You might also like

- Aerithmatic EvaluationDocument62 pagesAerithmatic EvaluationUmesgNo ratings yet

- Progress Billing 032818Document8 pagesProgress Billing 032818Francis F. RivamonteNo ratings yet

- Segment Wise Revenue and Cost Analysis of Consumer Goods CompanyDocument47 pagesSegment Wise Revenue and Cost Analysis of Consumer Goods Companyrahul1094No ratings yet

- Payment Certificates for Construction ProjectsDocument48 pagesPayment Certificates for Construction Projectsfilomeno martinsNo ratings yet

- My First ExperimentDocument4 pagesMy First ExperimentRamesh RadhakrishnarajaNo ratings yet

- Real Estate vs Shares Investment ComparisonDocument19 pagesReal Estate vs Shares Investment Comparisonamit1234No ratings yet

- Product CostingDocument8 pagesProduct CostingHitesh RawatNo ratings yet

- WPR SR1285477 COCS Clean Up Minas 7C-77 (Site Prep) Cut Off 29 Nop 2019Document47 pagesWPR SR1285477 COCS Clean Up Minas 7C-77 (Site Prep) Cut Off 29 Nop 2019Erick SavrinaldoNo ratings yet

- Cma of HostelDocument128 pagesCma of HostelkolnureNo ratings yet

- FormworksDocument94 pagesFormworksLouie Zavalla LeyvaNo ratings yet

- Data Cycle Time & Target Produksi Die CastingDocument7 pagesData Cycle Time & Target Produksi Die CastingHeri SutiknoNo ratings yet

- Project ReportDocument16 pagesProject Reportmaxaryan0% (1)

- Contract Package Schedule: Average Foreign Currency RateDocument23 pagesContract Package Schedule: Average Foreign Currency RateThon Marvine Dionisio UrbanoNo ratings yet

- Sales & Revenue Dashboard: October 2012Document4 pagesSales & Revenue Dashboard: October 2012Ramesh RadhakrishnarajaNo ratings yet

- Britania ValuationDocument28 pagesBritania ValuationSantanu DasNo ratings yet

- FM Assignment - Prashant KhombhadiaDocument3 pagesFM Assignment - Prashant Khombhadiavicky54321inNo ratings yet

- Balance Sheet - in Rs. Cr.Document72 pagesBalance Sheet - in Rs. Cr.sukesh_sanghi100% (1)

- Britannia Industries LTD Industry:Food and Dairy Products - MultinationalDocument22 pagesBritannia Industries LTD Industry:Food and Dairy Products - MultinationalArghya SenNo ratings yet

- Diamond Cutting Industry Retained EarningsDocument12 pagesDiamond Cutting Industry Retained EarningsVaibhav ShahNo ratings yet

- Project Task EffortTracker TemplateDocument15 pagesProject Task EffortTracker TemplateSayedAsgarAliNo ratings yet

- The Creeping WormDocument4 pagesThe Creeping WormRamesh RadhakrishnarajaNo ratings yet

- ACCPA Conference 2017 - IFC PresentationDocument23 pagesACCPA Conference 2017 - IFC PresentationGodsonNo ratings yet

- Business ValuationDocument2 pagesBusiness Valuationahmed HOSNYNo ratings yet

- Management Accounting SampleDocument25 pagesManagement Accounting SampleEdward Baffoe100% (1)

- Project progress report Jan 14Document2 pagesProject progress report Jan 14Uday PandheNo ratings yet

- SEEP FRAME Tool, Version 2.02Document159 pagesSEEP FRAME Tool, Version 2.02anish-kc-8151No ratings yet

- DPWH-Isabela Second District Engineering Office Contract Payment ChecklistDocument26 pagesDPWH-Isabela Second District Engineering Office Contract Payment ChecklistLouie MacniNo ratings yet

- WHO - HMN HIS Tools To Support GFR10 - Template For Costing The HIS GapDocument202 pagesWHO - HMN HIS Tools To Support GFR10 - Template For Costing The HIS GapHarumNo ratings yet

- Just Some BlingDocument5 pagesJust Some BlingRamesh RadhakrishnarajaNo ratings yet

- Update Project Control Sheet PT Sekman Wisata 27 April 2020Document27 pagesUpdate Project Control Sheet PT Sekman Wisata 27 April 2020dedy suryaNo ratings yet

- Add: Purchases Net of Scheme Cost (Including F. Goods Purchases)Document12 pagesAdd: Purchases Net of Scheme Cost (Including F. Goods Purchases)rinku10431No ratings yet

- Valuation Healthcare IndustryDocument7 pagesValuation Healthcare IndustryProbal BiswasNo ratings yet

- Personlig BudgetDocument6 pagesPersonlig BudgetAnn SundkvistNo ratings yet

- Arctic Insultion Case Study - Rashik GuptaDocument12 pagesArctic Insultion Case Study - Rashik GuptaRashik Gupta50% (2)

- Break-Even Visualizer TemplateDocument4 pagesBreak-Even Visualizer TemplateAnnaNo ratings yet

- Netstal Hourly Production Monitoring Sheet 09-08-2018Document1 pageNetstal Hourly Production Monitoring Sheet 09-08-2018saadbinsadaqat123456No ratings yet

- Schedule of Duties and Professional Charges For Quantity SurveyingDocument4 pagesSchedule of Duties and Professional Charges For Quantity SurveyingJared MakoriNo ratings yet

- OMR 450,000 OMR 3,000,000: Planned-Monthly Gross Actual-Monthly Planned-Cumulative Gross Actual-CumulativeDocument1 pageOMR 450,000 OMR 3,000,000: Planned-Monthly Gross Actual-Monthly Planned-Cumulative Gross Actual-CumulativeDINESHNo ratings yet

- JUBlifeDocument37 pagesJUBlifeavinashtiwari201745No ratings yet

- PROBLEM 2-45:: Particulars Case A Case B Case CDocument6 pagesPROBLEM 2-45:: Particulars Case A Case B Case CSrihari KumarNo ratings yet

- Cost Control Spreadsheet BLK ADocument17 pagesCost Control Spreadsheet BLK AØwięs MØhãmmed100% (1)

- Cumulative Cost Curve Percent TemplateDocument10 pagesCumulative Cost Curve Percent TemplatensadnanNo ratings yet

- Contract No.: 2017eod0001Document11 pagesContract No.: 2017eod0001Jhundel PajarillagaNo ratings yet

- Tender Evaluation ScoresDocument28 pagesTender Evaluation Scoresmuhammad iqbalNo ratings yet

- Gail India LTD ReferenceDocument46 pagesGail India LTD Referencesharadkulloli100% (1)

- Project Scheduling & Costing: Objectives Test Project Task Start Finished Days Q1 Q2 Q3 Q4Document5 pagesProject Scheduling & Costing: Objectives Test Project Task Start Finished Days Q1 Q2 Q3 Q4Ejaz Ahmed RanaNo ratings yet

- Cause and Effect Diagram For Export Development Canada: Quality Tool - Fish BoneDocument2 pagesCause and Effect Diagram For Export Development Canada: Quality Tool - Fish BonewaweruhNo ratings yet

- Milestone 3 Evm Powerhouse1Document1 pageMilestone 3 Evm Powerhouse1api-59751528No ratings yet

- Appropriations Dividend To Shareholders of Parent CompanyDocument30 pagesAppropriations Dividend To Shareholders of Parent Companyavinashtiwari201745No ratings yet

- Financial Feasibility of Product ADocument4 pagesFinancial Feasibility of Product AMuhammad AsadNo ratings yet

- Untitled SpreadsheetDocument816 pagesUntitled SpreadsheetrakhalbanglaNo ratings yet

- DCF & Relative Valuation of Reliance EnergyDocument96 pagesDCF & Relative Valuation of Reliance EnergySovit JaiswalNo ratings yet

- Major CIF & Joints Jointing and TestingDocument1 pageMajor CIF & Joints Jointing and TestingMohamed ImranNo ratings yet

- ZZZZZZDocument3 pagesZZZZZZZizamele ShabalalaNo ratings yet

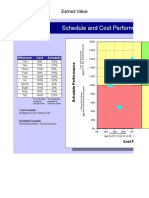

- Earned Value Quadrant ChartDocument2 pagesEarned Value Quadrant ChartAbhishek Pandey100% (1)

- TOTAL PC FLOWTEC INDIA ORGANIZATION CHARTDocument51 pagesTOTAL PC FLOWTEC INDIA ORGANIZATION CHARTHarshanand KalgeNo ratings yet

- Final Report C.PDocument14 pagesFinal Report C.PRozminSamnaniNo ratings yet

- Cost of Capital: Financial Management ProjectDocument10 pagesCost of Capital: Financial Management ProjectMoinak DasNo ratings yet

- Cost of Capital ComponentsDocument27 pagesCost of Capital ComponentsShashank PandeyNo ratings yet

- Module 4 - The Cost of CapitalDocument10 pagesModule 4 - The Cost of CapitalMarjon DimafilisNo ratings yet

- Unctad - Trade and Dev Report 1997 - Pp.69-98Document220 pagesUnctad - Trade and Dev Report 1997 - Pp.69-98vica3_No ratings yet

- Mongolia Sources of GrowthDocument32 pagesMongolia Sources of Growthvica3_100% (1)

- MDG Mongolia ReportDocument61 pagesMDG Mongolia ReportkhashchuluunNo ratings yet

- Barmash Web EngDocument2 pagesBarmash Web Engvica3_No ratings yet

- WB EAP Econ Seminar - EngDocument6 pagesWB EAP Econ Seminar - Engvica3_No ratings yet

- Project Management HandbookDocument48 pagesProject Management HandbookNancy Carolina Salcedo HernandezNo ratings yet

- How Is Crude Coal Tar DerivedDocument8 pagesHow Is Crude Coal Tar DerivedRudy MadianNo ratings yet

- England: by Hulan M. ASU Class: 5 (A)Document3 pagesEngland: by Hulan M. ASU Class: 5 (A)vica3_No ratings yet

- Tree HoroscopeDocument12 pagesTree Horoscopevica3_100% (2)

- Beyond BetrayalDocument11 pagesBeyond Betrayalvica3_100% (1)

- Celtic Astrology HoroscopesDocument3 pagesCeltic Astrology Horoscopesvica3_100% (2)

- Abusive Betrayal of LoveDocument2 pagesAbusive Betrayal of Lovevica3_No ratings yet

- Chapter 29-The Monetary SystemDocument51 pagesChapter 29-The Monetary SystemThảo DTNo ratings yet

- Test of T.B (2 Copies)Document4 pagesTest of T.B (2 Copies)vriddhi kanodiaNo ratings yet

- Question #1: Inventory ItemDocument7 pagesQuestion #1: Inventory ItemAngelo TipaneroNo ratings yet

- Valuation of SecuritiesDocument8 pagesValuation of SecuritiesVinayak SaxenaNo ratings yet

- Lex Service PLCDocument3 pagesLex Service PLCMinu RoyNo ratings yet

- Medicine Vending Machine - MedEx PDFDocument23 pagesMedicine Vending Machine - MedEx PDFHariz Syahmi100% (3)

- DC 51: Busi 640 Case 3: Valuation of Airthread ConnectionsDocument4 pagesDC 51: Busi 640 Case 3: Valuation of Airthread ConnectionsTunzala ImanovaNo ratings yet

- Aqa Acc5 W QP Jan08Document8 pagesAqa Acc5 W QP Jan08Yusuf EyoNo ratings yet

- Economic Value Added-Shrieves & Wachowicz PDFDocument17 pagesEconomic Value Added-Shrieves & Wachowicz PDFxaver lawNo ratings yet

- IFRS 16 Example: Initial Measurement of The Right-Of-Use Asset and Lease Liability (Quarterly Payments)Document4 pagesIFRS 16 Example: Initial Measurement of The Right-Of-Use Asset and Lease Liability (Quarterly Payments)Ankit ShahNo ratings yet

- LDJZ Bhjlafh Aduighjh DDocument20 pagesLDJZ Bhjlafh Aduighjh Dsernhaow_658673991No ratings yet

- SFM MTP - May 2018 QuestionDocument6 pagesSFM MTP - May 2018 QuestionMajidNo ratings yet

- Test - Finance & Accounting For Managers - WBPN222100 - 1Document3 pagesTest - Finance & Accounting For Managers - WBPN222100 - 1محمد شاميمNo ratings yet

- Mini Project - QuestionsDocument28 pagesMini Project - QuestionsMuskan Rathi 5100No ratings yet

- 05 Lecture - The Time Value of Money PDFDocument26 pages05 Lecture - The Time Value of Money PDFjgutierrez_castro7724No ratings yet

- Ebit Revenue - Operating ExpensesDocument7 pagesEbit Revenue - Operating ExpensesArchay TehlanNo ratings yet

- q4 1Document7 pagesq4 1JimmyChaoNo ratings yet

- Problems: Set B: InstructionsDocument4 pagesProblems: Set B: InstructionsflrnciairnNo ratings yet

- Valuing Bonds: Fundamentals of Corporate FinanceDocument26 pagesValuing Bonds: Fundamentals of Corporate FinanceNabeel Ahmed ShaikhNo ratings yet

- Shareholders' Equity: 2. Journal Entry MethodDocument5 pagesShareholders' Equity: 2. Journal Entry MethodSuzette VillalinoNo ratings yet

- BBM-DH47ISB-03 - Saragam Aluminium Limited - 4usDocument36 pagesBBM-DH47ISB-03 - Saragam Aluminium Limited - 4usNguyet Tran Thi ThuNo ratings yet

- Chapter 7 SolutionsDocument8 pagesChapter 7 SolutionsAustin LeeNo ratings yet

- Capital Markets Chapter 3Document11 pagesCapital Markets Chapter 3Faith FajarilloNo ratings yet

- Fundamental Principles of ValuationDocument6 pagesFundamental Principles of Valuationnatalie clyde matesNo ratings yet

- Chapter 5 Solutions V1Document16 pagesChapter 5 Solutions V1meemahsNo ratings yet

- Chapter 4 Investments in Debt Securities and Other Long Term InvestmentDocument30 pagesChapter 4 Investments in Debt Securities and Other Long Term InvestmentAngelica Joy ManaoisNo ratings yet

- Oromia Pipe Factory PLC Business Valuation ReportDocument122 pagesOromia Pipe Factory PLC Business Valuation ReportKokand100% (1)

- Capital Budgeting Chapter 14 True False QuestionsDocument38 pagesCapital Budgeting Chapter 14 True False QuestionsXandae MempinNo ratings yet

- Calculations for bond premium, discount, interest expense and carrying amountDocument9 pagesCalculations for bond premium, discount, interest expense and carrying amountClaire BarbaNo ratings yet

- FIN2339-Ch4 - Practice QuestionsDocument3 pagesFIN2339-Ch4 - Practice QuestionsJasleen Gill100% (1)