You might also like

- Waste Management SNBP 9thd Euminds 22-23Document31 pagesWaste Management SNBP 9thd Euminds 22-23api-570680528No ratings yet

- 52211CA Commercial Banking in Canada Industry ReportDocument34 pages52211CA Commercial Banking in Canada Industry ReportAnshul Sharma100% (1)

- PG 4. Gccs in India - To Be or Not To Be... PG 41. Interview: MR Sashidharan Balasundaram, Isg ResearchDocument52 pagesPG 4. Gccs in India - To Be or Not To Be... PG 41. Interview: MR Sashidharan Balasundaram, Isg ResearchRaghvendra N DhootNo ratings yet

- Jute History Bangladesh Harvard PDFDocument312 pagesJute History Bangladesh Harvard PDFBarry Fradkin100% (1)

- B.A. Hons Economics Readings 2012 13Document13 pagesB.A. Hons Economics Readings 2012 13Puja KumariNo ratings yet

- Pros and Cons of Violence in GamesDocument3 pagesPros and Cons of Violence in GamesAnjana AgnihotriNo ratings yet

- Waste Management in Hotel Indistry-1Document27 pagesWaste Management in Hotel Indistry-1arpit verma100% (2)

- Accountancy Project Book - 47thDocument14 pagesAccountancy Project Book - 47thHimanshu Dadhich0% (1)

- Soneri Bank Managment ProjectDocument29 pagesSoneri Bank Managment ProjectAamir Raza100% (3)

- Group Members:: Comparison Between Bank AL Habib & Habib Metro BankDocument13 pagesGroup Members:: Comparison Between Bank AL Habib & Habib Metro BankAbbas AliNo ratings yet

- Submitted By:-: (GROUP-5)Document18 pagesSubmitted By:-: (GROUP-5)Debendra Kumar NayakNo ratings yet

- Commercial Banking Assignment: Analysis of Assets and Liabilities of A BankDocument15 pagesCommercial Banking Assignment: Analysis of Assets and Liabilities of A BankAyaz QaiserNo ratings yet

- Yes Bank - India's 4th largest private bankDocument14 pagesYes Bank - India's 4th largest private banksanju kumarNo ratings yet

- Press Release: L&T Infrastructure Finance Company LimitedDocument4 pagesPress Release: L&T Infrastructure Finance Company Limitedjignesh_vaderaNo ratings yet

- Greater Bombay Bank CO OPERATIVESDocument62 pagesGreater Bombay Bank CO OPERATIVESsnehalgaikwadNo ratings yet

- The Rajastan Co-Operative BankDocument12 pagesThe Rajastan Co-Operative Bankjini03No ratings yet

- One Bank Final Review AssignmentDocument5 pagesOne Bank Final Review AssignmentJonaed Ashek Md. RobinNo ratings yet

- Step Up - Understanding Lump Sum, Sip, STP, SWPDocument12 pagesStep Up - Understanding Lump Sum, Sip, STP, SWPaadhil1992No ratings yet

- Yes Bank - ReportDocument51 pagesYes Bank - ReportRajatNo ratings yet

- SBI Investment ProductsDocument20 pagesSBI Investment ProductssaravananNo ratings yet

- IBS Session 1 With SolutionDocument16 pagesIBS Session 1 With SolutionMOHD SHARIQUE ZAMANo ratings yet

- Financial Planning For Retirement NewDocument26 pagesFinancial Planning For Retirement NewNamrataNo ratings yet

- Page 1 of 3 Islamic Naya Pakistan Certificates - February 2021Document6 pagesPage 1 of 3 Islamic Naya Pakistan Certificates - February 2021MWBABARNo ratings yet

- Ovely Rofessional Niversity: Personal Financial PlanningDocument6 pagesOvely Rofessional Niversity: Personal Financial PlanningGagandeep SinghNo ratings yet

- P-Soup Business PlanDocument23 pagesP-Soup Business PlanHeavenson ChimaNo ratings yet

- State Bank of PatialaDocument5 pagesState Bank of PatialaBaljinderrai7No ratings yet

- Sales Kit Backup 1Document28 pagesSales Kit Backup 1api-26863276No ratings yet

- ProCredit NVB Angola 2006Document44 pagesProCredit NVB Angola 2006lumcolor100% (1)

- Chapter3 Bank OperationsDocument16 pagesChapter3 Bank OperationsRiya AgarwalNo ratings yet

- The Preferred Partner in Prosperity: One Stop Solution For All Banking NeedsDocument37 pagesThe Preferred Partner in Prosperity: One Stop Solution For All Banking NeedsvelankanniamNo ratings yet

- Module 1 - Time Value of Money Handout For LMS 2020Document8 pagesModule 1 - Time Value of Money Handout For LMS 2020sandeshNo ratings yet

- Banking ReportDocument8 pagesBanking Reportisteaq ahamedNo ratings yet

- Ooredoo Group - RFP - MODE - Commercial ProposalDocument7 pagesOoredoo Group - RFP - MODE - Commercial ProposalAntony KanyokoNo ratings yet

- Week 2 Treasury Management by LCLEJARDEDocument34 pagesWeek 2 Treasury Management by LCLEJARDEErica CadagoNo ratings yet

- Bank Muamalat LoanDocument7 pagesBank Muamalat LoanSiveram MarthammuthuNo ratings yet

- CASHe LoansDocument7 pagesCASHe LoansAshwani KumarNo ratings yet

- Module 1Document53 pagesModule 1SSNo ratings yet

- National Bank of Pakistan: ChairmanDocument32 pagesNational Bank of Pakistan: ChairmanfarrukhNo ratings yet

- Investor Returns and Banking Industry AnalysisDocument6 pagesInvestor Returns and Banking Industry AnalysisAnooja SajeevNo ratings yet

- Sreekarayil ChitsDocument16 pagesSreekarayil ChitsSatyamev JayateNo ratings yet

- LIC Housing Finance LTD FDDocument6 pagesLIC Housing Finance LTD FDBiswa Jyoti GuptaNo ratings yet

- SKCILDocument16 pagesSKCILSatyamev JayateNo ratings yet

- Present Value and Rate of Return - 3Document29 pagesPresent Value and Rate of Return - 3hdy66No ratings yet

- FIN619 - Internship ReportDocument27 pagesFIN619 - Internship Reportmalik_saleem_akbarNo ratings yet

- The Bank of Punjab Latest Internship Report With Three Years Financial DataDocument23 pagesThe Bank of Punjab Latest Internship Report With Three Years Financial DataMuhammad Taif KhanNo ratings yet

- Small Savings: ObjectivesDocument5 pagesSmall Savings: ObjectivesGuruRajNo ratings yet

- Manappuram General Finance & Leasing Ltd. (Gold Loan)Document14 pagesManappuram General Finance & Leasing Ltd. (Gold Loan)Rushabh ShahNo ratings yet

- Refinancing Savings Round 2: Frasers Commercial TrustDocument5 pagesRefinancing Savings Round 2: Frasers Commercial Trustcentaurus553587No ratings yet

- LT Infrastructure Final Product NoteDocument1 pageLT Infrastructure Final Product NoteChandra Mohan SNo ratings yet

- Rate of InterestDocument1 pageRate of InterestMinhaz UddinNo ratings yet

- Ahmad Hamidi MaduDocument129 pagesAhmad Hamidi MaduAfiq NadzmiNo ratings yet

- Govt. IncentivesDocument19 pagesGovt. IncentivesMANTRA COLLEGENo ratings yet

- Credible Microfinance Private LimitedDocument2 pagesCredible Microfinance Private LimitedDebabrata MalickNo ratings yet

- Final Project ReportDocument18 pagesFinal Project ReportUsamaNaeemNo ratings yet

- OfferLetter 712470 31012024 9928 638423112048934621Document6 pagesOfferLetter 712470 31012024 9928 638423112048934621My ArchitectNo ratings yet

- UblDocument3 pagesUbladeel haiderNo ratings yet

- Updated Presentation On Operations (Company Update)Document25 pagesUpdated Presentation On Operations (Company Update)Shyam SunderNo ratings yet

- SHORT RESEARCH-WPS OfficeDocument5 pagesSHORT RESEARCH-WPS OfficeClinton Dimaya BasilaNo ratings yet

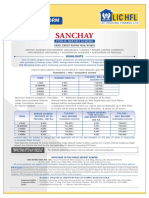

- Sanchay Public Deposit Scheme FormDocument6 pagesSanchay Public Deposit Scheme FormChilly IvaNo ratings yet

- Amanjot Kaur 2191003Document35 pagesAmanjot Kaur 2191003AmanjotNo ratings yet

- Behavioral Decision MakingDocument24 pagesBehavioral Decision MakinglushcheeseNo ratings yet

- Excercise3 Problems in JumpsDocument3 pagesExcercise3 Problems in JumpslushcheeseNo ratings yet

- Nooruddin's Family Decision 30-04-2014Document4 pagesNooruddin's Family Decision 30-04-2014lushcheeseNo ratings yet

- Stage 2 Lending Operation and RMDocument14 pagesStage 2 Lending Operation and RMlushcheeseNo ratings yet

- Jumper Value List 14-05-2014Document1 pageJumper Value List 14-05-2014lushcheeseNo ratings yet

- Decision Coaching Journal HighlightsDocument4 pagesDecision Coaching Journal HighlightslushcheeseNo ratings yet

- Interview With Usher Q:: What Were You Hoping For When You Started Off?Document2 pagesInterview With Usher Q:: What Were You Hoping For When You Started Off?lushcheeseNo ratings yet

- Metropolitan Service System (MV)Document50 pagesMetropolitan Service System (MV)lushcheeseNo ratings yet

- Research Assignment - Satellite Communication SystemDocument18 pagesResearch Assignment - Satellite Communication SystemlushcheeseNo ratings yet

- Virtual LAN (VLAN)Document16 pagesVirtual LAN (VLAN)lushcheeseNo ratings yet

- Assignment 2 - Interview Instructional Video LayoutDocument12 pagesAssignment 2 - Interview Instructional Video LayoutlushcheeseNo ratings yet

- Project - 2D Car Racing Game (Flash) DocumentationDocument45 pagesProject - 2D Car Racing Game (Flash) Documentationlushcheese76% (49)

- Proposal & Base Line Project Plan - CompucareDocument6 pagesProposal & Base Line Project Plan - CompucarelushcheeseNo ratings yet

- Pakistan Economy Challenges ProspectsDocument14 pagesPakistan Economy Challenges ProspectsArslan AwanNo ratings yet

- Business Communication-Ders NotuDocument223 pagesBusiness Communication-Ders NotuDaniyal KhanNo ratings yet

- Marketing Management - POS Solutions ProjectDocument13 pagesMarketing Management - POS Solutions Projectlushcheese100% (2)

- Article Presentation - Players in The System GameDocument3 pagesArticle Presentation - Players in The System Gamelushcheese0% (1)

- System AdministratorDocument1 pageSystem AdministratorlushcheeseNo ratings yet

- Money & Banking: Topics: Lesson 1 To 09Document13 pagesMoney & Banking: Topics: Lesson 1 To 09lushcheese100% (1)

- Strategic Management - Ufone ProjectDocument16 pagesStrategic Management - Ufone Projectlushcheese97% (29)

- Entrepreneurship Plastic Recycling ProjectDocument21 pagesEntrepreneurship Plastic Recycling Projectlushcheese95% (78)

- E Commerce ProposalDocument13 pagesE Commerce Proposallushcheese95% (56)

- Moneyandbanking10 22Document39 pagesMoneyandbanking10 22lushcheeseNo ratings yet

- Strategicmanagment 01-10Document24 pagesStrategicmanagment 01-10lushcheese100% (5)

- Marketingmanagment 01-10Document16 pagesMarketingmanagment 01-10lushcheese100% (2)

- Marketing Management 11 22Document28 pagesMarketing Management 11 22lushcheese100% (9)

- Moneyandbanking 01-09 Part2Document17 pagesMoneyandbanking 01-09 Part2lushcheeseNo ratings yet

- Reviewer Civil Procedure San Carlos CollegeDocument15 pagesReviewer Civil Procedure San Carlos CollegeSheena ValenzuelaNo ratings yet

- State Bank of Pakistan GOP IJARA SUKUK ProcedureDocument31 pagesState Bank of Pakistan GOP IJARA SUKUK ProcedureBabarKalamNo ratings yet

- CIS Individual EditableDocument6 pagesCIS Individual EditableJUNIE DAVE ORQUITANo ratings yet

- XYZ Bank Balance Sheet AnalysisDocument4 pagesXYZ Bank Balance Sheet AnalysisMarcusNo ratings yet

- Account Opening Form For Resident Individuals Sole Proprietorship Firms PDFDocument12 pagesAccount Opening Form For Resident Individuals Sole Proprietorship Firms PDFShashank YadavNo ratings yet

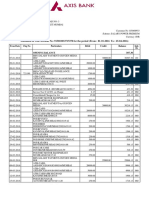

- Bank StatementDocument3 pagesBank StatementNeha Pradeep SainiNo ratings yet

- Bank CircularDocument159 pagesBank CircularpriyankaNo ratings yet

- ListDocument6 pagesListalonsoNo ratings yet

- Gujarat Electricity Regulatory Commission (GERC) Security Deposit RegulationsDocument10 pagesGujarat Electricity Regulatory Commission (GERC) Security Deposit RegulationsshirishNo ratings yet

- Economic Analysis of Banking Regulation: © 2005 Pearson Education Canada IncDocument15 pagesEconomic Analysis of Banking Regulation: © 2005 Pearson Education Canada IncMuntazir HussainNo ratings yet

- Bank ReconciliationDocument5 pagesBank Reconciliationrandom17341No ratings yet

- Financial Institutions and Markets Lecture Note: Chapter One Introduction To Financial System 1.1 Meaning of MoneyDocument130 pagesFinancial Institutions and Markets Lecture Note: Chapter One Introduction To Financial System 1.1 Meaning of MoneyEYOB AHMEDNo ratings yet

- Cbjesspl 09Document10 pagesCbjesspl 09Riya SharmaNo ratings yet

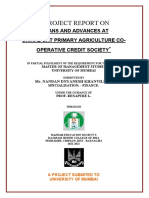

- Loans at Shiral Co-op Society ReportDocument72 pagesLoans at Shiral Co-op Society ReportNandan Khanvilkar100% (1)

- PrefaceDocument97 pagesPrefaceMAX PAYNENo ratings yet

- Practical Accounting 1Document14 pagesPractical Accounting 1Anonymous Lih1laaxNo ratings yet

- AE 111 MIDTERMS EXAM REVIEWDocument8 pagesAE 111 MIDTERMS EXAM REVIEWDjunah ArellanoNo ratings yet

- Fixed / Recurring Deposit Application-Cum-Deposit Slip Date: Deposit Opened in Branch: Branch SOL IDDocument3 pagesFixed / Recurring Deposit Application-Cum-Deposit Slip Date: Deposit Opened in Branch: Branch SOL IDSS56% (16)

- Washington Mutual (WMI) - Appendix To The Brief in Support of The Motion of Plaintiffs For Summary Judgment (Affidavit of Doreen Logan)Document216 pagesWashington Mutual (WMI) - Appendix To The Brief in Support of The Motion of Plaintiffs For Summary Judgment (Affidavit of Doreen Logan)meischer100% (1)

- Internship Report On Askari Bank LimitedDocument46 pagesInternship Report On Askari Bank Limitedbbaahmad89100% (4)

- Credit Creation Theory: The Concept of Money & How It Is CirculatedDocument2 pagesCredit Creation Theory: The Concept of Money & How It Is CirculatedMoud KhalfaniNo ratings yet

- Philippine Supreme Court upholds postal money order conditionsDocument31 pagesPhilippine Supreme Court upholds postal money order conditionsRosemarie Rimando CruzNo ratings yet

- 2020 Friendly Hills BankDocument34 pages2020 Friendly Hills BankNate TobikNo ratings yet

- Audit Working Paper (Contoh)Document65 pagesAudit Working Paper (Contoh)Trick1 HahaNo ratings yet

- 2012 Banking Services RFP - Exhibit Items - Supplement To Exhibit SAP PDFDocument0 pages2012 Banking Services RFP - Exhibit Items - Supplement To Exhibit SAP PDFanilr008No ratings yet

- Beneficiary Letter of InstructionDocument1 pageBeneficiary Letter of Instructionkdopson83% (12)

- IPL ReviewerDocument5 pagesIPL ReviewerPrincessNo ratings yet

- Digital Finance 10 May (EID)Document25 pagesDigital Finance 10 May (EID)Muhammad Awlad HossainNo ratings yet

- Lesson 8 - Bank Reconciliation StatementDocument18 pagesLesson 8 - Bank Reconciliation StatementLio MelNo ratings yet