaKaushik PatelNo ratings yet

- Credit Appraisal Process & Financial ParametersDocument35 pagesCredit Appraisal Process & Financial ParametersAbhishek Barman100% (1)

- Chapter 3Document10 pagesChapter 3Ahmad Kabir MaikanoNo ratings yet

- 202 FM Cha 3 BDocument52 pages202 FM Cha 3 BKrishna JadhavNo ratings yet

- Pamantasan NG Lungsod NG Maynila PLM Business School A.Y. 2020 - 2021 First Semester Fin 3104: Credit Management and Collection PoliciesDocument29 pagesPamantasan NG Lungsod NG Maynila PLM Business School A.Y. 2020 - 2021 First Semester Fin 3104: Credit Management and Collection PoliciesHarlene BulaongNo ratings yet

- Note On Bank Loans-SummaryDocument7 pagesNote On Bank Loans-Summaryscbihari1186No ratings yet

- Credit Appraisal TechniquesDocument9 pagesCredit Appraisal TechniquesMragank Dixit0% (2)

- UNIT-5Financial Credit Risk AnalyticsDocument27 pagesUNIT-5Financial Credit Risk Analyticsblack canvasNo ratings yet

- UNIT 2 Process and DocumentationDocument27 pagesUNIT 2 Process and DocumentationAroop PalNo ratings yet

- G. Bhavana Types Loans - BajajDocument51 pagesG. Bhavana Types Loans - BajajNaveen KNo ratings yet

- Receivable ManagementDocument6 pagesReceivable Managementabdul samadNo ratings yet

- Credit Rating:: Working Capital LoansDocument7 pagesCredit Rating:: Working Capital Loansdon faperNo ratings yet

- Credit ManagementDocument46 pagesCredit ManagementMohammed ShaffanNo ratings yet

- Unit 5 Credit Analysis & RatingDocument29 pagesUnit 5 Credit Analysis & Ratingsaurabh thakurNo ratings yet

- Credit Process and Credit Appraisal of A CommercialDocument26 pagesCredit Process and Credit Appraisal of A CommercialLiza Ahmed100% (2)

- MBF - Unit 4 5Document11 pagesMBF - Unit 4 5Sachin TiwariNo ratings yet

- Lending Portfolio of BankDocument5 pagesLending Portfolio of BankMahi MaheshNo ratings yet

- Unit I MBF22408T Credit Risk and Recovery ManagementDocument17 pagesUnit I MBF22408T Credit Risk and Recovery ManagementSheetal DwevediNo ratings yet

- Full Notes MBF22408T Credit Risk and Recovery ManagementDocument90 pagesFull Notes MBF22408T Credit Risk and Recovery ManagementSheetal DwevediNo ratings yet

- Create A Pictorial Representation On The Five C Principles of Lendi - 20240401 - 110846 - 0000Document11 pagesCreate A Pictorial Representation On The Five C Principles of Lendi - 20240401 - 110846 - 0000mohankumar12tha1No ratings yet

- Money & Banking Mix TopicsDocument35 pagesMoney & Banking Mix TopicsAAMINA ZAFARNo ratings yet

- Ibf Assignment 3Document4 pagesIbf Assignment 3Zaroon KhanNo ratings yet

- Chapter 1: The Principles of Lending and Lending BasicsDocument5 pagesChapter 1: The Principles of Lending and Lending Basicshesham zakiNo ratings yet

- Financing Working Capital - Naveen SavitaDocument7 pagesFinancing Working Capital - Naveen SavitaMurli SavitaNo ratings yet

- Easy Guide to Building a Good Credit Score: Personal Finance, #3From EverandEasy Guide to Building a Good Credit Score: Personal Finance, #3No ratings yet

- Venture Capital: Rajendran Ananda KrishnanDocument32 pagesVenture Capital: Rajendran Ananda KrishnanSnisha YadavNo ratings yet

- Objective of The ProjectDocument2 pagesObjective of The ProjectSnisha YadavNo ratings yet

- Project ManagementDocument3 pagesProject ManagementSnisha YadavNo ratings yet

- General ElectricDocument15 pagesGeneral ElectricSnisha Yadav100% (1)

- Capital Structure 1227282765096005 8Document10 pagesCapital Structure 1227282765096005 8Snisha YadavNo ratings yet

- Role of Marketing Research (MR)Document9 pagesRole of Marketing Research (MR)Snisha YadavNo ratings yet

- "A Study of Agriculture Loan" Vividh Karyakari Seva Sahkari Society Ltd. DingoreDocument34 pages"A Study of Agriculture Loan" Vividh Karyakari Seva Sahkari Society Ltd. Dingorespiritual pfiNo ratings yet

- Sbi, 1Q Fy 2014Document14 pagesSbi, 1Q Fy 2014Angel BrokingNo ratings yet

- Terms in This SetDocument3 pagesTerms in This SetAccounting MaterialsNo ratings yet

- JohnsonDocument12 pagesJohnsonJannah Victoria AmoraNo ratings yet

- 3AB3S10Document8 pages3AB3S10Jason TangNo ratings yet

- Chapter 9 & 10Document2 pagesChapter 9 & 10atikah darayaniNo ratings yet

- Lecture Notes On Quasi-ReorganizationDocument2 pagesLecture Notes On Quasi-ReorganizationalyssaNo ratings yet

- ResumeDocument4 pagesResumeapi-3826517No ratings yet

- List of Ledgers Group in TallyDocument8 pagesList of Ledgers Group in TallyAMIT KUMARNo ratings yet

- Fintech: Foundations & Applications of Financial Technology: Divyansh SehgalDocument1 pageFintech: Foundations & Applications of Financial Technology: Divyansh SehgalDivyansh SehgalNo ratings yet

- BP'S Office of The Chief Technology Officer (A) : Driving Open Innovation Through An Advocate TeamDocument2 pagesBP'S Office of The Chief Technology Officer (A) : Driving Open Innovation Through An Advocate TeamsruthiNo ratings yet

- Portfolio ManagementDocument36 pagesPortfolio Managementrajujaipur1234No ratings yet

- M&a Case Study - Amazon and ZapposDocument5 pagesM&a Case Study - Amazon and ZapposJack Jacinto0% (1)

- Derivatives - Basics Types and UsesDocument5 pagesDerivatives - Basics Types and Usesgoel76vishalNo ratings yet

- Portfolio Management Portfolio Management Portfolio ManagementDocument4 pagesPortfolio Management Portfolio Management Portfolio ManagementAbhishek MishraNo ratings yet

- Layman's Guide To Pair TradingDocument9 pagesLayman's Guide To Pair TradingaporatNo ratings yet

- SAR-MAR-210422-1227PM - RR - 034-COPY 1.editedDocument12 pagesSAR-MAR-210422-1227PM - RR - 034-COPY 1.editedJishnu ChaudhuriNo ratings yet

- Particulars Opening Capital 2,00,000 Closing Capital 2,50,000 Drawings Made During The Year 60,000 Capital Added During The Year 75,000Document3 pagesParticulars Opening Capital 2,00,000 Closing Capital 2,50,000 Drawings Made During The Year 60,000 Capital Added During The Year 75,000Somasundaram ANo ratings yet

- Accreditation of Auditing FirmDocument2 pagesAccreditation of Auditing FirmGilbert AguillonNo ratings yet

- A Dissertation On InvestmentDocument108 pagesA Dissertation On InvestmentPrakash SinghNo ratings yet

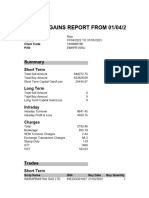

- Capital Gains - Stocks-GrowwDocument11 pagesCapital Gains - Stocks-Growwriyagupta10122000No ratings yet

- Crowdfunding: Online Charity or A Modern Tool For Innovative Projects Implementation?Document6 pagesCrowdfunding: Online Charity or A Modern Tool For Innovative Projects Implementation?ksatria juniNo ratings yet

- Selecting Entry ModeDocument22 pagesSelecting Entry ModeandiNo ratings yet

- Omar Halabieh's Review of Market WizardsDocument2 pagesOmar Halabieh's Review of Market Wizardsmytemp_01No ratings yet

- Dividend PolicyDocument52 pagesDividend PolicyANISH KUMARNo ratings yet

- Mono 1Document5 pagesMono 1Novais paulaNo ratings yet