You might also like

- Eviews Class ProblemsDocument3 pagesEviews Class ProblemsLakshmiNo ratings yet

- SSRN Id262067Document71 pagesSSRN Id262067Juliano VieiraNo ratings yet

- Simulated Annealing For Complex Portfolio Selection ProblemsDocument26 pagesSimulated Annealing For Complex Portfolio Selection Problemsveeken77No ratings yet

- Markowitz Portfolio Optimisation Process With Single Index ModelDocument13 pagesMarkowitz Portfolio Optimisation Process With Single Index ModelVinod KumarNo ratings yet

- SSRN Id3760593Document68 pagesSSRN Id3760593YI LINo ratings yet

- A Risk-Transaction Cost Trade-Off Model For Index Tracking: Alex SinghDocument40 pagesA Risk-Transaction Cost Trade-Off Model For Index Tracking: Alex SinghTalin MachinNo ratings yet

- Final Report SI Model - Group 1 - Sec ADocument13 pagesFinal Report SI Model - Group 1 - Sec AVinod KumarNo ratings yet

- Powerful Forecasting With MS Excel SampleDocument257 pagesPowerful Forecasting With MS Excel SamplelpachasmNo ratings yet

- Emperical Evidence in CAPMDocument2 pagesEmperical Evidence in CAPMgauravjindal1No ratings yet

- The Mathematics of DiversificationDocument8 pagesThe Mathematics of DiversificationRyanNo ratings yet

- Index Models ExplainedDocument46 pagesIndex Models ExplainedHanis RashidahNo ratings yet

- Statistical Arbitrage For Mid-Frequency TradingDocument17 pagesStatistical Arbitrage For Mid-Frequency Tradingc0ldlimit8345No ratings yet

- ISYE Midterm Project: Allan Zhang June 2019Document6 pagesISYE Midterm Project: Allan Zhang June 2019Allan ZhangNo ratings yet

- PR Emet 2 PDFDocument2 pagesPR Emet 2 PDFgleniaNo ratings yet

- On The Stability of The CAPM Before and After The Financial Crisis: Panel Evidence From The Johannesburg Securities ExchangeDocument10 pagesOn The Stability of The CAPM Before and After The Financial Crisis: Panel Evidence From The Johannesburg Securities ExchangeGian Carlo Malapajo ArceNo ratings yet

- SSRN Id3586040 PDFDocument25 pagesSSRN Id3586040 PDFAkil LawyerNo ratings yet

- Powerful Forecasting With MS Excel SampleDocument257 pagesPowerful Forecasting With MS Excel SampleBiwesh NeupaneNo ratings yet

- Summary of The Asset Pricing PapersDocument41 pagesSummary of The Asset Pricing PapersClaas RenkemaNo ratings yet

- RapportDocument39 pagesRapportMichael PetersNo ratings yet

- Portfolio ConstructionDocument27 pagesPortfolio ConstructionmarkosovsNo ratings yet

- Single Index ModelDocument14 pagesSingle Index ModelBikram MaharjanNo ratings yet

- The Relative Efficiency of Beta EstimatesDocument20 pagesThe Relative Efficiency of Beta EstimatesWill SongNo ratings yet

- Dynamic Surplus OptimizationDocument31 pagesDynamic Surplus OptimizationdeepNo ratings yet

- MP1 ReportDocument9 pagesMP1 ReportRachit BhagatNo ratings yet

- Asset PricingDocument23 pagesAsset PricingBrian DhliwayoNo ratings yet

- CH 22Document17 pagesCH 22Junaid JamshaidNo ratings yet

- Table of Contents................................................................................... 1 I.A New Approach To Real Estate Risk by Dibartolomeo, Et - Al.................... 2Document33 pagesTable of Contents................................................................................... 1 I.A New Approach To Real Estate Risk by Dibartolomeo, Et - Al.................... 2Nancy Dela TorreNo ratings yet

- Chapter 3: The Arbitrage Pricing TheoryDocument8 pagesChapter 3: The Arbitrage Pricing TheoryAshikNo ratings yet

- SIMP-40Document26 pagesSIMP-40Ishtiaq Hasnat Chowdhury RatulNo ratings yet

- Black Litter ManDocument34 pagesBlack Litter ManmaoychrisNo ratings yet

- Resume CH 7 - 0098 - 0326Document5 pagesResume CH 7 - 0098 - 0326nur eka ayu danaNo ratings yet

- Long-Term Market Equilibrium Modeling For Generation Expansion PlanningDocument7 pagesLong-Term Market Equilibrium Modeling For Generation Expansion PlanningItalo ChiarellaNo ratings yet

- Risk, Returns and WACC: CAPM and The Capital BudgetingDocument41 pagesRisk, Returns and WACC: CAPM and The Capital Budgetingpeter sumNo ratings yet

- Powerful Forecasting With MS Excel Sample PDFDocument257 pagesPowerful Forecasting With MS Excel Sample PDFn_gireesh5468No ratings yet

- LLR PengWangDocument22 pagesLLR PengWangJacky PoNo ratings yet

- Powerful Forecasting With MS Excel SampleDocument257 pagesPowerful Forecasting With MS Excel SampleHarsa WaraNo ratings yet

- Applying Deep Learning To Enhance Momentum Trading Strategies in StocksDocument5 pagesApplying Deep Learning To Enhance Momentum Trading Strategies in StocksMarkNo ratings yet

- Portfolio Optimization: Proceedings of The 2nd Fields-MITACS Industrial Problem-Solving Workshop, 2008Document13 pagesPortfolio Optimization: Proceedings of The 2nd Fields-MITACS Industrial Problem-Solving Workshop, 2008Srijan SehgalNo ratings yet

- Table of Content: Executive Summary Part I: Introduction I. Background and MotivationDocument14 pagesTable of Content: Executive Summary Part I: Introduction I. Background and MotivationTungPhamNo ratings yet

- CH 6 Single IndexDocument20 pagesCH 6 Single IndexAkshay GatkalNo ratings yet

- FCF Valuation ModelDocument8 pagesFCF Valuation ModelDemi Tugano BernardinoNo ratings yet

- Forecasting Swiss Inflation With A Structural Macromodel: The Role of Technical Progress and The "Mortgage Rate-Housing Rent" LinkDocument40 pagesForecasting Swiss Inflation With A Structural Macromodel: The Role of Technical Progress and The "Mortgage Rate-Housing Rent" LinkerererehgjdsassdfNo ratings yet

- Salomon Smith Barney Principles of Principal Components A Fresh Look at Risk Hedging and Relative ValueDocument45 pagesSalomon Smith Barney Principles of Principal Components A Fresh Look at Risk Hedging and Relative ValueRodrigoNo ratings yet

- Single Index Model & The Capital Asset Pricing ModelDocument75 pagesSingle Index Model & The Capital Asset Pricing ModelPrathiba PereraNo ratings yet

- ForecastingDocument5 pagesForecastingDaphne Joyce NocilladoNo ratings yet

- Measuring, Adjusting, and Forecasting Beta: The Case of All The Lebanese Listed FirmsDocument12 pagesMeasuring, Adjusting, and Forecasting Beta: The Case of All The Lebanese Listed Firmsjiten_duaNo ratings yet

- Stock Market Analysis Using Multidimensional Scaling: Ravee MallaDocument5 pagesStock Market Analysis Using Multidimensional Scaling: Ravee MallarajritesNo ratings yet

- FINALS Investment Cheat SheetDocument9 pagesFINALS Investment Cheat SheetNicholas YinNo ratings yet

- Finance and Economics Discussion Series Divisions of Research & Statistics and Monetary Affairs Federal Reserve Board, Washington, D.CDocument33 pagesFinance and Economics Discussion Series Divisions of Research & Statistics and Monetary Affairs Federal Reserve Board, Washington, D.CPradeep Srivatsava ManikondaNo ratings yet

- Evaluating The Performance of Nearest Neighbour Algorithms When Forecasting US Industry ReturnsDocument20 pagesEvaluating The Performance of Nearest Neighbour Algorithms When Forecasting US Industry ReturnsOotam SeewoogoolamNo ratings yet

- How to Value Stocks Using Capital Asset Pricing Theory and the CAPM ModelDocument41 pagesHow to Value Stocks Using Capital Asset Pricing Theory and the CAPM ModelAdam KhaleelNo ratings yet

- Can Market Regimes Really Be Timed With Historical Volatility?Document21 pagesCan Market Regimes Really Be Timed With Historical Volatility?hackmaverickNo ratings yet

- Ecf350 FPD 9 2021 1Document27 pagesEcf350 FPD 9 2021 1elishankampila3500No ratings yet

- Arbitrage Pricing Theory ExplainedDocument8 pagesArbitrage Pricing Theory Explainedsush_bhatNo ratings yet

- Cost 1Document23 pagesCost 1vatsadbgNo ratings yet

- Integer Optimization and its Computation in Emergency ManagementFrom EverandInteger Optimization and its Computation in Emergency ManagementNo ratings yet

- TT19BTCDocument9 pagesTT19BTCamericus_smile7474No ratings yet

- Economics AffairsDocument14 pagesEconomics AffairsAjdin ImsirovicNo ratings yet

- Econ252 15 032111 MCDocument3 pagesEcon252 15 032111 MCAaron CollinsNo ratings yet

- Chuong3 Swaps 2013 SDocument50 pagesChuong3 Swaps 2013 Samericus_smile7474No ratings yet

- Sentence TransformationDocument9 pagesSentence Transformationamericus_smile7474No ratings yet

- Chuong 2 Forward and Futures 2013 SDocument120 pagesChuong 2 Forward and Futures 2013 Samericus_smile7474100% (1)

- 983 BC Ket Qua Thuc Hien Co Che Tu Chu Ve Tai Chinh0001Document3 pages983 BC Ket Qua Thuc Hien Co Che Tu Chu Ve Tai Chinh0001americus_smile7474No ratings yet

- Ac Guide Dec11 CH 11Document4 pagesAc Guide Dec11 CH 11americus_smile7474No ratings yet

- ActerDocument5 pagesActeramericus_smile7474No ratings yet

- Bai NhomDocument5 pagesBai Nhomamericus_smile7474No ratings yet

- Econ 252 Spring 2011 Problem Set 5 SolutionDocument7 pagesEcon 252 Spring 2011 Problem Set 5 Solutionamericus_smile7474No ratings yet

- Econ 252 Spring 2011 Problem Set 5Document5 pagesEcon 252 Spring 2011 Problem Set 5americus_smile7474No ratings yet

- Bai Tap 16Document6 pagesBai Tap 16americus_smile7474No ratings yet

- Chuong 1 Introduction 2013 SDocument82 pagesChuong 1 Introduction 2013 Samericus_smile7474No ratings yet

- Lecture Notes (Financial Economics)Document136 pagesLecture Notes (Financial Economics)americus_smile7474100% (2)

- 5021 Solutions 6Document5 pages5021 Solutions 6americus_smile7474100% (1)

- Derivatives Test BankDocument36 pagesDerivatives Test BankNoni Alhussain100% (2)

- Review ExercisesDocument11 pagesReview Exercisesamericus_smile7474No ratings yet

- Review ExercisesDocument11 pagesReview Exercisesamericus_smile7474No ratings yet

- DerivativesDocument10 pagesDerivativesamericus_smile7474No ratings yet

- Assignment1 SolutionsDocument10 pagesAssignment1 Solutionsamericus_smile7474No ratings yet

- 11 Understanding Samsungs Diversification Strategy The Case of Samsung Motors IncDocument17 pages11 Understanding Samsungs Diversification Strategy The Case of Samsung Motors IncSunita NairNo ratings yet

- William Sharpe Simplified Model of Portfolio Analysis 0Document18 pagesWilliam Sharpe Simplified Model of Portfolio Analysis 0americus_smile7474No ratings yet

- CH 5 QaDocument2 pagesCH 5 Qaamericus_smile7474100% (1)

- Margaret Thatcher A PortraitDocument235 pagesMargaret Thatcher A Portraitamericus_smile7474No ratings yet

- Analysis of Variance (ANOVA)Document9 pagesAnalysis of Variance (ANOVA)americus_smile7474No ratings yet

- UTP App CTA ExplanationDocument7 pagesUTP App CTA ExplanationDuyen HuynhNo ratings yet

- Lagrangian Methods For Constrained OptimizationDocument6 pagesLagrangian Methods For Constrained Optimizationcesar_luis_galliNo ratings yet

- Portflolio Optimisation 2Document28 pagesPortflolio Optimisation 2americus_smile7474No ratings yet

- Core Lbo ModelDocument25 pagesCore Lbo Modelsalman_schonNo ratings yet

- The Cost of Capital ExplainedDocument56 pagesThe Cost of Capital ExplainedAndayani SalisNo ratings yet

- Standard Setting As Politics (CH13) Scott PDFDocument19 pagesStandard Setting As Politics (CH13) Scott PDFDwie HernawanNo ratings yet

- DPT-3 filing deadline: What is not considered a depositDocument2 pagesDPT-3 filing deadline: What is not considered a depositNiyati KamaniNo ratings yet

- 2.0 Practical Lessons On Dos and Donts For Internal Auditors A Case Study of A Listed Company CPA Denish OsodoDocument15 pages2.0 Practical Lessons On Dos and Donts For Internal Auditors A Case Study of A Listed Company CPA Denish Osododaniel geevargheseNo ratings yet

- Investor Agreement ContractDocument4 pagesInvestor Agreement ContractGian Joaquin0% (1)

- A Study On Accounting Policies Followed byDocument23 pagesA Study On Accounting Policies Followed byhbkrakesh83% (12)

- Capital Raising Book by Richard C WilsonDocument101 pagesCapital Raising Book by Richard C WilsonNickMyersNo ratings yet

- Reading List First Semester 2017-2018Document15 pagesReading List First Semester 2017-2018NajjaSheriff007No ratings yet

- Ch2 The Conceptual Framework Project TesDocument15 pagesCh2 The Conceptual Framework Project TesAbdalelah FrarjehNo ratings yet

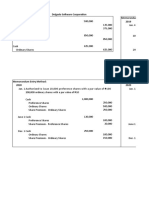

- Memorandum and Journal Entry Methods for Share Capital TransactionsDocument3 pagesMemorandum and Journal Entry Methods for Share Capital TransactionsFeiya Liu100% (1)

- PT Delta Djakarta TBK Dan Entitas Anak/: and Its SubsidiaryDocument77 pagesPT Delta Djakarta TBK Dan Entitas Anak/: and Its SubsidiaryAlensyahNo ratings yet

- Lesson 5 Agency Problems and Accountability of Corporate Managers and 2Document39 pagesLesson 5 Agency Problems and Accountability of Corporate Managers and 2Dianne Pearl DelfinNo ratings yet

- Group Financial Accounting PresentationDocument84 pagesGroup Financial Accounting PresentationAndoline SibandaNo ratings yet

- UT Dallas Syllabus For Fin7310.001 05f Taught by Nina Baranchuk (nxb043000)Document5 pagesUT Dallas Syllabus For Fin7310.001 05f Taught by Nina Baranchuk (nxb043000)UT Dallas Provost's Technology GroupNo ratings yet

- Startup India PDFDocument16 pagesStartup India PDFAkshayNo ratings yet

- Financial Statements-Schedule-III - Companies Act, 2013 PDFDocument13 pagesFinancial Statements-Schedule-III - Companies Act, 2013 PDFCA Ujjwal KumarNo ratings yet

- Shashi FinalDocument86 pagesShashi FinalVidyaNo ratings yet

- 6-2 Affidavit of Mailing Notice - Shareholders Annual MeetingDocument1 page6-2 Affidavit of Mailing Notice - Shareholders Annual MeetingDanielNo ratings yet

- FDI and Its Impact in Indian EconomyDocument13 pagesFDI and Its Impact in Indian EconomyMd Haamid NadeemNo ratings yet

- Meezan Bank: Islamic Banking Services and Account TypesDocument41 pagesMeezan Bank: Islamic Banking Services and Account TypesBilal AhmedNo ratings yet

- Luzon Brokerage Co. v. Maritime Building Co. (1972)Document1 pageLuzon Brokerage Co. v. Maritime Building Co. (1972)Onnie Lee100% (1)

- Nubank: A Brazilian FinTech Worth $10 Billion - MEDICIDocument25 pagesNubank: A Brazilian FinTech Worth $10 Billion - MEDICIKay BarnesNo ratings yet

- CJS INDEMNITY BOND SECTION 1 Draft Freedom DocumentsDocument44 pagesCJS INDEMNITY BOND SECTION 1 Draft Freedom DocumentsAnonymous 23VuLx95% (21)

- Assignment Risk and ReturnDocument3 pagesAssignment Risk and ReturnCheong Yu ShuangNo ratings yet

- CMM Short Dated Calc v2 PDFDocument5 pagesCMM Short Dated Calc v2 PDFtallindianNo ratings yet

- Final Exam: Derivatives and Risk ManagementDocument29 pagesFinal Exam: Derivatives and Risk ManagementTrang Nguyễn Hoàng LêNo ratings yet

- Chapter 7 Importance of Money and Capital MarketsDocument9 pagesChapter 7 Importance of Money and Capital MarketsSyrill CayetanoNo ratings yet

- Trading With RDocument19 pagesTrading With Rcodereverser100% (1)

- Deeds Under HK LawDocument2 pagesDeeds Under HK LawAdina MadchenNo ratings yet