You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Life Mapping Workbook 2013Document14 pagesLife Mapping Workbook 2013Regent Brown93% (15)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Sec Trans Outline MEE/UBEDocument8 pagesSec Trans Outline MEE/UBEArthur Shalagin100% (2)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Affordable Housing Recommendations To The Mayor ReportDocument30 pagesAffordable Housing Recommendations To The Mayor ReportMinnesota Public RadioNo ratings yet

- 300 Million Engines of Growth: A Middle-Out Plan For Jobs, Business, and A Growing EconomyDocument252 pages300 Million Engines of Growth: A Middle-Out Plan For Jobs, Business, and A Growing EconomyCenter for American ProgressNo ratings yet

- Xex10 - Working Capital Management With SolutionDocument10 pagesXex10 - Working Capital Management With SolutionJoseph Salido100% (1)

- A Simple FTP Model For A Commercial BankDocument80 pagesA Simple FTP Model For A Commercial BankMaratAyaibergenovNo ratings yet

- Uber Elevate White PaperDocument98 pagesUber Elevate White PaperRoger AllanNo ratings yet

- Commercial CasesDocument28 pagesCommercial CasesJepoy Nisperos ReyesNo ratings yet

- NCBP (NGO) ProfileDocument34 pagesNCBP (NGO) ProfileNCBP100% (1)

- Lagos State Investor Handbook FinalsDocument35 pagesLagos State Investor Handbook Finalsdavid patrick50% (2)

- Jaminan Kewangan BiDocument4 pagesJaminan Kewangan BiWilson Lim100% (1)

- Disability Services Directory June 2014Document7 pagesDisability Services Directory June 2014Roger AllanNo ratings yet

- Trilogy Monthly Income Trust PDS 22 July 2015 WEBDocument56 pagesTrilogy Monthly Income Trust PDS 22 July 2015 WEBRoger AllanNo ratings yet

- WHO - Urban Health - Major Opportunities For Improving Global Health Outcomes, Despite Persistent Health InequitiesDocument4 pagesWHO - Urban Health - Major Opportunities For Improving Global Health Outcomes, Despite Persistent Health InequitiesRoger AllanNo ratings yet

- CL-King Conference Investor-Deck Final 9-9-16Document35 pagesCL-King Conference Investor-Deck Final 9-9-16Roger AllanNo ratings yet

- Jump-Starting Malaysia's Growth - An Interview With Idris JalaDocument7 pagesJump-Starting Malaysia's Growth - An Interview With Idris JalaRoger AllanNo ratings yet

- Hedge Funds Oversight Final ReportDocument26 pagesHedge Funds Oversight Final ReportfafoouNo ratings yet

- Create Your Own Currency!Document7 pagesCreate Your Own Currency!Thomas HoyNo ratings yet

- GratuityDocument6 pagesGratuityLibraryNo ratings yet

- SBI Overview: History, Leadership, OperationsDocument59 pagesSBI Overview: History, Leadership, Operationspuneetbansal14No ratings yet

- G Mango Accounting Pack System v7 2Document13 pagesG Mango Accounting Pack System v7 2GeneVive MendozaNo ratings yet

- Williams v. United States Fidelity & Guaranty Co., 236 U.S. 549 (1915)Document5 pagesWilliams v. United States Fidelity & Guaranty Co., 236 U.S. 549 (1915)Scribd Government DocsNo ratings yet

- Audit procedures for purchase transaction assertionsDocument7 pagesAudit procedures for purchase transaction assertionsnajaneNo ratings yet

- FInalDocument7 pagesFInalRyan Martinez0% (1)

- Indian BankDocument9 pagesIndian BankPraneelaNo ratings yet

- Bank Management Koch 8th Edition Test BankDocument10 pagesBank Management Koch 8th Edition Test Bankmeghantaylorxzfyijkotm100% (45)

- Public Notice REOI CMCDocument2 pagesPublic Notice REOI CMCCliantha AimeeNo ratings yet

- Sales Full Cases (Part I)Document173 pagesSales Full Cases (Part I)Niki Dela CruzNo ratings yet

- CH4+CH5 .FinincingDocument9 pagesCH4+CH5 .Finincingdareen alhadeed100% (1)

- Housing FinanceDocument10 pagesHousing FinancelakshmiNo ratings yet

- Amaefule 12 PH DDocument343 pagesAmaefule 12 PH DIrene A'sNo ratings yet

- Ohnb18 14052 CreditorsDocument2 pagesOhnb18 14052 CreditorsAnonymous YU6gbBcvu3No ratings yet

- Application-Automatic Encashment Plan FacilityDocument9 pagesApplication-Automatic Encashment Plan FacilityVishal KackarNo ratings yet

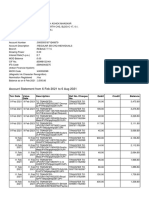

- Mr. SANTOSH ASHOK MHASKAR's account statementDocument14 pagesMr. SANTOSH ASHOK MHASKAR's account statementSantosh MhaskarNo ratings yet

- Improving settlement efficiency and mitigating risks in Hong Kong payment systemsDocument16 pagesImproving settlement efficiency and mitigating risks in Hong Kong payment systemsSathiya RameshNo ratings yet

- Micro Credit in CanadaDocument16 pagesMicro Credit in CanadatextbooksneedthemNo ratings yet

- VIT University Katpadi - Thiruvalam Road Vellore-632014Document1 pageVIT University Katpadi - Thiruvalam Road Vellore-632014AravindanNo ratings yet