You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Bbo Complaint Against Mark Lee - 11-3-22 FinalDocument288 pagesBbo Complaint Against Mark Lee - 11-3-22 FinalJohn WallerNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Trial of Warrant CasesDocument23 pagesTrial of Warrant CasesirampeerzadaNo ratings yet

- Class 11 Political Science - EqualityDocument30 pagesClass 11 Political Science - EqualityRamita Udayashankar100% (2)

- Powerpoint MCQ Bank PDFDocument21 pagesPowerpoint MCQ Bank PDFquickincometips0% (1)

- Powerpoint MCQ Bank PDFDocument21 pagesPowerpoint MCQ Bank PDFquickincometips0% (1)

- Punish The Crime - UNESCO Report On Journalists' SafetyDocument18 pagesPunish The Crime - UNESCO Report On Journalists' SafetyRafister2k13No ratings yet

- Internship Report - CRM (Credit Risk Management) Practice of BASIC Bank Limited, BangladeshDocument67 pagesInternship Report - CRM (Credit Risk Management) Practice of BASIC Bank Limited, BangladeshJamal Hossain Shuvo100% (2)

- Dissecting Anti-Terror Bill in The Philippines: A Swot AnalysisDocument15 pagesDissecting Anti-Terror Bill in The Philippines: A Swot AnalysisAdie LadnamudNo ratings yet

- Private individuals liable under RA 3019 for conspiring with public officersDocument3 pagesPrivate individuals liable under RA 3019 for conspiring with public officersMax RamosNo ratings yet

- Operating Systems MCQ BankDocument21 pagesOperating Systems MCQ BankJamal Hossain Shuvo100% (1)

- JSC composition suggestionsDocument3 pagesJSC composition suggestionsJamal Hossain ShuvoNo ratings yet

- Main Body Part - CRGDocument24 pagesMain Body Part - CRGJamal Hossain ShuvoNo ratings yet

- Bear Call Spread Strategy ExplainedDocument2 pagesBear Call Spread Strategy ExplainedJamal Hossain ShuvoNo ratings yet

- Comparative Short NotesDocument1 pageComparative Short NotesJamal Hossain ShuvoNo ratings yet

- CRM Slide Jamal50duDocument18 pagesCRM Slide Jamal50duJamal Hossain ShuvoNo ratings yet

- Essay Mid-Semester Exam - 6 August 2013Document2 pagesEssay Mid-Semester Exam - 6 August 2013Jamal Hossain ShuvoNo ratings yet

- Bbbaa VivaDocument4 pagesBbbaa VivaJamal Hossain ShuvoNo ratings yet

- Ent MGT Assignment 1 Detailed GuidelineDocument2 pagesEnt MGT Assignment 1 Detailed GuidelineJamal Hossain ShuvoNo ratings yet

- Interpersonal CommunicationDocument2 pagesInterpersonal CommunicationJamal Hossain ShuvoNo ratings yet

- Arif's CVDocument3 pagesArif's CVJamal Hossain ShuvoNo ratings yet

- Management Foundations Assessment 2 Business Report 2013Document7 pagesManagement Foundations Assessment 2 Business Report 2013Jamal Hossain ShuvoNo ratings yet

- Statistics Term Paper FINALDocument60 pagesStatistics Term Paper FINALJamal Hossain ShuvoNo ratings yet

- 1 Managing-ProjectsDocument9 pages1 Managing-ProjectsJamal Hossain ShuvoNo ratings yet

- Ethics Case Study ADocument2 pagesEthics Case Study AJamal Hossain ShuvoNo ratings yet

- HRMDocument5 pagesHRMJamal Hossain ShuvoNo ratings yet

- Shantii Marketing AssignmentDocument4 pagesShantii Marketing AssignmentJamal Hossain ShuvoNo ratings yet

- Assessment 2 International Marketing StrategyDocument4 pagesAssessment 2 International Marketing StrategyJamal Hossain ShuvoNo ratings yet

- Investment BankingDocument3 pagesInvestment BankingJamal Hossain ShuvoNo ratings yet

- AuditDocument3 pagesAuditJamal Hossain ShuvoNo ratings yet

- Assessment 1 International Marketing StrategyDocument2 pagesAssessment 1 International Marketing StrategyJamal Hossain ShuvoNo ratings yet

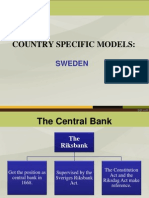

- SWEDEN'S CENTRAL BANK AND PARLIAMENTARY OVERSIGHTDocument8 pagesSWEDEN'S CENTRAL BANK AND PARLIAMENTARY OVERSIGHTJamal Hossain ShuvoNo ratings yet

- Audit FinalDocument4 pagesAudit FinalJamal Hossain ShuvoNo ratings yet

- AuditDocument3 pagesAuditJamal Hossain ShuvoNo ratings yet

- Step10 PlagiarismDocument15 pagesStep10 PlagiarismJamal Hossain Shuvo100% (1)

- Islamic BankingDocument1 pageIslamic BankingJamal Hossain ShuvoNo ratings yet

- CV of Jamal HossainDocument2 pagesCV of Jamal HossainJamal Hossain ShuvoNo ratings yet

- Nikole Read Appointed Chairperson of International Trade Council in CanadaDocument2 pagesNikole Read Appointed Chairperson of International Trade Council in CanadaMary Joy Dela MasaNo ratings yet

- FS - Courtesy Copy of The Partial AwardDocument549 pagesFS - Courtesy Copy of The Partial AwardNatalia CheleNo ratings yet

- Land Bank of The Philippines Vs Eugenio Dalauta DigestDocument2 pagesLand Bank of The Philippines Vs Eugenio Dalauta DigestLawrence Y. CapuchinoNo ratings yet

- Judicial Activism OR PILDocument26 pagesJudicial Activism OR PILShaman KingNo ratings yet

- MC 2016 Hypothetical Case PDFDocument8 pagesMC 2016 Hypothetical Case PDFMulugeta BarisoNo ratings yet

- IJCIET (International Journal of Civil Engineering and Technology)Document1 pageIJCIET (International Journal of Civil Engineering and Technology)Andi Nurul Annisaa FirdausiNo ratings yet

- Barangay Budget Self Evaluation No. 2018-000 TemplateDocument3 pagesBarangay Budget Self Evaluation No. 2018-000 Templatejuliet comia canino100% (1)

- Social Movement CoalitionsDocument17 pagesSocial Movement CoalitionsgmNo ratings yet

- Summary Sheet NFPA 1710 StandardDocument2 pagesSummary Sheet NFPA 1710 StandardNicoNo ratings yet

- Philippine Courts, Justices and Judges: Politics and Governance With The New ConstitutionDocument11 pagesPhilippine Courts, Justices and Judges: Politics and Governance With The New ConstitutionDominick DiscargaNo ratings yet

- Top TipsDocument2 pagesTop TipsPeter GriffinNo ratings yet

- Raghav Sehgal - 1 Mar. 2021Document3 pagesRaghav Sehgal - 1 Mar. 2021Raghav SehgalNo ratings yet

- Digital Roadmap For Ruslan VodkaDocument14 pagesDigital Roadmap For Ruslan VodkaShrinesh PoudelNo ratings yet

- Fazle Rabbi Annoor Id-05 MBA Mid Exam Answer MTM-5201Document3 pagesFazle Rabbi Annoor Id-05 MBA Mid Exam Answer MTM-5201Fazle-Rabbi AnnoorNo ratings yet

- Promotional ToolsDocument36 pagesPromotional ToolsKyla LimNo ratings yet

- Chandru Tro ResearchDocument2 pagesChandru Tro ResearchJoey JawidNo ratings yet

- SFPD Chief Greg Suhr April 4 Letter To DA George Gascón Re: Bigoted TextsDocument2 pagesSFPD Chief Greg Suhr April 4 Letter To DA George Gascón Re: Bigoted TextsKQED NewsNo ratings yet

- SPEC PRO 255. Republic v. Cantor, GR No. 184621, December 10, 2013Document15 pagesSPEC PRO 255. Republic v. Cantor, GR No. 184621, December 10, 2013Claudia LapazNo ratings yet

- Dinesh Kumar Yadav Vs State of UP and Ors 27102016UP2016151216163121274COM512213Document14 pagesDinesh Kumar Yadav Vs State of UP and Ors 27102016UP2016151216163121274COM512213Geetansh AgarwalNo ratings yet

- Court acquits Negros radio anchor of libel chargesDocument6 pagesCourt acquits Negros radio anchor of libel chargesPrincessNo ratings yet

- Gallardo vs. Judge TabamoDocument8 pagesGallardo vs. Judge TabamoAlyssa Alee Angeles JacintoNo ratings yet

- QAI Counter Terrorism Finance and Anti Money Laundering Discussion ReportDocument7 pagesQAI Counter Terrorism Finance and Anti Money Laundering Discussion ReportQatar-America InstituteNo ratings yet

- DOJ Report On BPD PDFDocument164 pagesDOJ Report On BPD PDFMichael LindenbergerNo ratings yet

- Court upholds denial of petition seeking relief from legal mistakesDocument3 pagesCourt upholds denial of petition seeking relief from legal mistakesEFGNo ratings yet