You might also like

- The Magnificent 10 For Men by MrLocario-1Document31 pagesThe Magnificent 10 For Men by MrLocario-1Mauricio Cesar Molina Arteta100% (1)

- Present Tense Exercises. Polish A1Document6 pagesPresent Tense Exercises. Polish A1Pilar Moreno DíezNo ratings yet

- Contracts, Biddings and Tender:Rule of ThumbFrom EverandContracts, Biddings and Tender:Rule of ThumbRating: 5 out of 5 stars5/5 (1)

- Estimating Engineering Hours from Project DataDocument9 pagesEstimating Engineering Hours from Project DataMartín Diego MastandreaNo ratings yet

- The Law of SchedulesDocument15 pagesThe Law of ScheduleshusktechNo ratings yet

- Standard BoQ (UAE - DoT) - CESMM4 PDFDocument554 pagesStandard BoQ (UAE - DoT) - CESMM4 PDFNektarios Matheou86% (44)

- Contract Administration Pitfalls and Solutions for Architect-Engineering Projects: A JournalFrom EverandContract Administration Pitfalls and Solutions for Architect-Engineering Projects: A JournalNo ratings yet

- Contract Strategies for Major Projects: Mastering the Most Difficult Element of Project ManagementFrom EverandContract Strategies for Major Projects: Mastering the Most Difficult Element of Project ManagementNo ratings yet

- Contract Strategy For Design Management in The Design and Build SystemDocument10 pagesContract Strategy For Design Management in The Design and Build SystemchouszeszeNo ratings yet

- Construction Law in the United Arab Emirates and the GulfFrom EverandConstruction Law in the United Arab Emirates and the GulfRating: 4 out of 5 stars4/5 (1)

- A Practical Guide to Disruption and Productivity Loss on Construction and Engineering ProjectsFrom EverandA Practical Guide to Disruption and Productivity Loss on Construction and Engineering ProjectsRating: 5 out of 5 stars5/5 (1)

- Aace International's: Certified Forensic Claim Consultant™ (CFCC™) Certification Study GuideDocument20 pagesAace International's: Certified Forensic Claim Consultant™ (CFCC™) Certification Study GuideKhaled AbdelbakiNo ratings yet

- Managing Risk in EPC ContractsDocument20 pagesManaging Risk in EPC ContractspoundingNo ratings yet

- Bioassay Techniques For Drug Development by Atta-Ur RahmanDocument214 pagesBioassay Techniques For Drug Development by Atta-Ur RahmanEmpress_MaripossaNo ratings yet

- AACE International - Certification Paper - 52284Document37 pagesAACE International - Certification Paper - 52284fareed_imadiNo ratings yet

- 10 Things To Know About FidicDocument7 pages10 Things To Know About FidicJaswin JonsonNo ratings yet

- Simple Format Construction ClaimsDocument3 pagesSimple Format Construction ClaimspanjemadjoNo ratings yet

- FIDIC Sub-Clause 3.5 ExplainedDocument9 pagesFIDIC Sub-Clause 3.5 ExplainedYashveer TakooryNo ratings yet

- Assessing Extension of Time Delays on Major ProjectsDocument20 pagesAssessing Extension of Time Delays on Major ProjectsSiawYenNo ratings yet

- SCL - Delay Disruption Protocol 2nd Edition by CM (R5)Document31 pagesSCL - Delay Disruption Protocol 2nd Edition by CM (R5)ILTERIS DOGAN100% (1)

- Allocating Risk in An EPC Contract - Patricia GallowayDocument13 pagesAllocating Risk in An EPC Contract - Patricia Gallowayjorge plaNo ratings yet

- Commentary:: Amending Clause 13.1 of FIDIC - Protracted NegotiationsDocument2 pagesCommentary:: Amending Clause 13.1 of FIDIC - Protracted NegotiationsArshad MahmoodNo ratings yet

- Risk Allocations in Construction ContractsDocument10 pagesRisk Allocations in Construction ContractsMdms PayoeNo ratings yet

- Engineering, Procurement and Construction (ECP) ContractsDocument124 pagesEngineering, Procurement and Construction (ECP) ContractsPopeyeNo ratings yet

- Toc - 44r-08 - Risk Analysis RangDocument4 pagesToc - 44r-08 - Risk Analysis RangdeeptiNo ratings yet

- Introduction To FIDIC Conditions of Contract: Dr. Mirosław J. Skibniewski, A.J. Clark Chair ProfessorDocument46 pagesIntroduction To FIDIC Conditions of Contract: Dr. Mirosław J. Skibniewski, A.J. Clark Chair ProfessorNeni Sumiatty100% (1)

- Case Study of Delay Impact Analysis of Lost Productivity in Construction ProjectsDocument2 pagesCase Study of Delay Impact Analysis of Lost Productivity in Construction ProjectsGeorge NunesNo ratings yet

- FCCMDocument2 pagesFCCMMohanna Govind100% (1)

- Cornes and Lupton's Design Liability in the Construction IndustryFrom EverandCornes and Lupton's Design Liability in the Construction IndustryNo ratings yet

- Introduction To FIDIC Dispute Adjudication Board Provisions (Owen - 2004)Document61 pagesIntroduction To FIDIC Dispute Adjudication Board Provisions (Owen - 2004)shady_sherif100% (3)

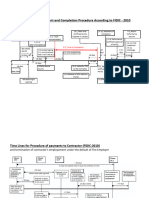

- Flow Charts of FIDIC-2010Document7 pagesFlow Charts of FIDIC-2010Irshad Ali Durrani100% (1)

- Fidic Variation PDFDocument268 pagesFidic Variation PDFjohnpaul100% (1)

- EPC Vs EPCMDocument4 pagesEPC Vs EPCMNemanja KlisaraNo ratings yet

- FIDIC delay and disruption standardsDocument7 pagesFIDIC delay and disruption standardsMohammad FayazNo ratings yet

- Pacing DelayDocument5 pagesPacing DelayChelimilla Ranga ReddyNo ratings yet

- Deciding JCT Contract PDFDocument43 pagesDeciding JCT Contract PDFchamil_dananjayaNo ratings yet

- Does Better Scheduling Drive Execution Success?Document9 pagesDoes Better Scheduling Drive Execution Success?AcumenNo ratings yet

- Fidic UpdateDocument3 pagesFidic Updatefhsn84No ratings yet

- Guide To FIDIC EPC ConditionsDocument35 pagesGuide To FIDIC EPC ConditionsZiad Zouheir Namani100% (1)

- Mega Project Construction Contracts - An Owner's PerspectiveDocument16 pagesMega Project Construction Contracts - An Owner's Perspectivesevero97No ratings yet

- Construction Claims and Responses: Effective Writing and PresentationFrom EverandConstruction Claims and Responses: Effective Writing and PresentationNo ratings yet

- Increased Size: FIDIC Redbook 2017 Vs 99 - Top 11 ChangesDocument3 pagesIncreased Size: FIDIC Redbook 2017 Vs 99 - Top 11 ChangesDangi DilleeRamNo ratings yet

- Gemmell - R - The Quantification of Loss Caused by Disruption - Thomson Reuters - 31 BCL 390Document17 pagesGemmell - R - The Quantification of Loss Caused by Disruption - Thomson Reuters - 31 BCL 390Jijo PjNo ratings yet

- Sub-Clause 4.7 - Notice of Items of Reference For Setting OutDocument2 pagesSub-Clause 4.7 - Notice of Items of Reference For Setting Outkhiem44No ratings yet

- Fidic - Condictions of Contract For Epc-Turnkey ProjectsDocument49 pagesFidic - Condictions of Contract For Epc-Turnkey Projectssharon gradosNo ratings yet

- Drafting EPC Contract TermsDocument8 pagesDrafting EPC Contract Termsaugustaq100% (2)

- Construction Claim - ILQ - Fall - 2014Document72 pagesConstruction Claim - ILQ - Fall - 2014A SetiadiNo ratings yet

- Vdocuments - MX Fidic Conditions of Contract For Underground Works U 2019 Athe Emerald BookDocument43 pagesVdocuments - MX Fidic Conditions of Contract For Underground Works U 2019 Athe Emerald Bookshengkai zhangNo ratings yet

- An Introduction To FIDIC and FIDIC Contract BooksDocument15 pagesAn Introduction To FIDIC and FIDIC Contract Booksaniket100% (1)

- The Prevention Principle After Muliplex V HoneywellDocument11 pagesThe Prevention Principle After Muliplex V HoneywellbarryroNo ratings yet

- ..AACE InternationalDocument3 pages..AACE International891966No ratings yet

- Contract Administration GuildlinesDocument117 pagesContract Administration GuildlinesEslam Ashour100% (1)

- The NEC4 Engineering and Construction Contract: A CommentaryFrom EverandThe NEC4 Engineering and Construction Contract: A CommentaryNo ratings yet

- A Comparison of NEC and FIDIC by Rob GerrardDocument4 pagesA Comparison of NEC and FIDIC by Rob GerrardbappanaduNo ratings yet

- LIQUIDATED-DAMAGES-Case Studies-Anamul HoqueDocument11 pagesLIQUIDATED-DAMAGES-Case Studies-Anamul HoqueMuhammad Anamul HoqueNo ratings yet

- Symphonological Bioethical Theory: Gladys L. Husted and James H. HustedDocument13 pagesSymphonological Bioethical Theory: Gladys L. Husted and James H. HustedYuvi Rociandel Luardo100% (1)

- EPC or EPCM Contracts: Which One Can Drive Stronger Outcomes For Project Owners?Document7 pagesEPC or EPCM Contracts: Which One Can Drive Stronger Outcomes For Project Owners?Đặng Trung AnhNo ratings yet

- RISK IN FidicDocument53 pagesRISK IN FidicANASNo ratings yet

- A Practical Guide To Compensation EventsDocument2 pagesA Practical Guide To Compensation EventssharfutajNo ratings yet

- AACE Journal On Concurrent DelayDocument10 pagesAACE Journal On Concurrent DelayManoj LankaNo ratings yet

- FIDIC's New Standard Forms of Construction Contract - An Introduction - C.R. SeppalaDocument7 pagesFIDIC's New Standard Forms of Construction Contract - An Introduction - C.R. SeppalaHubert BonamisNo ratings yet

- Contracts and Contract Law: Prepared and Presented BY: Prof. Khem DallakotiDocument11 pagesContracts and Contract Law: Prepared and Presented BY: Prof. Khem DallakotiSujan SinghNo ratings yet

- MPL Article Managing An NEC3 ProgrammeDocument9 pagesMPL Article Managing An NEC3 Programmecv21joNo ratings yet

- Management PhrasesDocument1 pageManagement PhrasesEslam AshourNo ratings yet

- 1 by 50Document3 pages1 by 50Eslam AshourNo ratings yet

- Concurrently DelayedDocument6 pagesConcurrently DelayedEslam AshourNo ratings yet

- British Steel V Cleveland Bridge (1981) 24 BLR 94, Robert Goff J.Document1 pageBritish Steel V Cleveland Bridge (1981) 24 BLR 94, Robert Goff J.Eslam AshourNo ratings yet

- Article 19Document18 pagesArticle 19Eslam AshourNo ratings yet

- Tunnelling Journal 6-2017 - Dispute Adjudication BoardsDocument4 pagesTunnelling Journal 6-2017 - Dispute Adjudication BoardsEslam AshourNo ratings yet

- Delay Analysis 1Document8 pagesDelay Analysis 1Eslam AshourNo ratings yet

- Agreement Sub-ConsultancyDocument4 pagesAgreement Sub-ConsultancyEslam AshourNo ratings yet

- Inspection Report Materials Delivered Project SiteDocument1 pageInspection Report Materials Delivered Project SiteEslam AshourNo ratings yet

- HOWES - Alan - Patrick CV PDFDocument6 pagesHOWES - Alan - Patrick CV PDFEslam AshourNo ratings yet

- Field Sketch IssueDocument1 pageField Sketch IssueEslam AshourNo ratings yet

- Income Taxes: Foreign Operating Companies - Branch OfficesDocument2 pagesIncome Taxes: Foreign Operating Companies - Branch OfficesEslam AshourNo ratings yet

- Estimated ScheduleDocument6 pagesEstimated ScheduleEslam AshourNo ratings yet

- Acknowledgment FormDocument1 pageAcknowledgment FormEslam AshourNo ratings yet

- Question 2: (Your Answers Should Be Taken From FIDIC 99, As May Be Applicable)Document2 pagesQuestion 2: (Your Answers Should Be Taken From FIDIC 99, As May Be Applicable)Eslam AshourNo ratings yet

- LOBST Example PDFDocument3 pagesLOBST Example PDFEslam AshourNo ratings yet

- Management PhrasesDocument1 pageManagement PhrasesEslam AshourNo ratings yet

- MENASOL 2010 Hela CheikhrouhouDocument20 pagesMENASOL 2010 Hela CheikhrouhouEslam AshourNo ratings yet

- Solution of Case 14 PDFDocument8 pagesSolution of Case 14 PDFEslam AshourNo ratings yet

- BechtelDocument10 pagesBechtelEslam AshourNo ratings yet

- AmCham Egypt - Online Services - Tenders Alert Service (TAS) 1111Document2 pagesAmCham Egypt - Online Services - Tenders Alert Service (TAS) 1111Eslam AshourNo ratings yet

- Management PhrasesDocument1 pageManagement PhrasesEslam AshourNo ratings yet

- Sample Letter of RecommendationDocument1 pageSample Letter of RecommendationEslam AshourNo ratings yet

- Script - TEST 5 (1st Mid-Term)Document2 pagesScript - TEST 5 (1st Mid-Term)Thu PhạmNo ratings yet

- B767 WikipediaDocument18 pagesB767 WikipediaxXxJaspiexXx100% (1)

- Grammar Level 1 2013-2014 Part 2Document54 pagesGrammar Level 1 2013-2014 Part 2Temur SaidkhodjaevNo ratings yet

- Module 1 in Contemporary Arts First MonthDocument12 pagesModule 1 in Contemporary Arts First MonthMiles Bugtong CagalpinNo ratings yet

- 6 Lesson Writing Unit: Personal Recount For Grade 3 SEI, WIDA Level 2 Writing Kelsie Drown Boston CollegeDocument17 pages6 Lesson Writing Unit: Personal Recount For Grade 3 SEI, WIDA Level 2 Writing Kelsie Drown Boston Collegeapi-498419042No ratings yet

- Chippernac: Vacuum Snout Attachment (Part Number 1901113)Document2 pagesChippernac: Vacuum Snout Attachment (Part Number 1901113)GeorgeNo ratings yet

- Selloooh X Shopee HandbookDocument47 pagesSelloooh X Shopee Handbooknora azaNo ratings yet

- Georgetown University NewsletterDocument3 pagesGeorgetown University Newsletterapi-262723514No ratings yet

- Portfolio HistoryDocument8 pagesPortfolio Historyshubham singhNo ratings yet

- Introduction To ResearchDocument5 pagesIntroduction To Researchapi-385504653No ratings yet

- Bach Invention No9 in F Minor - pdf845725625Document2 pagesBach Invention No9 in F Minor - pdf845725625ArocatrumpetNo ratings yet

- Midterm Exam ADM3350 Summer 2022 PDFDocument7 pagesMidterm Exam ADM3350 Summer 2022 PDFHan ZhongNo ratings yet

- Building Materials Alia Bint Khalid 19091AA001: Q) What Are The Constituents of Paint? What AreDocument22 pagesBuilding Materials Alia Bint Khalid 19091AA001: Q) What Are The Constituents of Paint? What Arealiyah khalidNo ratings yet

- Understanding Malaysian Property TaxationDocument68 pagesUnderstanding Malaysian Property TaxationLee Chee KheongNo ratings yet

- Calvo, G (1988) - Servicing The Public Debt - The Role of ExpectationsDocument16 pagesCalvo, G (1988) - Servicing The Public Debt - The Role of ExpectationsDaniela SanabriaNo ratings yet

- LIN 1. General: Body Electrical - Multiplex Communication BE-13Document2 pagesLIN 1. General: Body Electrical - Multiplex Communication BE-13Roma KuzmychNo ratings yet

- Evirtualguru Computerscience 43 PDFDocument8 pagesEvirtualguru Computerscience 43 PDFJAGANNATH THAWAITNo ratings yet

- Diagram Illustrating The Globalization Concept and ProcessDocument1 pageDiagram Illustrating The Globalization Concept and ProcessAnonymous hWHYwX6No ratings yet

- I CEV20052 Structureofthe Food Service IndustryDocument98 pagesI CEV20052 Structureofthe Food Service IndustryJowee TigasNo ratings yet

- AGIL KENYA For Web - tcm141-76354Document4 pagesAGIL KENYA For Web - tcm141-76354Leah KimuhuNo ratings yet

- PNP TELEPHONE DIRECTORY As of JUNE 2022Document184 pagesPNP TELEPHONE DIRECTORY As of JUNE 2022lalainecd0616No ratings yet

- ITN v7 Release NotesDocument4 pagesITN v7 Release NotesMiguel Angel Ruiz JaimesNo ratings yet

- Q3 Week 7 Day 2Document23 pagesQ3 Week 7 Day 2Ran MarNo ratings yet

- Expectations for Students and ParentsDocument15 pagesExpectations for Students and ParentsJasmine TaourtiNo ratings yet

- Krittika Takiar PDFDocument2 pagesKrittika Takiar PDFSudhakar TomarNo ratings yet

- MAT 1100 Mathematical Literacy For College StudentsDocument4 pagesMAT 1100 Mathematical Literacy For College StudentsCornerstoneFYENo ratings yet