You might also like

- TUI - Analysis and ImplicationsDocument26 pagesTUI - Analysis and ImplicationsSreerag Gangadharan92% (13)

- PEST Analysis of European Tour OperatorsDocument12 pagesPEST Analysis of European Tour OperatorsSarojani NeupaneNo ratings yet

- Alarm List NodeBDocument16 pagesAlarm List NodeBAli GencerNo ratings yet

- Balakrishnan MGRL Solutions Ch07Document50 pagesBalakrishnan MGRL Solutions Ch07deeNo ratings yet

- TTCR Chapter1.5 2013Document7 pagesTTCR Chapter1.5 2013Deepak PandeyNo ratings yet

- The Impact of Exchange Rate On Tourism IDocument15 pagesThe Impact of Exchange Rate On Tourism IMija DiroNo ratings yet

- Incredible India - Final Report RecoveredDocument33 pagesIncredible India - Final Report RecoveredanujkuthialaNo ratings yet

- The Task, Challenges and Strategies For The Marketing of Tourism and Relaxation Services in NigeriaDocument22 pagesThe Task, Challenges and Strategies For The Marketing of Tourism and Relaxation Services in Nigeriaali purityNo ratings yet

- Analysis of Fdi in The Tourism Sector: The Case Study of The Republic of CroatiaDocument12 pagesAnalysis of Fdi in The Tourism Sector: The Case Study of The Republic of Croatia01082008No ratings yet

- UNWTO Tourism Highlights 2010Document3 pagesUNWTO Tourism Highlights 2010Marko ŠpraljaNo ratings yet

- The Global Crisis and Philippine Tourism: Impact and Policy Responses Executive SummaryDocument9 pagesThe Global Crisis and Philippine Tourism: Impact and Policy Responses Executive Summarysatria carterNo ratings yet

- Economic Environment: 1. Macroeconomic TrendsDocument13 pagesEconomic Environment: 1. Macroeconomic TrendsJonathan FernandezNo ratings yet

- Unit 1 Tourism 1 2023Document30 pagesUnit 1 Tourism 1 2023slimdash4bookingsNo ratings yet

- Modelling Multivariate Volatility in International Tourism and Country Risk For Cyprus and MaltaDocument9 pagesModelling Multivariate Volatility in International Tourism and Country Risk For Cyprus and MaltaspratiwiaNo ratings yet

- (Full Paper) Greek Tourism Under Crisi - Strategies and The Way OutDocument24 pages(Full Paper) Greek Tourism Under Crisi - Strategies and The Way OutSotiris VarelasNo ratings yet

- Cambodia Global Econ CrisisDocument64 pagesCambodia Global Econ Crisisru_radaNo ratings yet

- Impact of Covid 19 On Tourism and Hotels of EthiopiaDocument6 pagesImpact of Covid 19 On Tourism and Hotels of EthiopiaFuadNo ratings yet

- Module-3 TrendsDocument8 pagesModule-3 TrendsKristine Rose D. AgustinNo ratings yet

- Turkey Tourism Report by British EmbassyDocument24 pagesTurkey Tourism Report by British Embassypromus1No ratings yet

- Tourism Market and Target SelectionDocument25 pagesTourism Market and Target SelectionHasinaImamNo ratings yet

- The Impacts of International Tourism Demand On Economic Growth of Small Economies Dependent On TourismDocument9 pagesThe Impacts of International Tourism Demand On Economic Growth of Small Economies Dependent On TourismNanda SyafiraNo ratings yet

- Travel and Tourism: Survive, Revive and Thrive in Times of COVID-19Document37 pagesTravel and Tourism: Survive, Revive and Thrive in Times of COVID-19Nazmul IslamNo ratings yet

- Indian Travel, Tourism and Hospitality IndustryDocument16 pagesIndian Travel, Tourism and Hospitality Industrysukriti2812No ratings yet

- Tourism and BrandingDocument20 pagesTourism and BrandingRaluca RaduNo ratings yet

- Travel & Tourism Competitiveness Report 2009Document526 pagesTravel & Tourism Competitiveness Report 2009World Economic Forum100% (2)

- Bereket Tourism EconomicsDocument13 pagesBereket Tourism EconomicsBereket keregaNo ratings yet

- Impacts of TourismDocument7 pagesImpacts of TourismCarson FowlingNo ratings yet

- Measuring Financial Leakage and LinkageDocument16 pagesMeasuring Financial Leakage and LinkageShyam ThapaNo ratings yet

- Turkey 2016Document24 pagesTurkey 2016api-341298343No ratings yet

- Lab AssignmentDocument16 pagesLab Assignmentakansha mehtaNo ratings yet

- Thomas Cook India PVT LTD (Soumit)Document90 pagesThomas Cook India PVT LTD (Soumit)Soumit BiswasNo ratings yet

- The Foregion Curency and The Indian Tourism IndustryDocument8 pagesThe Foregion Curency and The Indian Tourism IndustryAnonymous CwJeBCAXpNo ratings yet

- Impact of Pandemic Covid-19 On The Tourism Sector: Country AnalysisDocument8 pagesImpact of Pandemic Covid-19 On The Tourism Sector: Country AnalysisShopping SpreeNo ratings yet

- Brazil TourismDocument3 pagesBrazil Tourismvikram2328No ratings yet

- Editorial: Covid-19 Pandemic and International Tourism DemandDocument5 pagesEditorial: Covid-19 Pandemic and International Tourism DemandCaterpillar MinithesisNo ratings yet

- Şakir Görmüş - Imet GozerDocument13 pagesŞakir Görmüş - Imet GozerAzizur RohmanNo ratings yet

- Tourism Industry Profile IndiaDocument23 pagesTourism Industry Profile IndiaPrince Satish Reddy50% (2)

- Unit 2 Global Impacts: 2.0 ObjectivesDocument9 pagesUnit 2 Global Impacts: 2.0 ObjectivesAnvesh VakadiNo ratings yet

- Progress and Priorities, 2010-2011Document32 pagesProgress and Priorities, 2010-2011ovidiu.moisescu8209No ratings yet

- Chapter 1 Research Chapter 1Document48 pagesChapter 1 Research Chapter 1Pritz MishraNo ratings yet

- Egypt PEST AnalysisDocument12 pagesEgypt PEST AnalysisMohamed AlyNo ratings yet

- Comparison of UAE and French EconomyDocument16 pagesComparison of UAE and French EconomyuowdubaiNo ratings yet

- E Tourism PaperDocument16 pagesE Tourism Paperjimmy lecturerNo ratings yet

- Medical Tourism FinalDocument110 pagesMedical Tourism FinalsphoorthiiNo ratings yet

- Shivani 6Document28 pagesShivani 6Ravneet KaurNo ratings yet

- Article Financial Crisis KapikiDocument14 pagesArticle Financial Crisis KapikiFlorentin DrăganNo ratings yet

- Global Trends in TourismDocument7 pagesGlobal Trends in Tourismsainidharmveer1_6180No ratings yet

- UNWTO Tourism Highlights 2011 EditionDocument12 pagesUNWTO Tourism Highlights 2011 EditionPablo Alarcón100% (1)

- Portugal 2016Document24 pagesPortugal 2016Rahman FahimNo ratings yet

- Country Strategy 2011-2014 TurkeyDocument16 pagesCountry Strategy 2011-2014 TurkeyBeeHoofNo ratings yet

- An Economic Impact of The Tourism Industry in IndiaDocument5 pagesAn Economic Impact of The Tourism Industry in IndiaApurva WaikarNo ratings yet

- WTTC Sectors Summary GlobalDocument35 pagesWTTC Sectors Summary GlobalDragos SmedescuNo ratings yet

- Girard From Linear To Circular TourisDocument25 pagesGirard From Linear To Circular TourisRamón Rueda LópezNo ratings yet

- The Travel & Tourism Competitiveness Report 2015Document519 pagesThe Travel & Tourism Competitiveness Report 2015pavelbtNo ratings yet

- Post 25 JanDocument8 pagesPost 25 JanMohammad Salah RagabNo ratings yet

- Impact of Tourism On Economic GrowthDocument25 pagesImpact of Tourism On Economic Growthhira khalid kareemNo ratings yet

- Global Risks and Tourism IndusDocument25 pagesGlobal Risks and Tourism IndusCristina AftodeNo ratings yet

- Travel and Tourism Competitiveness Report Part 2/3Document111 pagesTravel and Tourism Competitiveness Report Part 2/3World Economic Forum100% (31)

- Macroeconomics IndicatorDocument11 pagesMacroeconomics IndicatorNandini RajNo ratings yet

- The Economic, Social, Environmental, and Psychological Impacts of Tourism DevelopmentFrom EverandThe Economic, Social, Environmental, and Psychological Impacts of Tourism DevelopmentNo ratings yet

- EIB Investment Report 2023/2024 - Key Findings: Transforming for competitivenessFrom EverandEIB Investment Report 2023/2024 - Key Findings: Transforming for competitivenessNo ratings yet

- Turkish Tourism 2010Document19 pagesTurkish Tourism 2010Ali GencerNo ratings yet

- Turkish Tourism 2010Document19 pagesTurkish Tourism 2010Ali GencerNo ratings yet

- EMF ProjectDocument15 pagesEMF ProjectAli GencerNo ratings yet

- Turkish Tourism 2010Document19 pagesTurkish Tourism 2010Ali GencerNo ratings yet

- Turkish Tourism 2010Document19 pagesTurkish Tourism 2010Ali GencerNo ratings yet

- Turkish Tourism 2010Document19 pagesTurkish Tourism 2010Ali GencerNo ratings yet

- Turkish Tourism 2010Document19 pagesTurkish Tourism 2010Ali GencerNo ratings yet

- Turkish Tourism 2010Document19 pagesTurkish Tourism 2010Ali GencerNo ratings yet

- Turkish Tourism 2010Document19 pagesTurkish Tourism 2010Ali GencerNo ratings yet

- Turkish Tourism 2010Document19 pagesTurkish Tourism 2010Ali GencerNo ratings yet

- 3G PSR CheckpointsDocument13 pages3G PSR CheckpointsAli GencerNo ratings yet

- Turkish Tourism 2010Document19 pagesTurkish Tourism 2010Ali GencerNo ratings yet

- 3G PSR CheckpointsDocument13 pages3G PSR CheckpointsAli GencerNo ratings yet

- GSM Optimization Training GOODDocument222 pagesGSM Optimization Training GOODRudianto AruanNo ratings yet

- Turkish Tourism 2010Document19 pagesTurkish Tourism 2010Ali GencerNo ratings yet

- Redefining Research: 186GB in An LTE Network - Been There, Done That (Part II)Document39 pagesRedefining Research: 186GB in An LTE Network - Been There, Done That (Part II)Ali GencerNo ratings yet

- 2019 Analysis SAC Version 2 SolutionDocument6 pages2019 Analysis SAC Version 2 SolutionLachlan McFarlandNo ratings yet

- Session 4 Urban Heritage and CommunityDocument368 pagesSession 4 Urban Heritage and CommunityQuang Huy NguyễnNo ratings yet

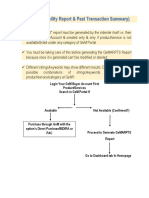

- Gem Availability Report & Past Transaction SummaryDocument9 pagesGem Availability Report & Past Transaction SummarypviveknaiduNo ratings yet

- Lecture 11 - Business and Economics Optimization Problems and Asymptotes PDFDocument9 pagesLecture 11 - Business and Economics Optimization Problems and Asymptotes PDFpupu_putraNo ratings yet

- SAP SD Questionnaire For Scoping and Better Understanding of Business Scenario - SAP BlogsDocument21 pagesSAP SD Questionnaire For Scoping and Better Understanding of Business Scenario - SAP BlogsKhetan BNo ratings yet

- Sale of Goods Act-MCQDocument5 pagesSale of Goods Act-MCQSunita Singhal0% (1)

- Art Fair HistoryDocument20 pagesArt Fair HistoryMo GuanNo ratings yet

- Chapter 01 Brief ThirdDocument28 pagesChapter 01 Brief Thirdjorge AlvaradoNo ratings yet

- Avia2501 StudyguideDocument19 pagesAvia2501 StudyguidePetronas Jeli PSSJELINo ratings yet

- Cost Data 2024 Dated 08022024 - 240209 - 144302Document78 pagesCost Data 2024 Dated 08022024 - 240209 - 144302sreejitvpNo ratings yet

- The 5 Tasks of Entrepreneurial DevelopmentDocument3 pagesThe 5 Tasks of Entrepreneurial DevelopmentJulhayda Fernando100% (1)

- Tata CementDocument70 pagesTata Cementramansuthar100% (2)

- Oferta y DemandaDocument9 pagesOferta y DemandaRosario Rivera NegrónNo ratings yet

- SBP Sample PaperDocument9 pagesSBP Sample PaperTariq Shahzad100% (1)

- Pay Back Contracts For Coordinating Supply ChainDocument29 pagesPay Back Contracts For Coordinating Supply Chainhappiest1No ratings yet

- Exam Success in Economics For Cambridge IGCSE AnswersDocument30 pagesExam Success in Economics For Cambridge IGCSE AnswersAKARESH JOSE EBOOKS100% (1)

- CJC Prelim h2 Econs p2 Answers 2016Document41 pagesCJC Prelim h2 Econs p2 Answers 2016Yan Shen TanNo ratings yet

- En Banc (G.R. No. 31339. November 27, 1929.) THOS. N. POWELL, Plaintiff-Appellee, v. THE PHILIPPINE NATIONAL BANK, DefendantDocument79 pagesEn Banc (G.R. No. 31339. November 27, 1929.) THOS. N. POWELL, Plaintiff-Appellee, v. THE PHILIPPINE NATIONAL BANK, DefendantAnonymous apYVFHnCYNo ratings yet

- Currency Futures NivDocument37 pagesCurrency Futures Nivpratibhashetty_87No ratings yet

- IB&F: 405: Trade Based Modes of Islamic Banking and FinanceDocument34 pagesIB&F: 405: Trade Based Modes of Islamic Banking and FinanceChrissyAlvordNo ratings yet

- (Marx, Engels, and Marxisms) Achim Szepanski - Financial Capital in The 21st Century - A New Theory of Speculative Capital-Palgrave Macmillan (2022)Document388 pages(Marx, Engels, and Marxisms) Achim Szepanski - Financial Capital in The 21st Century - A New Theory of Speculative Capital-Palgrave Macmillan (2022)MarianNo ratings yet

- Principles of Economics 7Th Edition Frank Test Bank Full Chapter PDFDocument67 pagesPrinciples of Economics 7Th Edition Frank Test Bank Full Chapter PDFJenniferWashingtonfbiqe100% (9)

- R5176b PDFDocument53 pagesR5176b PDFAnum ZahraNo ratings yet

- Guide To Pricing Accounting Services (Fixed & Value Pricing)Document28 pagesGuide To Pricing Accounting Services (Fixed & Value Pricing)rexNo ratings yet

- Consolidation Patterns: by Melanie F. Bowman and Thom HartleDocument7 pagesConsolidation Patterns: by Melanie F. Bowman and Thom HartleFetogNo ratings yet

- Answers To Review Quizzes & Problems - CH 05 PDFDocument16 pagesAnswers To Review Quizzes & Problems - CH 05 PDFPrajna MelittaNo ratings yet

- Definition of Failure:: Mubarak Abdessalam Argues ThatDocument14 pagesDefinition of Failure:: Mubarak Abdessalam Argues ThatNabeel AnsariNo ratings yet

- Agricultural PolicyDocument28 pagesAgricultural PolicyMuhammad JufriNo ratings yet