You might also like

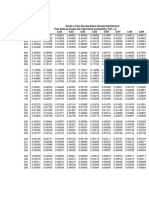

- Table For Standardised Normal DistributionDocument1 pageTable For Standardised Normal DistributionTheo SiafakasNo ratings yet

- Table For Standardised Normal DistributionDocument1 pageTable For Standardised Normal DistributionTheo SiafakasNo ratings yet

- Berstein, Jake - Introduction To Technical AnalysisDocument104 pagesBerstein, Jake - Introduction To Technical AnalysisTheo SiafakasNo ratings yet

- Essential MATLAB For Engineers and Scientists - Brian D. Hahn & Daniel T. ValentineDocument102 pagesEssential MATLAB For Engineers and Scientists - Brian D. Hahn & Daniel T. Valentinegagansingh87No ratings yet

- Outline of Business PlanDocument3 pagesOutline of Business PlanCoCo MaLuNo ratings yet

- DOE Mechanical Science Volume 2 of 2 DOE-HDBK-10182-93Document130 pagesDOE Mechanical Science Volume 2 of 2 DOE-HDBK-10182-93Titer100% (1)

- Economics - MacroeconomicsDocument122 pagesEconomics - MacroeconomicsChristina C ChNo ratings yet

- Modern Physics For Engineers ReviewDocument22 pagesModern Physics For Engineers Reviewpck87No ratings yet

- Motion Control HandbookDocument38 pagesMotion Control Handbookvincentttt100% (1)

- Essential MATLAB For Engineers and Scientists - Brian D. Hahn & Daniel T. ValentineDocument102 pagesEssential MATLAB For Engineers and Scientists - Brian D. Hahn & Daniel T. Valentinegagansingh87No ratings yet

- Materials Science 2 - DOEDocument112 pagesMaterials Science 2 - DOEshiv_1987No ratings yet

- DOE Fundamentals Handbook, Mechanical Science, Volume 1 of 2Document122 pagesDOE Fundamentals Handbook, Mechanical Science, Volume 1 of 2Bob VinesNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Rex - O. Ed. Wagner - W-Waves - BiocommDocument13 pagesRex - O. Ed. Wagner - W-Waves - BiocommLeon BlažinovićNo ratings yet

- Yokogawa 2015 Centum VP For Batch ControlDocument9 pagesYokogawa 2015 Centum VP For Batch ControlArzymanNo ratings yet

- CH3 SolutionsDocument40 pagesCH3 SolutionsRonelNo ratings yet

- Oscillation MCQDocument7 pagesOscillation MCQUmer KhalidNo ratings yet

- TC 1800 QI 1 1 0 (User Manual)Document25 pagesTC 1800 QI 1 1 0 (User Manual)Emman JimenezNo ratings yet

- Bar BendingDocument142 pagesBar Bendingjaffna100% (4)

- Manual LDM5 U enDocument3 pagesManual LDM5 U enLuizAugustoMedeirosNo ratings yet

- Phase Shift of 180 Degrees On Reflection From Optically Denser MediumDocument1 pagePhase Shift of 180 Degrees On Reflection From Optically Denser MediumGreato HibernatoNo ratings yet

- Hysys For Aspen Plus Users PDFDocument11 pagesHysys For Aspen Plus Users PDFKarim KholeifNo ratings yet

- CO2 Dosing and Generation SystemDocument344 pagesCO2 Dosing and Generation SystemABAID ULLAHNo ratings yet

- Cessna 172Document4 pagesCessna 172James DeatoNo ratings yet

- Abstract Load Balancing 1Document3 pagesAbstract Load Balancing 1Naveen AbhiNo ratings yet

- 1 Gauss SeidelDocument20 pages1 Gauss SeidelYanes Kristianus HediNo ratings yet

- J Gen Physiol-1952-Hershey-39-56Document18 pagesJ Gen Physiol-1952-Hershey-39-56api-277839406No ratings yet

- DocDocument6 pagesDocapi-287506055No ratings yet

- TIMO Mock 2019 卷P3fDocument9 pagesTIMO Mock 2019 卷P3fDo Yun100% (1)

- Smartdek Design ManualDocument48 pagesSmartdek Design ManualranddyNo ratings yet

- Na2xckbr2y Rev 08Document1 pageNa2xckbr2y Rev 08dardakNo ratings yet

- Wilo Fire Fighting BrochureDocument20 pagesWilo Fire Fighting BrochureAkhmad Darmaji DjamhuriNo ratings yet

- Tool Geometry and Tool LifeDocument29 pagesTool Geometry and Tool LifeSudeepHandikherkarNo ratings yet

- Friction Clutches 2020 CompressedDocument14 pagesFriction Clutches 2020 Compressedfikadu435No ratings yet

- Electrochemical Cleaningof Artificially Tarnished SilverDocument11 pagesElectrochemical Cleaningof Artificially Tarnished SilverRahmi Nur Anisah Nasution 2003114489No ratings yet

- Quarter3 Week4 ClimateDocument11 pagesQuarter3 Week4 ClimateJohn EdselNo ratings yet

- Solution of Problem Set 1 For Purity Hydrocarbon Data PDFDocument4 pagesSolution of Problem Set 1 For Purity Hydrocarbon Data PDFDrumil TrivediNo ratings yet

- 1956 - Colinese - Boiler Efficiencies in SugarDocument7 pages1956 - Colinese - Boiler Efficiencies in SugarPaul DurkinNo ratings yet

- Signal and Telecommunication - 1Document83 pagesSignal and Telecommunication - 1srinathNo ratings yet

- Testing The AdapterDocument8 pagesTesting The AdapterrejnanNo ratings yet

- Network Termination Unit STU4: Suppor Ting SHDSL - BisDocument2 pagesNetwork Termination Unit STU4: Suppor Ting SHDSL - BisНатальяNo ratings yet

- Quad Encoder Velocity Accel with CRIOLabVIEW FPGADocument5 pagesQuad Encoder Velocity Accel with CRIOLabVIEW FPGAChâu Tinh TrìNo ratings yet

- Info Iec62271-1Document28 pagesInfo Iec62271-1RichardLemusNo ratings yet